These ETFs Offer Durable Dividends

These funds aren't flawless, but they are solid options for income seekers.

/s3.amazonaws.com/arc-authors/morningstar/a90ba90e-1da2-48a4-98bf-a476620dbff0.jpg)

A version of this article previously appeared in the July 2021 issue of Morningstar ETFInvestor. Download a complimentary copy of Morningstar ETFInvestor by visiting the website.

Stocks that provide reliable streams of dividend income are appealing in most market environments. Though their current valuations aren’t compelling, stocks representing claims on solid franchises focused on generating cash and returning it to their owners may be one of the least-bad options available to investors facing low yields and rising inflation.

Here, I’ll take a look at the makings of a durable dividend, revisit two of our longtime favorite dividend exchange-traded funds, assess these funds’ blind spots, and take a peek at a trio of relative newcomers that try to harness dividend growth.

The Makings of a Durable Dividend

Dividends send a signal. When a company initiates a dividend, it tells the market that it is generating more cash than it can put to use by reinvesting it in existing business lines, new projects, acquisitions, and so on. It is an indication that the firm has begun to mature and that its most rapid growth is likely behind it.

Dividends are also a commitment device. They serve as an indirect means of enforcing capital allocation discipline on company management. Money earmarked for dividends can’t be spent frivolously, and the last thing a shareholder relying on regular dividends wants to see is signs of a dividend in distress.

Reliable dividends are rooted in solid franchises. Companies that are highly cash-generative and have low reinvestment requirements are likely to send regular checks to shareholders and grow those payments over time. These stocks include household names like Coca-Cola KO, McDonald’s MCD, and Procter & Gamble PG.

The Old Guard

There is no Coca-Cola-like secret recipe for building an equity portfolio that focuses on stocks with sturdy dividends. The not-so-secret ingredient in most dividend-growth ETFs’ selection criteria is a simple screen that sweeps in stocks based on their dividend track records.

Vanguard Dividend Appreciation ETF VIG, which carries a Morningstar Analyst Rating of Gold, and Schwab U.S. Dividend Equity ETF SCHD, which is rated Silver, both screen their selection universes based on stocks’ dividend history. VIG’s index requires stocks have a minimum of 10 years of consecutive dividend growth. SCHD’s benchmark mandates that stocks pay--though not necessarily grow--regular dividends for at least a decade to be considered. A decade or more of regular dividend payments sends a clear signal that these are companies that have committed to returning cash to shareholders. But can they keep it up?

Both VIG and SCHD employ additional selection criteria to focus on the firms that are most likely to maintain and grow their dividends, and to avoid dividend traps. VIG’s current Nasdaq bogy employs undisclosed proprietary criteria to weed out at-risk dividends. Its new benchmark, the S&P Dividend Growers Index, which it will transition to in the third quarter of 2021, weeds out the top 25% of eligible stocks as ranked by their indicated dividend yield. Above-normal yields are often an early sign that a dividend is in danger. Stocks that pass SCHD’s initial filter are scored based on a combination of their yield, free cash flow/ total debt, return on equity, and five-year dividend growth. These metrics help set aside stocks whose dividends may be sickly.

The effects of these funds’ emphasis on dividends’ staying power are evident in their portfolios. Exhibit 1 features key measures of their wherewithal to pay out steady streams of income. Relative to the broader U.S. market--proxied here by Gold-rated Vanguard Total Stock Market ETF VTI--they earn higher marks based on their stocks’ profitability and have a larger percentage of their portfolios invested in companies boasting wide or narrow Morningstar Economic Moat Ratings. VIG also scores higher on financial health, while SCHD’s grade matches VTI's.

These funds’ portfolios clearly skew toward higher-quality stocks. This means that they’ll likely fare better during market drawdowns and miss out on some of the market’s upside over the long term. But that’s not all they might miss. While their dividend focus is their greatest strength, it leaves them with a big blind spot.

