September CPI Report Shows Downward Trend for Inflation Intact, if Bumpy

Inflation data seen giving Fed room to leave rates steady in November.

September’s Consumer Price Index report offered investors reassuring news on the outlook for inflation, even if the path lower isn’t a straight line.

The Bureau of Labor Statistics reported that the Consumer Price Index increased 3.7% in September compared with the same period a year ago. The monthly reading was a little higher than economists expected, but well below the June 2022 peak of 9.1%.

Core CPI, which excludes volatile food and energy prices, rose 4.1% over the past 12 months after climbing 4.3% in August. That’s in line with economists’ expectations. A steep runup in shelter prices was largely responsible for the uptick during September, even as other components of the core index, such as used car prices, trended down.

Despite core inflation’s slight acceleration, Morningstar senior U.S. economist Preston Caldwell says September’s reading is an “impressive reduction” compared with a year ago. Inflation remains above the Federal Reserve’s target level, but it’s widely expected that the central bank will keep interest rates unchanged at its next meeting in November.

“The overall inflation trend continues to point downward,” Caldwell says.

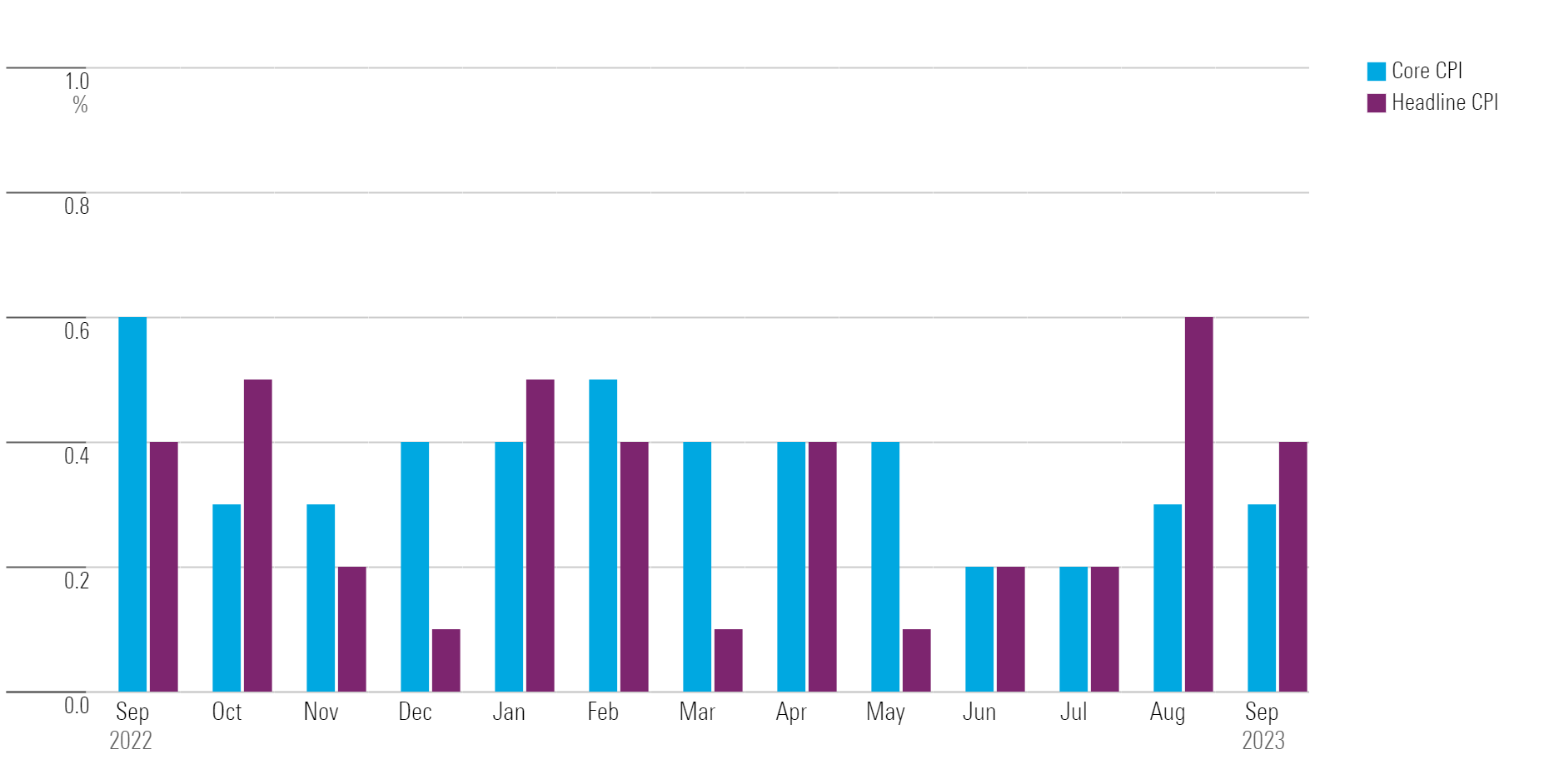

CPI vs. Core CPI

September CPI Report Key Stats

- CPI rose 0.4% for the month after falling 0.6% in August.

- Core CPI increased 0.3% after rising by the same amount in August.

- CPI climbed 3.7% year over year after rising by the same amount the prior month.

- Core CPI rose 4.1% from year-ago levels after increasing 4.3% in August.

Consumer Price Index

Housing Costs Push CPI Higher, But Gains Could Decelerate Soon

The index for shelter, which includes housing costs for both homeowners and renters, was the largest contributor to the monthly all-items increase. Shelter prices rose 0.6% on a monthly basis in September and 7.2% on an annual basis.

Caldwell points out that excluding shelter, core inflation has risen just 1.2% on an annual basis over the past three months. “In aggregate,” he says, “shelter prices are solely responsible for core inflation remaining above the Fed’s 2% target.”

