Sequence of Returns: Part II

The order of when things happen has implications for retirement savers, too.

/s3.amazonaws.com/arc-authors/morningstar/360a595b-3706-41f3-862d-b9d4d069160e.jpg)

In my last article, I explained why sequence-of-returns risk is one of the more underappreciated dangers of investing and showed how it can affect portfolio values during retirement. But how returns unfold over time also plays a role in planning for younger investors. In this article, I’ll explain why the sequence of returns is important and give some practical tips for dealing with it.

Background Sequence of returns is important because it can affect the dollar value of your portfolio if you're making contributions or withdrawals over time. In a nutshell, the periods when more dollars are invested will carry more weight in your overall results.

For investors already in retirement, that makes the first few years after retirement critically important. A negative sequence of returns can be detrimental for many years to come. For younger investors just getting started with saving, it works in reverse: The first few years carry less weight in your long-term results because your portfolio has fewer dollars to earn those returns. As your portfolio value increases over time, though, the sequence of returns becomes more important.

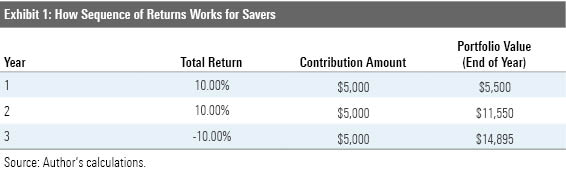

Let’s look at a couple of simple examples to see how this works in practice. If you invest $5,000 per year in a fund that earns 10% one year, 10% the second year, and negative 10% the third year, you’d end up with $14,895. That’s an internal rate of return of negative 0.35%--lower than the fund’s annualized return of 2.9% per year.

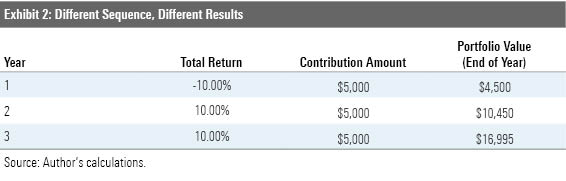

If the returns happen in a different order, you’d end up with different results. As shown below, the same $5,000 annual investment in fund that loses 10% the first year and then has positive returns of 10% in the second and third years ends up with a value of $16,995. Because more dollars are at work during the years when the fund had positive returns, the internal rate of return (about 6.4%) is actually higher than the fund’s total return.

Impact on Portfolio Value The basic math of total returns can work in your favor if you're a younger investor saving for retirement. Unless you're starting out with a significant portfolio balance from an inheritance or other personal assets, negative returns early on won't really hurt your long-term results, as shown in the table below.

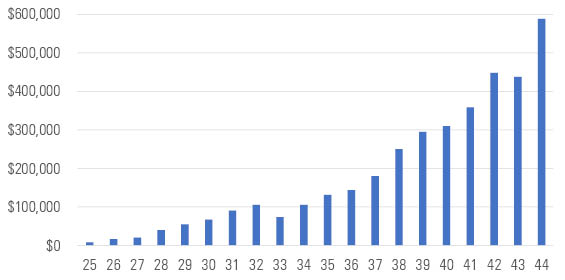

Exhibit 3: Long-Term Portfolio Value

Note: Portfolio values based on $10,000 annual contributions (not adjusted for inflation) and actual returns for S&P 500 starting in 2000. Source: Author's calculations.

For an investor who started contributing $10,000 per year to an all-equity portfolio just when the market headed into a three-year downturn beginning with the tech crash in 2000, sticking with the plan would have paid off. A young investor might feel like she’s throwing good money after bad after seeing two or three years of negative results. But over time, those early negative results have less impact. By simply continuing to invest $10,000 year in and year out (not adjusted for inflation) the investor would end up with close to $600,000 by age 44. Even after shifting part of the portfolio into fixed-income securities during her 30s and 40s (which would be a reasonable thing to do), she’d still have a strong start on saving for retirement.

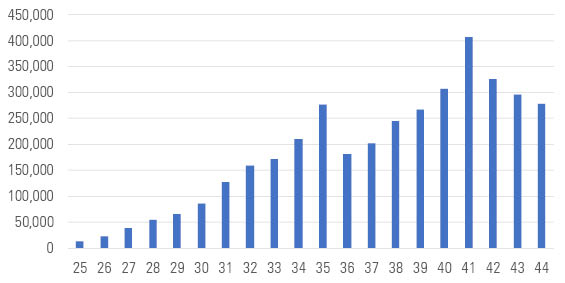

A negative sequence of returns can be more damaging if it happens closer to retirement. The table below illustrates what would happen with the same contribution amounts but a different sequence of returns. In this example, I used actual returns for the S&P 500 from 2000 through 2019, but in reverse order. With more dollars invested right before the three-year market downturn, the investor would end up with a portfolio value of about $278,000 at age 44. That’s not terrible, but less reassuring than the total in the previous example.

Exhibit 4: Long-Term Portfolio Value (Reversed Sequence of Returns)

Note: Portfolio values based on $10,000 annual contributions (not adjusted for inflation) and actual returns for the S&P 500 from 2019 to 2000 (in reverse order). Source: Author's calculations.

Mitigating the Risk There are a number of steps you can take to manage sequence-of-returns risk as a younger investor. Most important, don't get too discouraged if you start contributing to a 401(k) plan right before the market heads into an extended downturn. Time is your friend, and the odds are that sticking with your plan will eventually pay off. It's also important to keep any portfolio losses in perspective. They may be painful at the time, especially if your retirement portfolio represents all of the wealth you've managed to build up so far. But if you're planning for goals decades down the road, two or three years' worth of early losses won't really affect your odds of long-term success.

Checking in on your progress every few years is another wise move. Fidelity and other investment managers generally recommend setting a retirement savings target based on your age, aiming for a multiple of one times your salary by age 30, three times by age 40, and eventually 10 times by age 67. If you’re close to this target, keep doing what you’re doing. If you’re falling short, try to course-correct by boosting your savings rate as much as you can. If you’re ahead of the game, you can either build in a cushion or shift part of your savings toward other goals, such as investing for college or funding a taxable account.

Adjusting your asset allocation over time also plays a critical role in keeping sequence-of-returns risk in check. If you’re in your 20s, it makes sense to heavily favor stocks. Even a 100% equity allocation for retirement holdings can make sense for younger investors with a higher level of risk tolerance.

With age, though, you’ll want to adjust your portfolio mix to include more fixed-income securities, especially in the years leading up to retirement. Holding bonds as a buffer helps guard against losses in portfolio value during market downdrafts. Because equity values can take five years or more to recover from market downturns, a more balanced portfolio allocation can help mitigate the risk of a negative sequence of returns as you approach retirement.

Conclusion Sequence-of-returns risk involves a complex interplay of market returns, time, and cash inflows. For younger investors, though, it can represent both a hazard and an opportunity. Understanding how the order of when things happen can affect your portfolio value over time is an important first step toward taking control of your financial future.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/GJMQNPFPOFHUHHT3UABTAMBTZM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZYJVMA34ANHZZDT5KOPPUVFLPE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LDGHWJAL2NFZJBVDHSFFNEULHE.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/360a595b-3706-41f3-862d-b9d4d069160e.jpg)