Before You Sell Anything in Your 401(k), Read This

We think stocks will eventually recover from this downturn, and investors shouldn't wait on the sidelines until they do.

/s3.amazonaws.com/arc-authors/morningstar/3a6abec7-a233-42a7-bcb0-b2efd54d751d.jpg)

Editor’s note: Read the latest on how the coronavirus is rattling the markets and what investors can do to navigate it A version of this article was previously published on March 18, 2020.

Have you ever heard anyone say, "If I could go back in time, I would have bought shares of Apple AAPL in the '80s"?

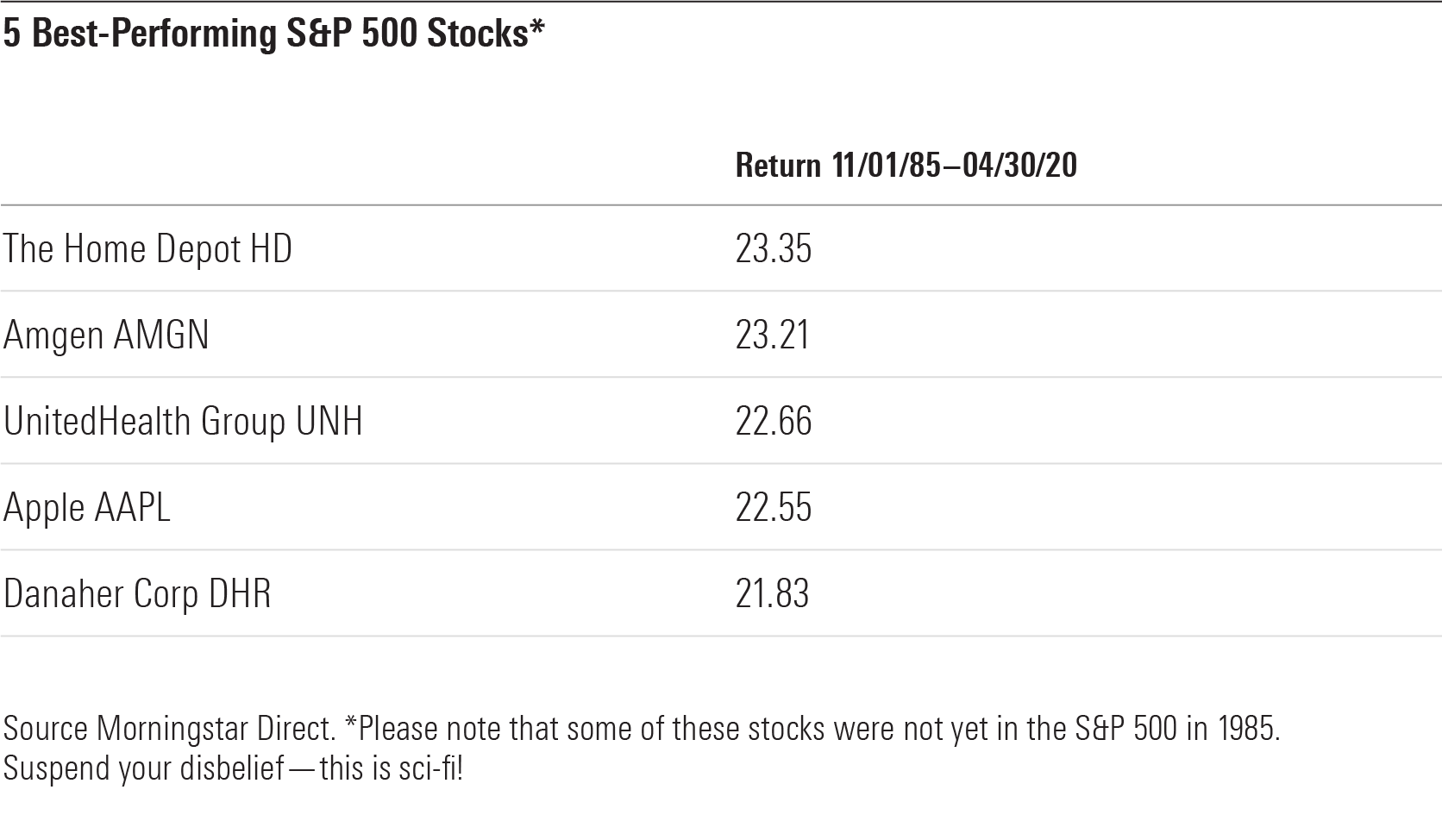

Let's go back to Oct. 26, 1985* (*the "future" date to which Marty McFly and Doc Brown must return in their time-traveling Delorean). We sidle up to a stockbroker (because we won't be trading online for a few decades) and say we want to buy the five S&P 500 stocks that will have the highest return over the next 35-ish years. The stockbroker looks at us quizzically, and we explain that we're time-travelers (maybe by pointing to the Delorean), so we already know what those five stocks (and their annualized returns) will be.