Shelter prices provide a “rearview mirror” perspective, Caldwell says, meaning they’re a snapshot of economic conditions that have already come to pass, rather than a preview of what things might look like in the future.

“Assuming market rent growth doesn’t reaccelerate, which is likely given the continued expansion in housing supply, it is inevitable that the shelter component of inflation will fall back to normal,” Caldwell says. “We expect the deacceleration in shelter inflation to renew in coming months.”

Impact of Shelter on Core CPI

Gas Price Rise Slows

An increase in the gasoline index, which rose 2.1% on a monthly basis and 3.0% on an annual basis, also helped drive overall prices higher in September, though the impact was not as dramatic as it was in August. Energy prices overall rose 1.5% month over month but fell 0.5% year over year. In August, energy prices spiked 5.6% on a monthly basis.

Caldwell expects this deceleration to continue. “Headline inflation will be driven lower in coming months owing to lower gasoline prices,” he says, adding that gasoline futures prices have fallen roughly 20% since the middle of September.

Change in Selected CPI Components

Fed Likely to Hold Rates Steady in November

“We don’t think the minor uptick in core inflation will push the Fed to hike in its November meeting,” Caldwell says. Inflation is continuing to trend downward, and “the effect of the Fed’s prior rate hikes have yet to fully play out.” Rising bond yields could also lead to a tightening of financial conditions, Caldwell says, which could have the same effect as another rate hike.

In the bond market, 60.5% of investors expect the Fed to hold the federal-funds rate at its current target range of 5.25%-5.50% at its last meeting of the year in December, according to the CME FedWatch tool. Another 35.7% expect a 0.25% hike. A month ago, 55.2% of investors expected the Fed to hold steady, while 41.2% were anticipating a 0.25% hike.

Expectations for December 2023 Federal Reserve Meeting

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/PKH6NPHLCRBR5DT2RWCY2VOCEQ.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/GJMQNPFPOFHUHHT3UABTAMBTZM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZYJVMA34ANHZZDT5KOPPUVFLPE.png)