Have Strategic-Beta ETFs Lost Their Sizzle?

Smart beta, strategic beta, modern alpha, factors—whatever you call it, it’s clear that the space has reached maturity.

/s3.amazonaws.com/arc-authors/morningstar/a90ba90e-1da2-48a4-98bf-a476620dbff0.jpg)

Strategic beta, also called smart beta, is a form of active management. Strategic-beta exchange-traded funds are linked to indexes that make active bets, of varying types and degrees of magnitude, against the broad market-cap-weighted benchmarks that are their starting point—more purely passive “market” exposures. These wagers are embedded in the funds’ index methodologies, which are their active playbooks. But unlike conventional active managers, strategic-beta funds cannot make adjustments. After the play has been called in the huddle, there is no option to call an audible. With respect to the ongoing implementation of the strategies built into their benchmarks, they are strictly passive.

In September 2014, Morningstar introduced its naming convention and taxonomy for the fast-growing universe of strategic-beta exchange-traded products, or ETPs. In our latest report, A Global Guide to Strategic-Beta Exchange-Traded Products, we provide an update on the state of the global strategic-beta ETP landscape, framed using our latest strategic-beta and index attributes, which were launched in Morningstar's global database in the fourth quarter of 2018.

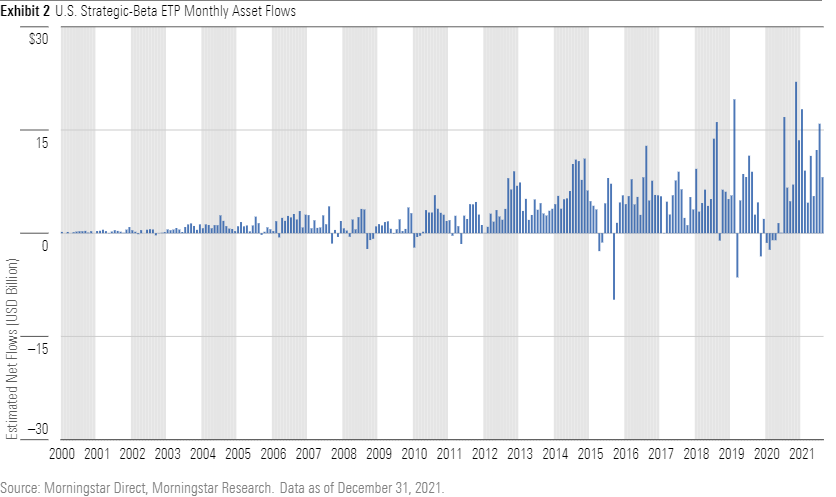

Over most of the past decade, the strategic-beta space grew more rapidly than the broader ETP market. Strategic-beta ETPs' growth has been driven by new cash flows, new launches, and the entrance of new players. However, more recently, these products' market-share gains have stalled.

This market segment has matured. The pace of net new inflows has stabilized. The number of strategic-beta ETPs worldwide declined on a year-over-year basis for the first time ever in 2020, as closures outnumbered new launches. In 2021, the global strategic-beta ETP menu added just 12 net new products, representing 0.9% growth versus the end of 2020. Meanwhile, these ETPs' fees have been squeezed. As the strategic-beta ETP landscape has settled, the asset management industry has moved on to build momentum behind new product ranges. Environmental, social, and governance investing, actively managed ETFs, and thematic funds now hog the spotlight.