If we had invested $1,000 in each of these stocks back in 1985, we would have around $3 million today.

But achieving those returns would have meant that we stuck it out through thick and thin (and reinvested those dividends). For instance, we didn’t sell our Home Depot HD stock in 2002 even though our investment lost more than half its value. We knew the stock would have a fantastic decade between January 2009 and December 2019, when it would gain more than 630% cumulatively.

Same thing with Apple. We didn't sweat it when Apple stock plunged nearly 57% in 2008, because we knew the stock would come roaring back the next year, gaining almost 120% in 2009. (Hope the Delorean has a seatbelt!)

When It Comes to Long-Term Investing, Stocks Pay Off In real life, the future performance of any investment is uncertain. That's particularly true of stocks: An investor has (theoretically) unlimited upside potential if the company does well, but she could lose her entire investment if the company goes belly up. (That's why in real life, where we don't have a crystal ball or a Delorean, we should spread our investment bets beyond just five stocks. More on that later.)

Because stocks’ long-term outlooks are more uncertain than, say, investment-grade bonds that are very likely to pay a fixed amount of income over a specific time frame, stocks' prices are more prone to swing around.

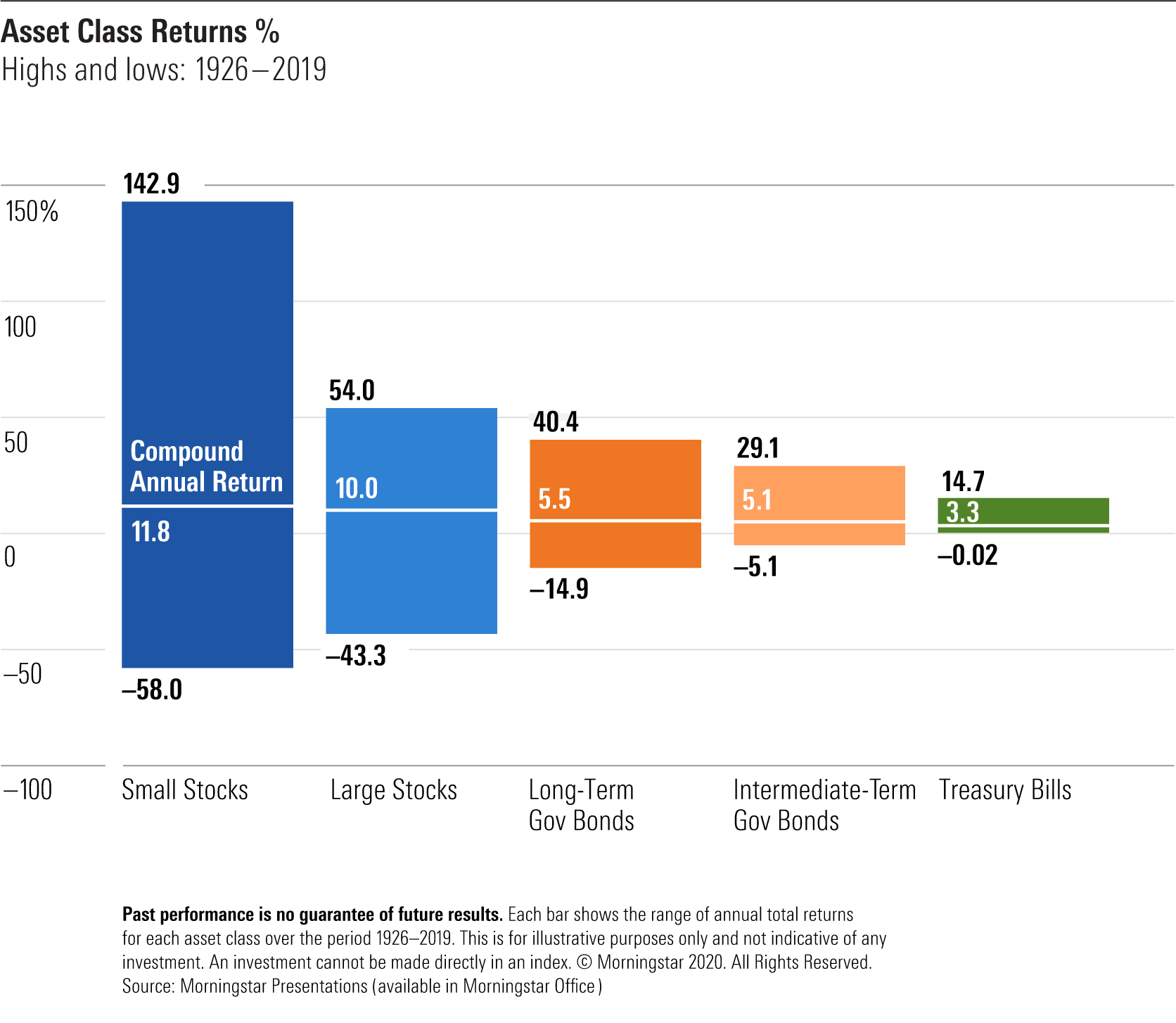

Why do people bother investing in stocks, then? Because historically, investors who have put up with stocks’ higher volatility (as measured by standard deviation, which shows how widely a stock’s price fluctuates from its median price) have been rewarded with higher returns. Consider the below chart, which compares the returns of these different asset classes.

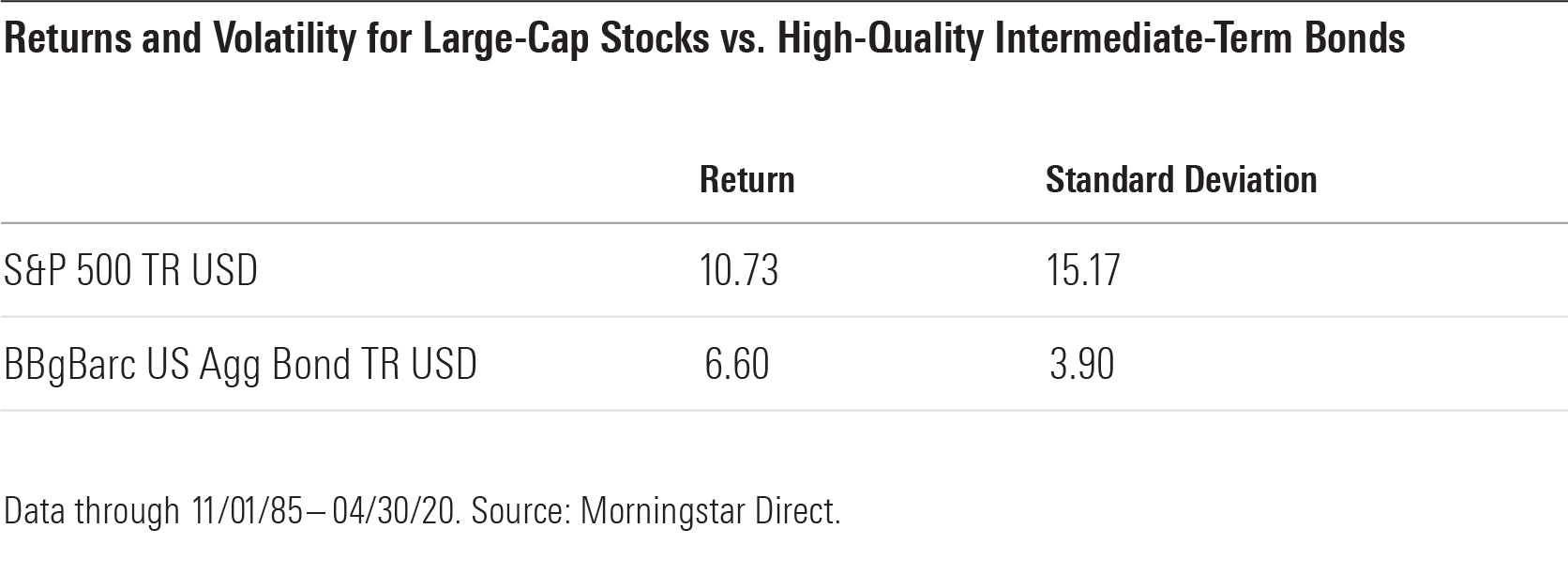

Even over our shorter Back-to-the-Future time frame (Oct. 26, 1985, through April 30, 2020), large-cap stocks outperformed high-quality intermediate-term bonds by more than 4 percentage points per year but were nearly 4 times as volatile. These returns are shown below.