Blind Spot

VIG and SCHD’s strict screens mean that they will miss out on stocks’ first decade of dividends. Some of these omissions will weed out companies whose plans to pay steady dividends never hatch. Others will weigh (and have weighed) on performance.

Exhibit 2 shows VIG and SCHD’s sector exposures relative to VTI. Both funds are significantly overweight in the steady-Eddie of dividend sectors, consumer staples, as well as industrials. But they are both correspondingly light on some of the sectors that have seen and/or may continue to see above-normal dividend growth for some time to come. Specifically, both funds are underweight in technology and communication services names. The funds are underweight in tech stocks on account of their relatively short dividend records. They have less exposure to communication services largely because Alphabet GOOG and Facebook FB--which collectively represent about 46% of the communications services sector within the S&P 500--have never paid a dividend.

By building their portfolios on the basis of dividend histories, these funds face a potential opportunity cost. They may miss out on 10 years’ worth of cash flows from the dividend franchises of the future. And they may also miss out on some of the market’s best-performing names. In that respect, they’re no different from any fund that strays from a broad, market-cap-weighted portfolio. After all, zeroing in on dividend payers is an active bet. In this case, some of their omissions have been costly. For example, the single biggest detractor from VIG’s performance relative to VTI during the trailing decade ended June 30, 2021, was a combination of being underweight in tech stocks and poor stock selection within that sector. Most notably, leaving out Apple AAPL, which is fast approaching the day when it will be eligible for inclusion in VIG’s portfolio, put a big dent in VIG’s performance relative to VTI over that 10-year span.

The (Newish) Kids on the Block

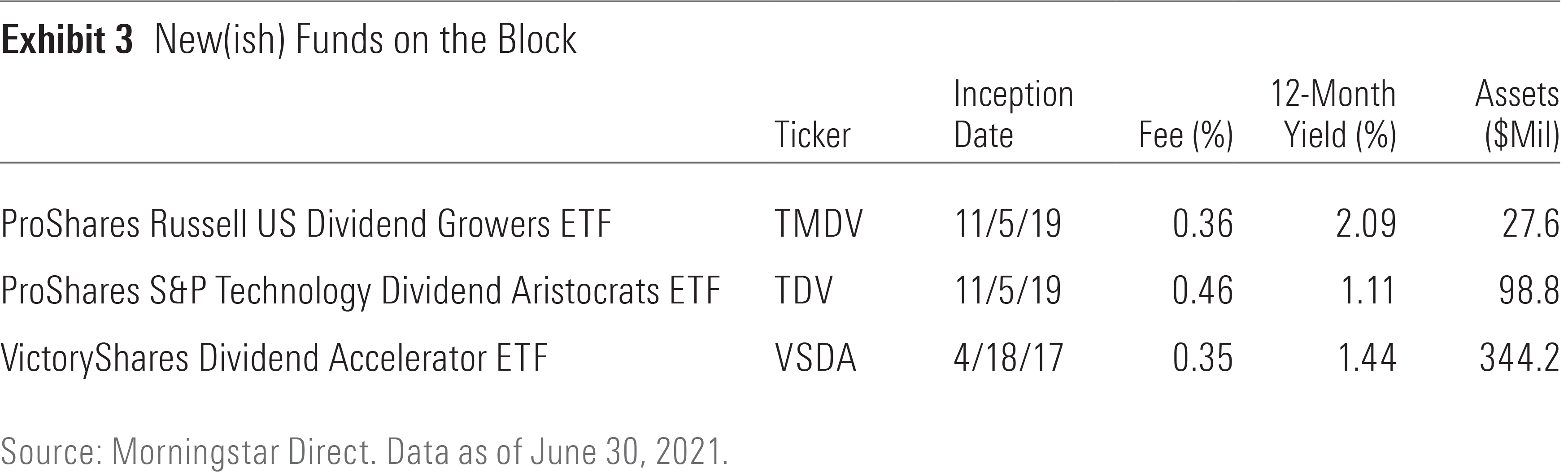

Over the past five years there have been two dividend ETFs launched that look to exploit the old-guard dividend ETFs’ blind spot. Another recent addition to the menu is even stricter than its predecessors.

