How Do Alternatives Fit Into a Diversified Portfolio?

It depends on the strategy.

/s3.amazonaws.com/arc-authors/morningstar/bdf88cbd-d3d8-4661-b946-d09f9ffe196b.jpg)

In our recently published 2022 Diversification Landscape report, we took a deep dive into how different asset classes performed in the past couple of years, how correlations between them have changed, and what those changes mean for investors and financial advisors trying to build well-diversified portfolios.

Investors seek out alternative strategies to reduce drawdowns, seeking a wider breadth of risk factors or asset classes, and for more portfolio stability. In eight out of the past 10 calendar years, all seven alternative Morningstar Categories underperformed the Morningstar US Market Index, often by substantial margins.

However, in periods of intense market selloffs like the one seen in January, all seven alternatives categories lost less than the Morningstar US Market Index, and in some cases delivered positive returns. Overall, most alternative strategies have shown significantly less downside risk than broad equity market benchmarks.

Something Different From Stocks and Bonds

Morningstar defines these strategies based on their ability to modify, diversify, or eliminate traditional market risks. There is considerable variation between strategies, though, and identifying appropriate benchmarks is tough. For that reason, we used fund categories as proxies for the most common strategies. Of note, Morningstar revised its classification definitions for alternative strategies in April 2021.

Alternatives are classified as diversifiers, with the most common being equity market neutral, event-driven, and relative value arbitrage. The options-trading and multistrategy categories are considered diversifiers as well. These incorporate various traditional market risk factors found in equities, alongside nontraditional or alternative risk factors/betas, to offer a more diversified source of long-term returns. Nontraditional betas include factors such as carry, momentum, and trend. Because these factors are often linked with traditional risk factors, they often don't protect capital during market crashes.

Equity market-neutral, event-driven, and relative value arbitrage strategies typically have little to no sensitivity to moves in equity markets. In all three cases, they tend to trade securities both long and short against each other rather than trading in line with overall market moves.

Those strategies defined as opportunistic--macro trading and systematic trend--tend to focus on absolute returns, meaning they aim for positive returns in all markets and focus more on capital preservation. Managers of these strategies move in and out of long and short positions as opportunities arise. Opportunistic funds tend to lose less in drawdowns but also come with more complexity. Sometimes these managers bet the market will continue moving in the same direction, sometimes they wager it won't, and they often switch or hedge their bets. They can get caught out of step with their expectations for markets, so they often use sophisticated risk-management systems to manage their myriad exposures.

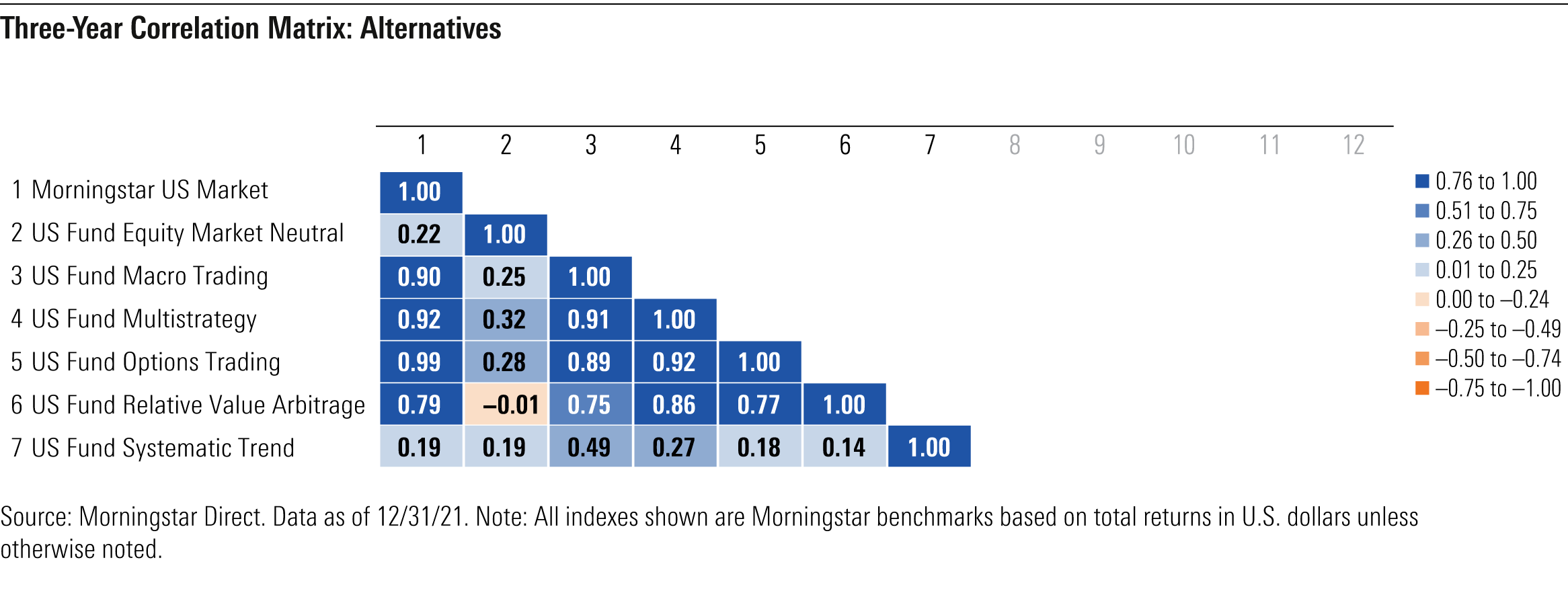

The 2021 Correlation Profile

Equity markets remained buoyant through most of 2021, and strategies such as macro trading, multistrategy, and options trading--all of which align to broad market movements--were closely correlated with the Morningstar US Market Index. These equity-sensitive portfolio offerings showed trailing three-year correlations of at least 0.90 (modestly higher than the previous year). Relative value arbitrage and event-driven strategies, both of which are equity strategies that tend to differ from the prior trio given their more concentrated and idiosyncratic investments, produced trailing three-year correlations of roughly 0.8. Equity market neutral and systematic trend, whose 0.2 three-year rolling correlations register as weakly positive, provided the most compelling opportunities for portfolio diversification.