"Market volatility is normal but nonetheless unsettling," said Morningstar Investment Management's chief investment officer Andew Lill. "In most cases, market corrections are healthy and create the mechanism for prices to better reflect fundamentals and allow the next phase of the market upturn."

In other words, you can expect stock prices to fall occasionally over short periods and maybe even over intermediate periods of a few years. But if you’re investing over long-term periods of a decade or more, chances are excellent that stocks as an asset class will earn a positive return.

Bear Markets Happen but They Don't Last Forever We think stocks will eventually recover from this impact, and that the long-term effects to the economy will be minimal. That doesn't mean we don't think the coronavirus concerns are a big deal.

Because this sell-off is tied to a global health epidemic, it’s especially scary. People feel like their personal safety as well as their financial security is threatened. They’re wondering, "Will I be OK? Even if I remain healthy, will I have any money left?"

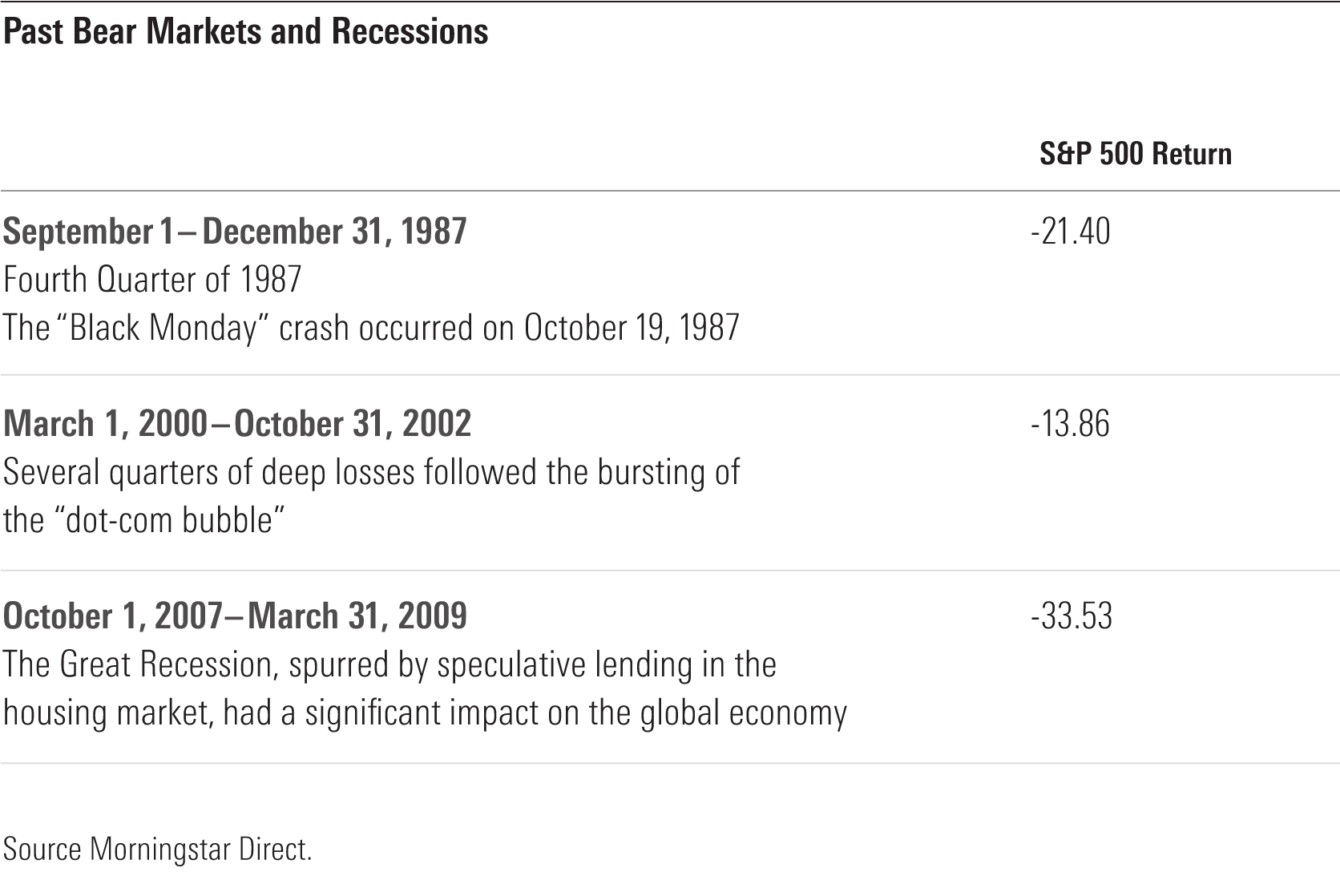

These fears are starting to feel like the new normal. In the first quarter, stock market losses were severe and sustained--the Morningstar US Market Index entered bear-market territory, losing more than 20%. The market regained its steam in April, but stocks have still lost around 10% in aggregate this year through the end of April. Although coronavirus concerns alone have not caused stocks' rout this year (uncertainties in the oil market have also taken their toll), they are certainly stoking the flames.

But bear markets, no matter their cause, don’t last forever. Markets and economies are resilient. Losses can be severe, though--and they can last for extended periods.

We think it's very likely that stocks will continue to decline this year. In "Coronavirus Update: Long-Term Economic Impact Forecast to Be Less Than 2008 Recession," Morningstar healthcare strategist Karen Andersen and equity analyst Preston Caldwell share their expectation that global gross domestic product will see a weighted average hit of 2.9% in 2020. But over the long term, they predict a very small impact. They believe that damage to productive capacity will be small and economic confidence should quickly return once the virus subsides. Additionally, the fiscal stimulus should prevent a collapse in demand.

Why You Should Invest in Stocks During This Market Downturn While we think more stock market losses are likely in the near term, that shouldn't be interpreted as a warning not to invest in the near term or as a recommendation to stay on the sidelines until things improve.

There are two good reasons not to sit this market downturn out.

If you're investing for the long term, this is a time to buy. If you stop contributing to your 401(k) during downturns, you're not buying stocks when they're cheap. Because the stock market has lost more than 10% so far this year, stocks (in aggregate) are cheaper than they were when 2020 started.

Trying to market-time in down markets can make losses much worse. Assuming you have a long time until you will need the money in your 401(k), you will most likely do more harm than good by pulling your money out and trying to get back in when things seem to be getting better.

