Recession or Not, There Will Be Pain

Investors and stock strategists are braced for a different kind of slump, but a slump nonetheless.

/s3.amazonaws.com/arc-authors/morningstar/ed88495a-f0ba-4a6a-9a05-52796711ffb1.jpg)

When is a recession not really a recession? When it’s a “rolling” recession.

A rolling recession occurs when different segments of the economy slump at different times, resulting in very low overall growth in gross domestic product output. By maintaining the barest minimum of growth and avoiding a sharp and prolonged economic contraction, rolling recessions sidestep being labeled as official recessions. Rolling recessions are also referred to frequently as “growth” recessions.

“It’s putting the best face on a recession,” explains Kenneth Kim, senior economist at KPMG, the multinational tax and accounting services firm. “There will be some growth in GDP output, but it will be so low that to businesses and households it will feel like a recession. The Fed is not done with raising rates and will continue to do so for the remainder of this year and into early 2023.”

Tough-Talking Fed

The term is gaining traction and rolling off the tongues of more and more investment managers and strategists since Federal Reserve Chair Jerome Powell recently warned in a short and uncharacteristically pointed speech at the annual Jackson Hole Economic Symposium of a "sustained period of below-trend growth" as the central bank continues to focus on bringing down stubbornly high inflation.

Powell dispensed with the notion of a soft landing and reiterated that the “overarching focus” of the Fed was to achieve price stability and meet its goal of a 2% inflation rate. Getting to that point will require more rate hikes, more job losses and “pain to households and businesses,” he said.

"Powell's use of the word pain can be viewed as code for recession," says Liz Ann Sonders, chief investment strategist at Charles Schwab SCHW. "It's possible there will be some version of a rolling recession."

“The best-case scenario is that inflation retreats and the labor market cools and that brings back a goldilocks economy,” she adds. “But that is a narrow needle to thread.”

Sonders notes that stocks continue to be in a bear market and economic growth is weak. At the same time, she anticipates corporate profits to weaken, the housing market to continue to soften and the labor market to deteriorate as the Fed actively works to beat back inflation.

"Growth is undoubtedly slowing," says Preston Caldwell, chief economist at Morningstar but he’s hesitant to say we’re in a recession or even suggest what kind of recession may lie ahead. He notes that it's "very unlikely" that the GDP drop in the first half represented an economic recession because it was driven by the "noisiest components" of spending, which was offset by other data points that showed growth. Caldwell believes the "risk of a recession will be most concentrated in 2023, when full-year growth hits a trough."

Stocks Sell Off on Fed’s More Restrictive Stance

Powell's speech led to a multiday, across-the-board selloff in the major stock market indexes, which ended August in the red. The start of September saw continued selling. Also pressuring stocks were remarks made by Loretta J. Mester, president of the Cleveland Federal Reserve Bank, to the Chamber of Commerce of Dayton, Ohio, in a speech called "Returning to Price Stability."

Said Mester: “My current view is that it will be necessary to move the fed-funds rate up to somewhat above 4% by early next year and hold it there; I do not anticipate the Fed cutting the fed-funds rate target next year.”