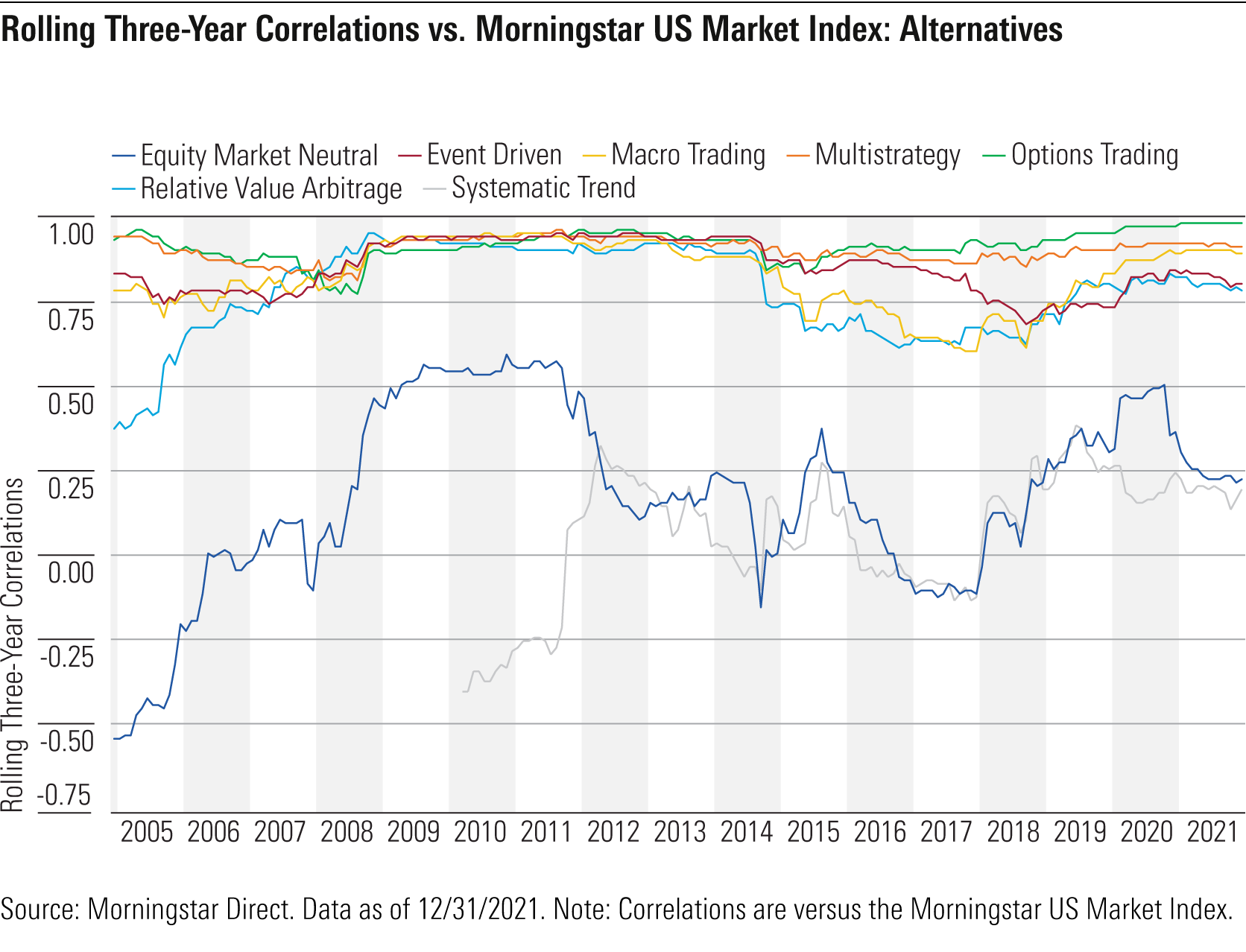

Longer-Term Trends

Over longer periods, most alternative categories have shown close correlations with equities but arguably very low levels of equity beta. This means that the returns of these alternatives categories are not primarily driven by moves in the equity market. Equity market neutral, by its category definition, has an equity beta of 0.3 or less, and so we'd expect to see little equity market dependency. Systematic trend obtains its returns by following market trends across commodities, currencies, government bonds, interest rates, and equity indexes. It similarly benefits from its eclectic menu, resulting in low long-term betas and correlations.

Portfolio Implications

From a portfolio construction perspective, though, investors must remember that it is the impact of the low equity beta that has a stronger effect on portfolio performance than that of correlation. Despite trailing U.S. equities by a wide margin over the past decade, a 20% allocation to some types of alternatives would have improved risk-adjusted returns versus an all-equity or balanced portfolio. The strategies with the greatest market neutrality--event-driven, relative value arbitrage, and equity market neutral--all matched or increased the portfolio's Sharpe ratio. As mentioned above, most alternative strategies also reduced portfolio drawdowns compared with an all-equity portfolio.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/CGEMAKSOGVCKBCSH32YM7X5FWI.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LUIUEVKYO2PKAIBSSAUSBVZXHI.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/bdf88cbd-d3d8-4661-b946-d09f9ffe196b.jpg)