Which Alternatives Fit Into Your Portfolio?

Learn how different strategies can enhance diversification.

/s3.amazonaws.com/arc-authors/morningstar/502d0355-28ed-483c-ae9d-b67bfbf5291b.jpg)

Not all alternatives offer the same diversification benefits—and even when correlations look high, the degree of market sensitivity makes a big difference here. In our recently published 2024 Diversification Landscape report, Amy Arnott, Christine Benz, and I took a deep dive into how different asset classes performed in the past couple of years, how correlations have evolved, and what those changes mean for investors and financial advisors trying to build well-diversified portfolios. You can also check out Arnott’s Portfolio Basics series, where she goes over some fundamentals of assembling sound portfolios, including an installment on how to use alternatives in your portfolio.

Alternative strategies, as the name suggests, offer something fundamentally different from mainstream asset classes. Morningstar defines these strategies based on their ability to modify, diversify, or eliminate traditional market risks. There is considerable variation between strategies, though, and identifying appropriate benchmarks is tough. For that reason, we used Morningstar’s fund categories as proxies for the most common strategies rather than market indexes.

Alternatives classified as diversifiers include the equity market-neutral, event-driven, options-trading, relative value arbitrage, and multistrategy Morningstar Categories. These incorporate various traditional market risk factors found in equities, alongside nontraditional or alternative risk factors, or betas, to offer a more diversified source of long-term returns. Nontraditional betas include factors such as carry, momentum, and trend, but because these are combined with residual traditional risk factors, they are still exposed to losses during market crashes. The most common strategies in this group—equity market-neutral, event-driven, and relative value arbitrage—typically have less sensitivity to moves in equities markets. And even if those strategies move in the same direction as equities, the magnitude is typically much more muted. In all three cases, portfolio managers tend to trade securities both long and short against each other rather than trading against the overall market.

Strategies defined as opportunistic (macro trading and systematic trading) generally focus on absolute returns, meaning they aim for positive returns in all markets and focus more on capital preservation. Managers of these strategies move in and out of long and short positions as opportunities arise. Opportunistic funds tend to lose less in drawdowns but also come with more complexity. Sometimes these managers bet the market will continue moving in the same direction, sometimes they wager it won’t, and they often switch or hedge their bets. Market expectations can often get caught out of step, so they often use sophisticated risk-management systems to manage their myriad exposures.

