Does the 4% Guideline Rest on a Flawed Assumption?

In-retirement spending is often incredibly variable rather than static.

/s3.amazonaws.com/arc-authors/morningstar/66112c3a-1edc-4f2a-ad8e-317f22d64dd3.jpg)

Our recent research on safe retirement spending rates featured a flashy takeaway: Retirees who are using a fixed real withdrawal system on a balanced portfolio should start with withdrawals in the low 3% range, rather than the standard 4% guidance for starting withdrawals.

The reasoning is straightforward. The Morningstar Investment Management team expects stock and especially bond returns to be fairly modest over the next 30 years--a typical planning horizon for retirement--and they think the next 10 could be particularly weak. Given those low return inputs, our research concluded that new retirees would do well to start conservatively on the spending front. Taking a low starting withdrawal helps limit the damage if the retiree encounters a weak market environment early on in retirement; it leaves more of the balance in place to repair itself when the market eventually recovers.

The question is, does a system of fixed real withdrawals, which we used to underpin our baseline conclusions about sustainable in-retirement spending, reflect how people actually spend in retirement? Not necessarily. Financial advisors often note that the early years of their clients’ retirements are the high-spending ones, with lower spending later on. Data on aggregate retiree spending corroborate a downward-sloping pattern for retiree spending. Given that, retirees who want to put a finer point on their own withdrawal systems should think through how their own outlays may change over their retirement time horizon, as well as the implications for their starting withdrawal amounts.