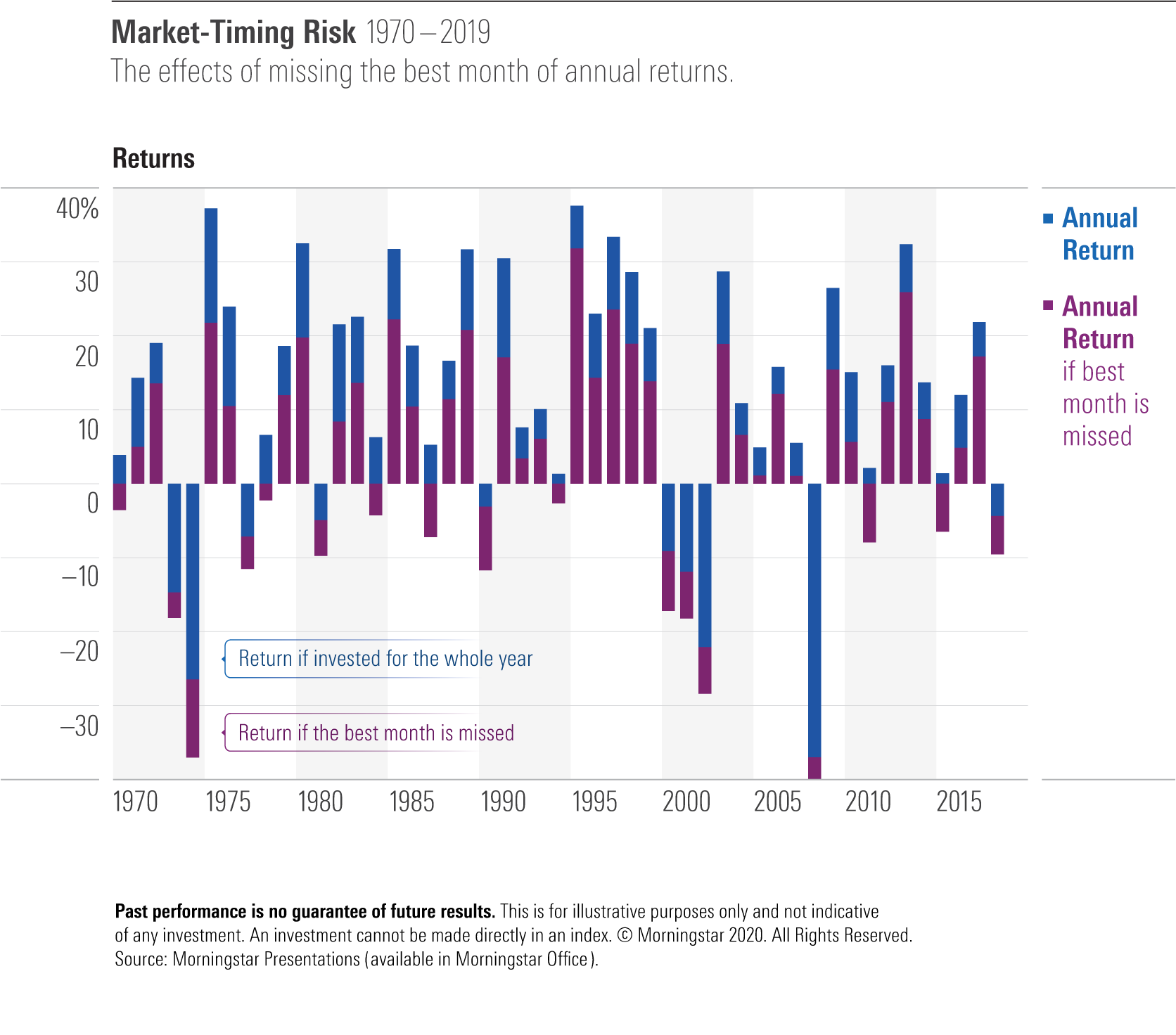

Steep stock market downturns are often followed by sharp recoveries, and investors who sit on the sidelines often miss out on these quick inflections. The image below illustrates the risk of attempting to time the stock market to avoid losses by showing the effects of missing the one best month of an annual return.

Rather than helping mitigate losses during years when returns were negative, missing the best month exaggerated the year’s loss. In seven of the 49 years shown (1970, 1978, 1984, 1987, 1994, 2011, and 2015), missing the best month would have dragged otherwise positive returns into negative territory.