Recent Performance Trends in Alternatives

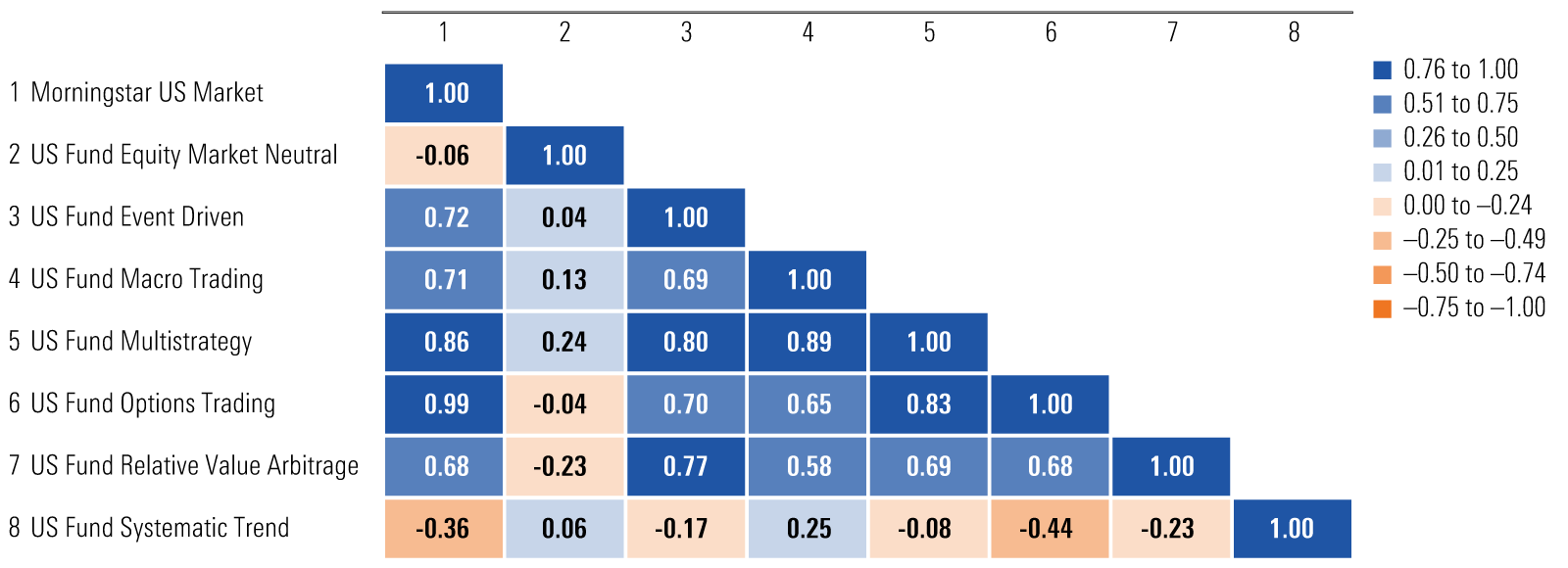

As the Morningstar US Market Index rose 26% in 2023, the alternative strategies categories delivered returns ranging between positive 17.1% and negative 4.4%. Trailing three-year correlations varied between 0.99 and negative 0.36, with two categories above 0.76. Unsurprisingly, the category with the strongest link to stocks fared the best with respect to returns, while the category with the weakest link was the only one to post negative returns in 2023: The options-trading category returned 17.1%, and the systematic trend category lost 4.4%. The relative value arbitrage, multistrategy, and event-driven categories all had medium to high correlations to the market and returned between 5.6% and 6.5% in 2023. Equity market-neutral, which has a near-zero correlation, returned 5.3%. Strategies in this category are meant to perform independently of the market. What might evoke some surprise is that the macro-trading category returned only 2% despite its 0.71 correlation to equities. This was due to its low equity and bond beta—an important consideration when assessing and understanding alternative categories’ performances.

Three-Year Correlation Matrix: Alternatives

Correlation figures tell us how directionally aligned these alternative categories’ returns are with the equity market’s returns but do not convey the magnitude of their performance. Thus, it’s also helpful to consider their respective betas (computed versus the Morningstar US Market Index), which provide insight into alternatives’ degree of sensitivity to equity movements. Alternatives exhibited three-year trailing equity betas between positive 0.53 and negative 0.18, with six of seven categories measuring below 0.26—meaning only 26% of their returns could be attributed to moves in the equity markets. With the macro-trading category, for example, based on correlations alone, investors might have expected the category to move in the same direction as equity markets but not the small degree to which that was the case. By factoring in the equity beta of 0.14, the category’s lackluster showing in 2023 makes more sense.