A Look at the U.S. Landscape

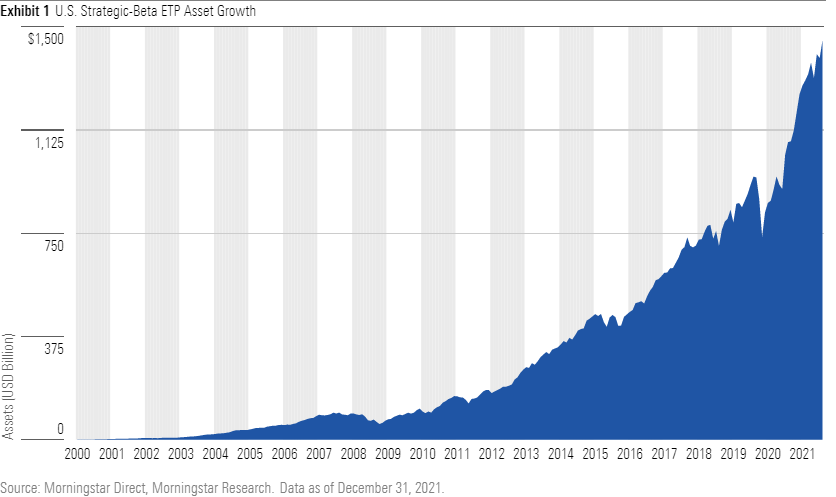

The United States is home to far and away the largest and most diverse stable of strategic-beta ETPs. The U.S. market accounts for 46% of the total number of strategic-beta ETPs, which together account for 88% of global strategic-beta ETP assets. This should come as little surprise given the overall size and maturity of the U.S. asset-management and financial-services industries. The first generation of strategic-beta ETPs came to the U.S. market in May 2000. IShares Russell 1000 Growth ETF IWF and iShares Russell 1000 Value ETF IWD were not only the first but remain two of the five largest strategic-beta ETPs. These funds represented “first-generation” strategic beta, introducing systematic style tilts to a market that was already well versed in a style-based approach to equity investing. Fast forward more than 20 years to Dec. 31, 2021, and strategic-beta ETPs numbered 622 and had collective assets of $1.45 trillion.

Morningstar

Grow With the Flow

Growth in strategic-beta ETPs has been driven primarily by new adopters across the investor spectrum, ranging from individuals to state pension funds. Approximately 54% of the aggregate growth in strategic-beta ETP assets dating back to May 2000 has come from net new inflows, while the remaining 46% reflects asset appreciation. In many ways, the U.S. market was well primed for strategic beta. The Morningstar Style Box had popularized the concept of style investing among U.S. investors by the time the first strategic-beta ETPs were launched in 2000. At that time, ETFs had been around for about seven years, though they were still novel to many investors and being used predominantly as trading vehicles. Also, within the advisor space, there were pockets of familiarity with the concept of factors owing in part to a rapidly growing and loyal army of Dimensional Fund Advisors[1] converts who were well versed in size, value, and momentum.

Morningstar

Roll Out the Betas

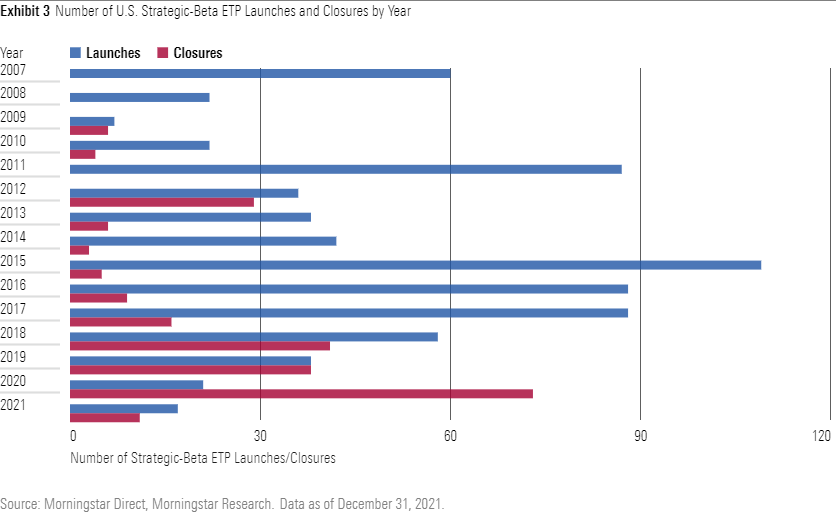

The first generation of strategic-beta ETPs delivered straightforward style tilts. Subsequently, there was a flurry of launch activity from 2005 to 2007, as strategic-beta-focused ETF providers rolled out full families of more-complex strategies. These included Invesco's (then known as PowerShares) roster of Dynamic and RAFI funds, WisdomTree's suite of dividend-screened/weighted funds, and First Trust's AlphaDex lineup. New launch activity hit a lull from 2008 to 2010 thanks to the global financial crisis but picked up once again in 2011 as providers moved to cover new bases (low-volatility strategies, for example).