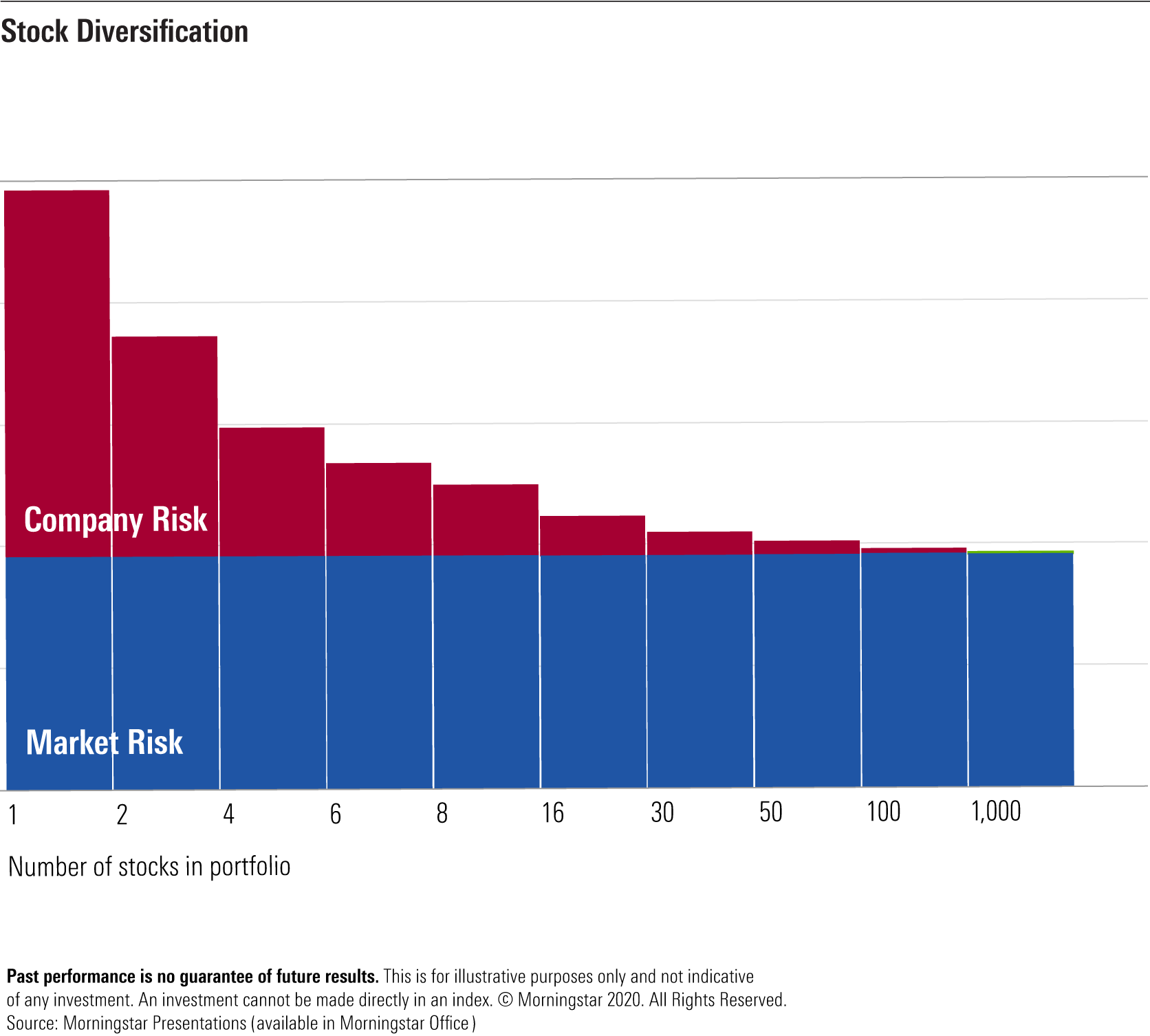

Reduce Risk by Diversifying, Not Selling Although it would be nice to have the Back-to-the-Future perspective of which stocks will perform best over the next 35 years, picking stocks isn't so easy when you don't know the future. What if you invest in five companies and three of them go bankrupt? Fortunately, there are some things you can do to help reduce risk and potentially improve returns.

You can reduce the risk of one failing stock negatively impacting your portfolio by holding lots of stocks. The image below shows that if an investor holds 100 stocks, he has essentially eliminated the impact of “company risk” from his portfolio.

Company risk, also known as business risk, is the risk that a specific stock might plunge because of non-market-related factors such as poor company management. This is beyond overall stock market risk and is not always rewarded with higher returns.

Holding broadly diversified investments is a good way to get exposure to stocks without having to worry as much that an individual company (or sector or industry) will have a large negative impact on your overall return. For instance, low-cost index funds that track the broad market provide exposure to lots of companies in different sectors and industries.

Holding international stock funds in addition to U.S. stock funds is another way to spread your bets and give yourself exposure to different economies and currencies.

You could also diversify by moving some money into safer assets, like bonds and cash. As we’ve discussed, stocks have offered good long-term return potential for investors who've held on for the sometimes white-knuckled ride. Stocks are prone to price gyrations, but that’s not really the same thing as risk. But, as Morningstar director of personal finance Christine Benz points out, volatility becomes risk if those gyrations occur at a time when you need to spend your money.

In other words, a 20-something investor with 40 years until retirement has plenty of time to recover from large losses. But for a 60-something investor who might need to start living off her retirement savings in the next few years, there might not be enough time to make her money back in the market if stocks don’t come roaring back soon.

Make sure you are taking on enough risk to give yourself the best chance of meeting your long-term investing goals. But if your investment goals are within the next 10 years, you might want to tilt toward safer assets.

As a model for this, you can look to target-date funds, which are professionally managed investments that aim to provide retirement savers at every life stage the best return potential for the amount of risk they take on. Target-date funds for investors age 40 and younger are mostly invested in a diversified mix of stock funds (both U.S. and international), and this mix shifts away from stocks and toward safer assets like fixed income as the investor moves toward their target retirement age.

Have a question about personal finance or investing? Please send me an email.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/YBH7V3XCWJ3PA4VSXNZPYW2BTY.png)

/d10o6nnig0wrdw.cloudfront.net/04-24-2024/t_a8760b3ac02f4548998bbc4870d54393_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/O26WRUD25T72CBHU6ONJ676P24.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/3a6abec7-a233-42a7-bcb0-b2efd54d751d.jpg)

{kind=link}