What the 4% Guideline Says…and What People Really Do

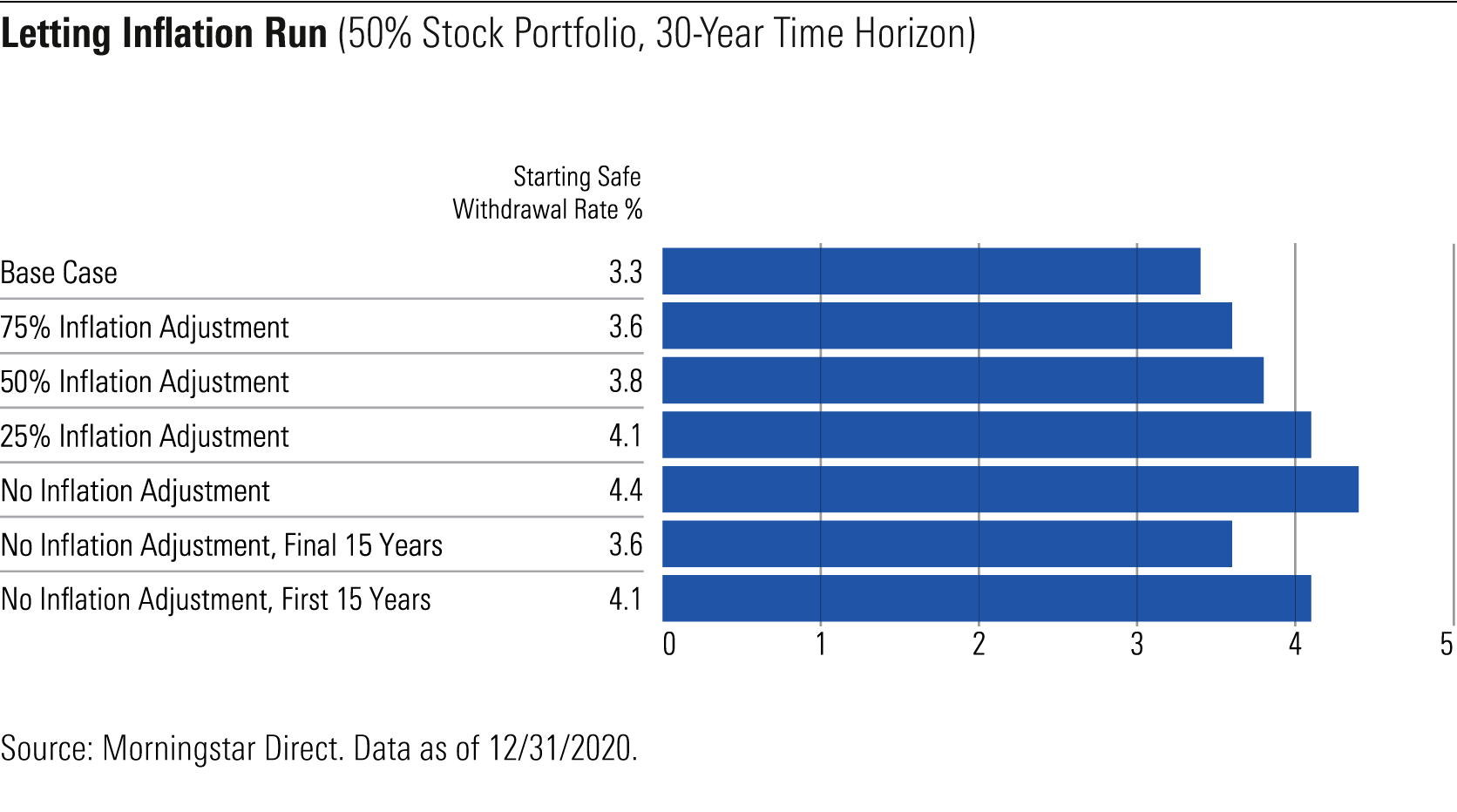

To start, it helps to outline the fixed real withdrawal system that underpins the 4% guideline and served as the baseline withdrawal system for our recent withdrawal-rate research. Such a system assumes that the retiree is seeking a stable standard of living--basically, the same portfolio “paycheck” throughout the whole of his or her retirement, with annual adjustments to boost that paycheck to accommodate rising prices. A 4% withdrawal on a $1 million portfolio would translate into a $40,000 year 1 withdrawal, $41,200 in year 2 (assuming 3% inflation), and so on. The “retirement paycheck” idea is appealing, especially for retirees who had little variability in their earnings, with the exception of periodic raises and cost-of-living adjustments, while they were working.

Yet aggregate retiree spending data point to a different pattern. Using data from the Bureau of Labor Statistics' Consumer Expenditure Survey, financial advisor Ty Bernicke noted that in-retirement spending generally decreases throughout the retirement life cycle. Retirees younger than 65 spent more than those age 65-74, and the 65- to 74-year-olds spent more than those over 75. Those downward reductions through time, according to Bernicke's research, more than offset inflation. That observation led Bernicke to conclude that many retirees are underspending in retirement, especially early on, because their withdrawal rates assume fixed real consumption, when instead later consumption patterns are more modest. Our research showed that retirees who don't adjust their withdrawals upward to fully account for inflation can take a higher starting withdrawal than would be the case for those who intend to take a full inflation adjustment.

Healthcare expenses are another crucial variable. Research from David Blanchett, now head of retirement research at PGIM and formerly head of retirement research for Morningstar Investment Management, concluded that retirement spending tends to be uneven through retirement. Much like Bernicke's research, Blanchett identified a downward slope in spending from the early to middle/middle-late years of retirement. But Blanchett also noted an uptick in spending toward the end of life, largely attributable to higher healthcare and long-term-care outlays.

How Retirees Can Fine-Tune It

Our withdrawal-rate research delved into how retirees can lift their lifetime spending by factoring in how the markets--and in turn their portfolios--have behaved. We explored simple tweaks to the fixed real withdrawal system as well as more complicated withdrawal systems that allow retirees to take more when the market is up in exchange for downward adjustments when it’s down.

But a concurrent line of thinking is also important: How does the retiree expect that his or her own needs and non-portfolio income sources, and in turn spending, might change over retirement? I like the idea of pre-retirees calibrating their inflows and outflows for retirement on a year-to-year basis, or perhaps in five-year increments if going year by year seems too onerous. Here are some of the key variables to consider.