New launches accelerated in 2015, and from 2015 through 2017 a total of 285 new strategic-beta ETPs were launched, representing 46% of the 622 products that were on the menu as of the end of 2021.

New product launches have since slowed considerably. There were just 17 new strategic-beta ETPs rolled out in the U.S. in 2021, representing a 19% year-over-year decline in new launches and an 84% decline from the 2015 record. While launches have slowed, closures have accelerated. In 2020, 73 strategic-beta ETPs were closed. In 2021, another 11 were liquidated. We view the slowdown in launches and the concurrent uptick in closures as clear signs that the menu was—and likely still is—oversaturated.

Morningstar

Simple Tastes

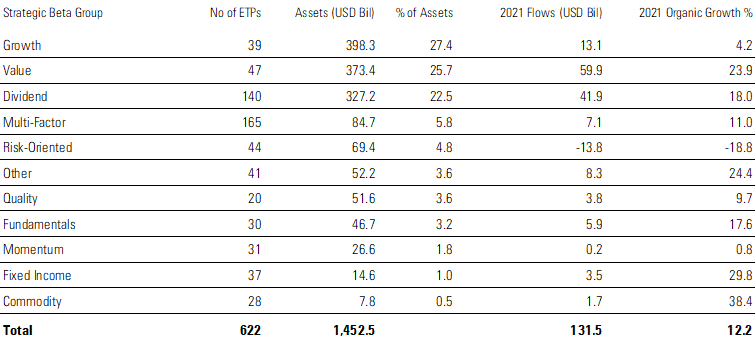

While complexity has been on the rise, investors' preferences remain plain-vanilla. Classifying the current roster of U.S. strategic-beta ETPs according to their strategic-beta groups shows that ETPs offering exposure to straightforward strategies (value, growth, dividend-screened/weighted) account for about 76% of strategic-beta ETP assets. Dividend strategies have proved particularly popular in the context of a yield-starved investment environment and investors who are placing a greater emphasis on investment income as they move from the accumulation stage of their investment lifecycle to the decumulation stage.

Funds belonging to Morningstar's Value strategic-beta group claimed the top spot in the flows league table in 2021, as they brought in $59.9 billion in new money. This was their second straight year on top—likely evidence that investors are betting on a turn of fortune for value stocks. Continued outflows among ETPs belonging to the Risk-Oriented strategic-beta group are also noteworthy. Low-volatility ETFs, which call the Risk-Oriented group home, had raked in tens of billions in new flows in recent years. In 2020, this group witnessed $13.2 billion in outflows—equating to an organic growth rate of negative 15%. Another $13.8 billion fled these funds in 2021, equating to an organic growth of nearly negative 19%. Investors had flocked to these funds as a means of maintaining equity exposure while reducing their portfolios' sensitivity to movements in the stock market. Some combination of disappointing performance through the early-2020 market melee and a broader rotation into value strategies were likely contributors to this exodus.

Exhibit 4: Ranking of U.S. Strategic-Beta ETP Assets by Strategic-Beta Group

Morningstar

Source: Morningstar Direct, Morningstar Research. Data as of Dec. 31, 2021.