Longer-Term Trends in Alternatives

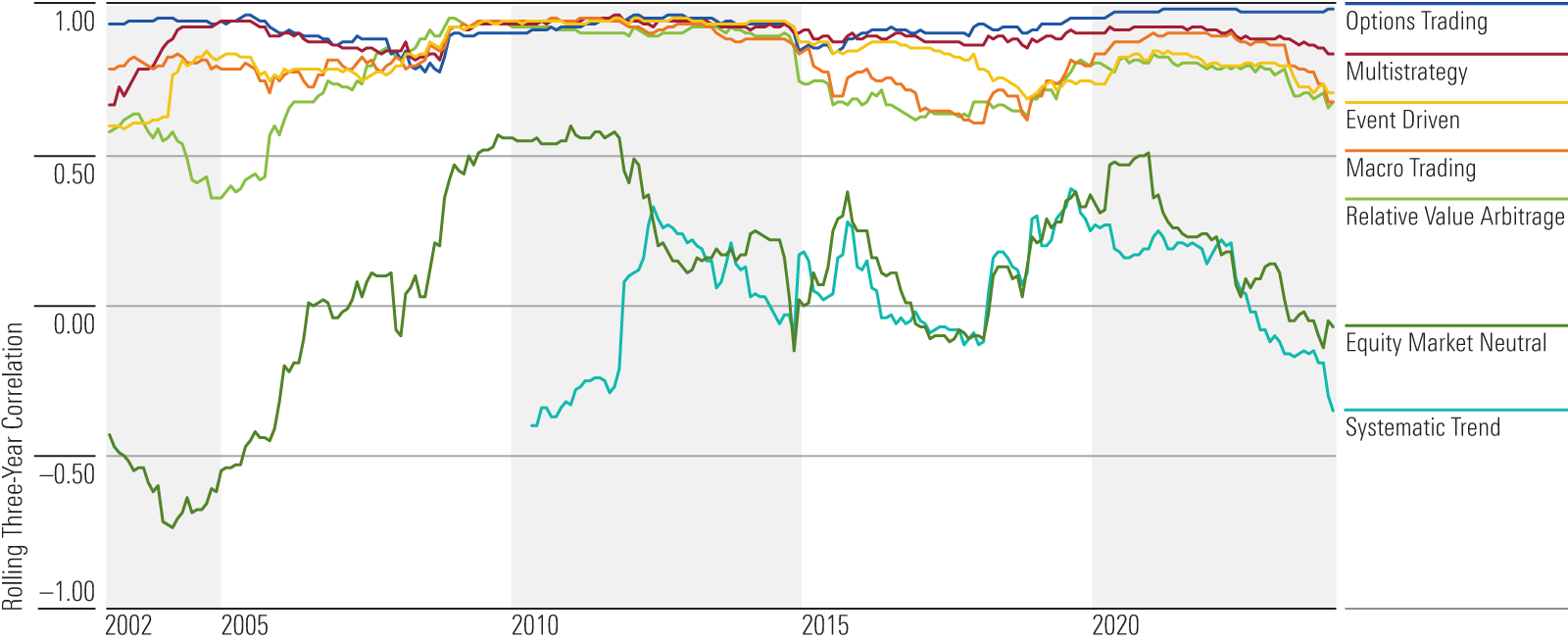

Over longer periods, correlations have been relatively stable for most categories, but some differences have arisen since our last analysis. In 2023, the three-year correlations for the systematic-trend, equity market-neutral, and macro-trading categories decreased the most. The systematic-trend category shifted deeper into negative territory, while equity market-neutral moved from a modestly positive correlation versus the overall equity market to a modestly negative one. Relative value arbitrage, event-driven, and multistrategy also became slightly less correlated to stock markets, while options-trading was marginally more correlated. Similarly, the three-year equity betas sat lower at the end of 2023 compared with one year prior and the 10-year average rolling figure for all but the options-trading category. Systematic trend’s rolling three-year beta decreased the most through 2023 and differed from its 10-year average by the greatest margin.

Rolling Three-Year Correlations vs. Morningstar US Market Index: Alternatives

Alternatives’ Implications for Your Portfolio

Investors seek out alternative strategies for a multitude of reasons, such as reducing drawdowns, seeking a wider range of risk factors or asset classes, or more portfolio stability. In other words, they’re not primarily viewed as return generators in bullish markets. Given alternatives’ primary purpose to complement and diversify an overall portfolio, it shouldn’t come as a surprise that in seven out of the past 10 calendar years, all seven alternative categories underperformed the Morningstar US Market Index, often by substantial margins. The benefit of alternatives becomes more evident when one considers intense market selloffs, such as the fourth quarter of 2018, the first quarter of 2020, and the first half of 2022′s market correction. The lower equity sensitivity translates into more modest losses during equity market drawdowns and in some cases even positive returns.

From a portfolio construction perspective, though, investors must remember that exceptionally low betas have a major impact on portfolio performance even when correlations seem high. Despite trailing US equities by a wide margin over the past decade, a 20% allocation to most categories of alternatives would have improved or matched risk-adjusted returns versus an all-equity portfolio or a balanced 60/40 portfolio. The strategies with the lowest 10-year equity betas—systematic trend and equity market-neutral—were the most additive to the portfolio’s Sharpe ratio.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/MNPB4CP64NCNLA3MTELE3ISLRY.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/SIEYCNPDTNDRTJFNF6DJZ32HOI.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZHTKX3QAYCHPXKWRA6SEOUGCK4.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/502d0355-28ed-483c-ae9d-b67bfbf5291b.jpg)