Changes in Non-Portfolio Income Sources Demands on an in-retirement portfolio will depend, at least in part, on the retiree's non-portfolio income sources and how those might change over the retirement horizon. For example, many retirees have heeded the advice to delay Social Security filing if they can afford to do so, but the net effect of that approach is apt to be higher portfolio withdrawals before Social Security kicks in. Conversely, a retiree might find a bigger share of her needed income is coming through a pension early on in retirement, but if that pension isn't inflation-adjusted (as is the case with many private-sector pensions), higher portfolio withdrawals later in retirement may be inevitable. Finally, income from work is in the mix for more and more "retirees," or one spouse might continue to work while the other is retired. Earned income from work can lower portfolio spending for part of retirement, but probably not all of it.

Changes to Nest Egg Another consideration for portfolio spending is if the retiree expects his or her portfolio size to see a meaningful infusion--or outflow--in retirement. For example, the sale of a second home in year 10 of retirement, and the subsequent addition of the home-sale proceeds to the portfolio, would reduce portfolio withdrawals on a percentage basis thereafter. Big expected outlays, meanwhile, would obviously have the opposite effect.

Anticipated Lifestyle Changes Is the retiree anticipating any major lifestyle changes that would increase or decrease ongoing outlays? Sticking with the preceding example, the sale of a second home would not only provide a one-time cash infusion for the portfolio but also reduce ongoing carrying costs and in turn spending. Downsizing to a smaller home would have a similar effect. Retirees might also see their travel habits change. While early retirement might include a lot of exotic (and expensive) travel, travel later in retirement may be closer to home.

Capital Expenditures Retirement blogger Fritz Gilbert calls them "expected unexpected expenses": big-ticket, lumpy outlays, such as new cars or new roofs. While it's impossible to forecast each and every one of them, most experienced car owners and homeowners are able to come up with a decent approximation of when these expenses are apt to hit and how much they'll cost.

Healthcare Costs The finding that retiree spending often trends up in the later years of retirement because of healthcare-related spending has implications for retirement spending. For retirees whose insurance coverage allows for more out-of-pocket expenditures and/or those who do not have long-term-care insurance, it is reasonable to expect that spending could well trend up later in life. For retirees who are self-funding long-term care, it makes sense to segregate the long-term-care assets from spendable assets--for example, holding two years' worth of long-term-care expenses in a separate "bucket." (Two years is a typical duration for a long-term care need.)

On the other hand, retirees with ironclad healthcare and long-term-care plans that cover most out-of-pocket expenses wouldn’t need to incorporate higher spending later in life. For them, the risk of a negative healthcare spending shock is simply much less than is the case for the broad population of older adults.

Inflation

The specific rate of inflation that prevails over a retiree's life cycle--and when that inflation hits--is one of the key wild cards in the spending calculus. Retired financial planner Bill Bengen, the founder of the 4% guideline and a prolific retirement researcher, has argued that "sequence of inflation" risk is a risk factor on par with sequence of return risk--a string of very poor returns early on in retirement. If inflation hits early in retirement, he argues, that inflates all subsequent withdrawals. If a retiree is embarking on retirement in what appears to be a period of elevated inflation, that argues for taking a conservative tack on starting withdrawals.

Inflation averaged just 2.5% from 2000-10 and dropped even lower, to just 1.9%, from 2011-20. That provided a helping hand to retirees in that they needed to increase spending only modestly from year to year to maintain their standards of living. But retirees in other eras have not been so lucky. Inflation averaged 7.4% per year in the 1970s and more than 5% per year in the 1980s. More recently, inflation has jumped again, though the question of whether higher prices are here to stay or will prove more fleeting is obviously a huge topic of debate today.

The fact that inflation is also highly personal is an additional complicating factor and suggests that pre-retirees carefully consider their own spending, as well as their income sources, when deciding how to factor inflation into their withdrawal plans. In part because of higher inflation in the healthcare sector, along with the fact that older adults spend a higher percentage of their budgets on healthcare than do younger generations, inflation for older adults has historically run higher than the general inflation rate.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/GQNJPRNPINBIJGIQBSKECS3VNQ.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/EC7LK4HAG4BRKAYRRDWZ2NF3TY.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/JNGGL2QVKFA43PRVR44O6RYGEM.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/66112c3a-1edc-4f2a-ad8e-317f22d64dd3.jpg)