ProShares S&P Technology Dividend Aristocrats ETF TDV was launched in November 2019, and it sits right in VIG and SCHD’s blind spot. It looks for tech and tech-related firms (it colors outside the GICS sector lines) that have grown their annual dividends for at least seven years in a row. As of March 31, 21 of the fund’s 38 holdings had less than 10 years of consecutive dividend growth, which would leave them on the outside of VIG and SCHD’s portfolios, looking in. This list includes names like Apple and Mastercard MA. Given that it holds so few names, stocks are weighted equally to ensure adequate diversification.

TDV has struggled over its brief history. Equal weighting means that it has been massively underweight in Apple and Microsoft MSFT, which together make up more than 40% of market-cap-weighted Technology Select Sector SPDR ETF’s XLK portfolio. From TDV’s November 2019 inception through June 30, 2021, it lagged XLK by more than 20 percentage points. So, while the fund isn’t blind to Apple’s long-term dividend growth potential, its weighting schema will prevent it from enjoying much of the tech giant’s upside--or that of any of its holdings--by definition.

VictoryShares Dividend Accelerator ETF VSDA launched in April 2017. The fund’s index draws stocks with at least five years of consecutive dividend growth from the Nasdaq U.S. Large Mid Index. Eligible stocks are scored based on 15 fundamental measures over a 10-year lookback period to assess which are most likely to continue growing their dividends in the future. Stocks are bucketed based on the duration of their dividend growth, with 65 of the 75 positions reserved for stocks with a minimum of 10 years of expanding cash outlays. So, while this fund saves space for some up-and-comers, most of its portfolio is invested in stocks with at least a decade of dividend growth. Merely tipping its hat to emerging dividend payers and limiting its reach to just 75 stocks leaves the fund light on tech and healthcare names--even more so than VIG as of the end of June.

ProShares Russell U.S. Dividend Growers ETF’s TMDV roster of stocks is a dividend-payers hall of fame. The fund, which launched alongside TDV in November 2019, tracks the Russell 3000 Dividend Elite Index. The benchmark employs the strictest screen of any dividend-oriented ETF, requiring stocks have 35 years of consecutive dividend growth to be eligible for inclusion. As of the beginning of July, the index held 69 companies, with an average of 48 consecutive years of dividend growth. Stocks are weighted equally. The fund’s stringent screen results in a narrow portfolio that drifts toward smaller, cheaper stocks, landing it in the mid-value Morningstar Category and leaving it decades away from including any of today’s emerging dividend payers. While it may have some appeal to dividend diehards, the fund’s relatively high fee (0.36%) and small asset base are important to consider. There are less-expensive options that are more likely to be around 35 years from now that apply slightly less-restrictive criteria to build more broadly diversified portfolios of solid dividend stocks.

Love the One You’re With

Despite their flaws, the old-guard duo of VIG and SCHD, in my opinion, remains among the best options for investors seeking a broadly diversified and low-cost source of growing dividend income. The funds’ blind spot is also their bedrock. While leaving out some of the market’s biggest names has cost them in recent years, there’s no guarantee that will be the case in the future--especially as more of those stocks become eligible for inclusion in these funds’ portfolios. In the meantime, they continue to provide a reliable source of dividend income in an income-challenged investment landscape.

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Morningstar, Inc. does not market, sell, or make any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/MNPB4CP64NCNLA3MTELE3ISLRY.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/SIEYCNPDTNDRTJFNF6DJZ32HOI.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZHTKX3QAYCHPXKWRA6SEOUGCK4.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/a90ba90e-1da2-48a4-98bf-a476620dbff0.jpg)