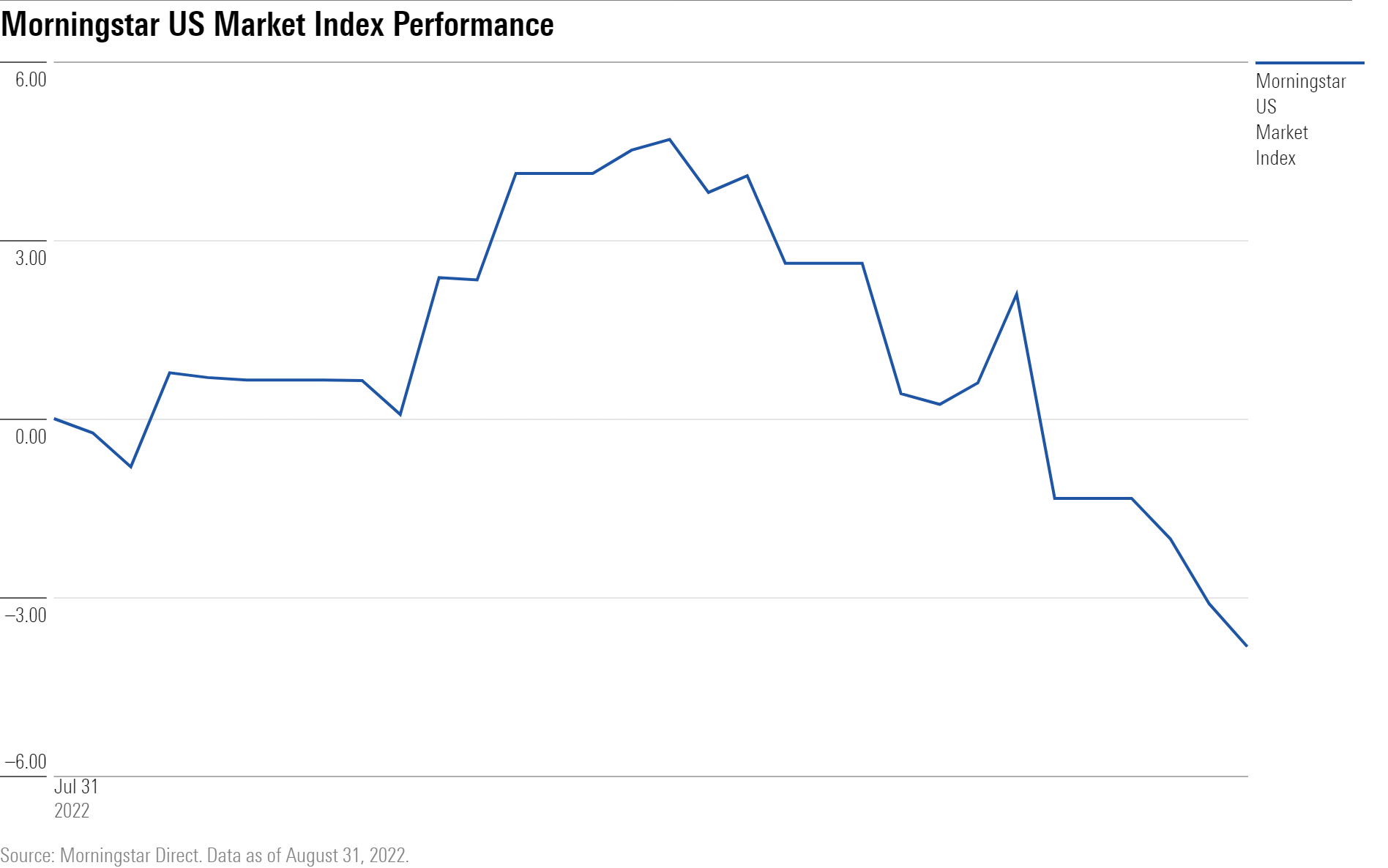

The Morningstar US Market Index fell nearly 4% in the month of August, losing 4.41% in the one-week period through Thursday. It is down 17.91% for the year to date.

Morningstar US Market Index Performance

“We’ve moved from a mollycoddling Fed to a tough-love Fed,” says Adrian Helfert, chief investment officer for multi-asset strategies at Dallas-based Westwood Holdings Group with about $12.1 billion under management. “We’re headed for an extended lower-growth environment that allows for a greater possibility of a rolling recession within industries. That should reduce the longer-term real growth rate of the economy, but a sharp contraction is unlikely because consumers are in good shape with less debt and higher savings.”

Such an environment will hurt corporate earnings, which make equities less attractive but should benefit high-quality corporate bonds, Helfert says.

Edward Yardeni, founder and president of Yardeni Research, a provider of global investment strategies and advisory services, in an Aug. 30 briefing called "Anatomy of a Rolling Recession" said he and his team consider the economy to have been in a "rolling recession since the start of this year." Yardeni says he sees it possibly continuing through the end of the year. He notes that real GDP fell slightly in the first half based on a supply shortage of new vehicles, recessionary conditions in the housing sector, and declines in capital spending on nonresidential structures in the commercial and health, power, communications, and manufacturing sectors. He tracks capital spending based on the regional business surveys conducted by the Federal Reserve's district banks.

On Sept. 1, the Institute of Supply Management released its monthly manufacturing purchasing managers index for August. The ISM M-PMI remained unchanged at 52.8, and its major components stayed above the 50 mark, indicating expansion, providing “confirmation of our economic outlook including a growth recession and moderating inflationary pressures,” Yardeni said.

Rolling or growth recessions are not common in the modern era, says Schwab’s Sonders. But “this cycle is incredibly unique,” because of the pandemic and pandemic-related disruptions that we are “still at the mercy of,” she says.

The 10-month recession stretching from April 1960 to February 1961 that led to then-Vice President Richard Nixon losing his presidential bid to John F. Kennedy is often referred to as a “rolling adjustment recession” because downturns hit several industries at different times. The auto industry, caught off guard by Americans’ new preference for foreign-made compact cars, suffered in particular as companies were forced to slash inventories and alter production.

The notion of a "growth recession" was first introduced by the late economist and former director of the National Bureau of Economic Research Solomon Fabricant in 1970 to describe a period when the economy grows ever so slightly amid a backdrop of rising unemployment, declining incomes, and production weakness. Not everyone bought into the concept. As the late columnist William Safire recounted in a 1984 piece in The New York Times, the economist Herbert Stein scoffed that a growth recession was the equivalent of calling a dog a "growth horse."

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/MQJKJ522P5CVPNC75GULVF7UCE.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZYJVMA34ANHZZDT5KOPPUVFLPE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/S7NJ3ZTJORFVLCRFS2S4LRN3QE.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ed88495a-f0ba-4a6a-9a05-52796711ffb1.jpg)