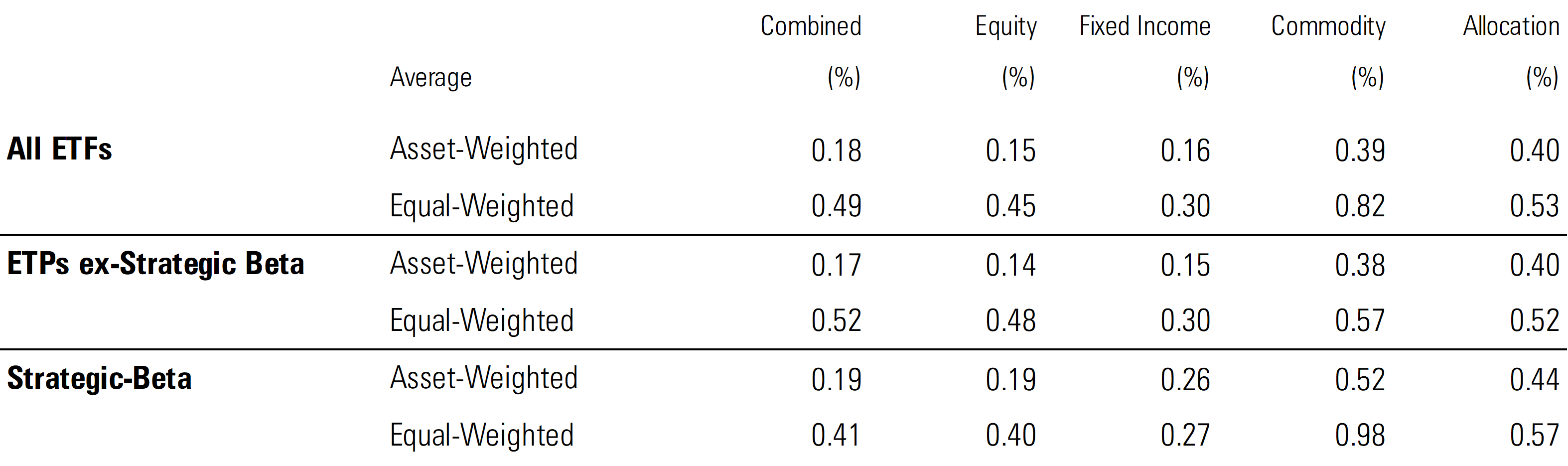

Keeping an Eye on Expenses

The fees levied by strategic-beta ETPs are, on average, competitive with those charged by the ETP field at large as well as the universe of ETPs excluding strategic beta. Of course, fees should be considered on a case-by-case basis. For example, Schwab U.S. Broad Market ETF SCHB, which tracks the market-capitalization-weighted Dow Jones U.S. Broad Stock Market Index, charges an annual fee of just 0.03%. Schwab Fundamental U.S. Broad Market ETF FNDB, which tracks the Russell RAFI US Index, levies a fee of 0.25%—a much higher hurdle relative to its more-ordinary sibling.

In aggregate, it is clear that across all three groupings—all else equal—investors prefer less pricey fare, as indicated by the fact that the asset-weighted average expense ratios tend to be lower than the simple averages. With that said, there are clearly some outlying ETPs that charge fees comparable to those of active managers. Investors should take extra care to assess whether such tolls are justifiable for an index-tracking product.

Among the 549 strategic-beta ETPs that have reported annual report net expense ratios for their 2020 and 2021 fiscal years to Morningstar's database, 105 (19%) saw their fees decrease during their 2021 fiscal year. The median decline in fees among this group was 0.01%. Meanwhile, 35 (6%) strategic-beta ETPs saw their fees inch higher, by a median level of 0.03%. The toll taken by the remaining 409 (74%) products remained unchanged. We expect that fees for strategic-beta ETPs will continue to trend lower with time.

Exhibit 5: U.S. Fees Under the Microscope

Morningstar

Source: Morningstar Direct, Morningstar Research. Data as of Dec. 31, 2021.

[1] As Dimensional Fund Advisors' funds do not track indexes by mandate, we exclude them from our definition of strategic beta. That said, the factors the firm sets out to exploit, the systematic manner in which it sets out to exploit them, and the fact that most of its funds levy low fees relative to peers make them—and other similar strategies from their competition—close cousins.

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Morningstar, Inc. does not market, sell, or make any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

/d10o6nnig0wrdw.cloudfront.net/07-25-2024/t_56eea4e8bb7d4b4fab9986001d5da1b6_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/BU6RVFENPMQF4EOJ6ONIPW5W5Q.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/a90ba90e-1da2-48a4-98bf-a476620dbff0.jpg)