How Much Has the Market Benefited from Investor Optimism?

Measuring the effects of multiple expansion.

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

Reader Response

Last week’s column, “Why the Rich Have Become Richer,” argued that over recent decades, two developments have favored higher-income Americans. First, their salaries have outgrown the national average. Second, their stocks have boomed. The former claim went unchallenged, but several readers wondered about the latter. There's no question U.S. equities have thrived, but isn’t that largely because they have become more expensive? How would they have fared without that boost?

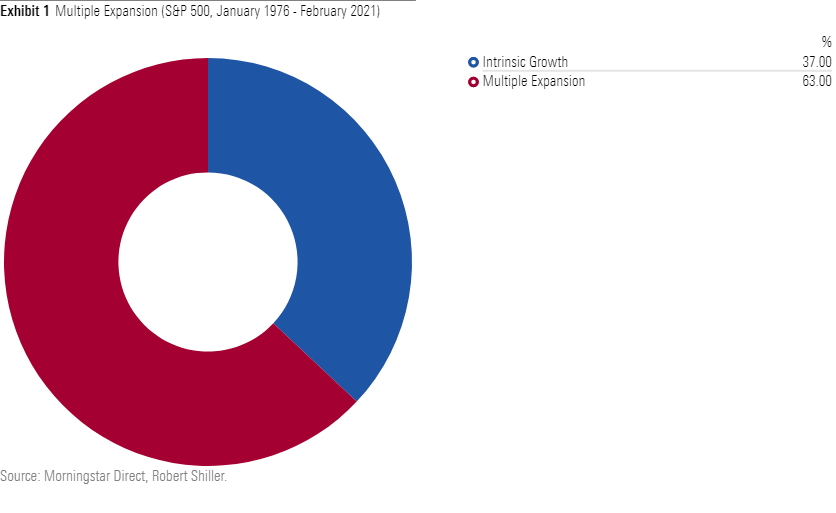

Your wish is my command. Per Nobel Laureate Robert Shiller's data, the companies in the S&P 500 traded at 11.8 times their earnings in January 1976, as opposed to 31.5 times in March 2021. Thus, 63% of the index's current value owes to multiple expansion. The S&P 500 has appreciated, for the most part, because today's investors pay more for the same dollar of earnings.

That was the readers’ objection. Stock gains have been exaggerated by investor optimism. One should discount that one-time effect when evaluating the future.

Giving 219%

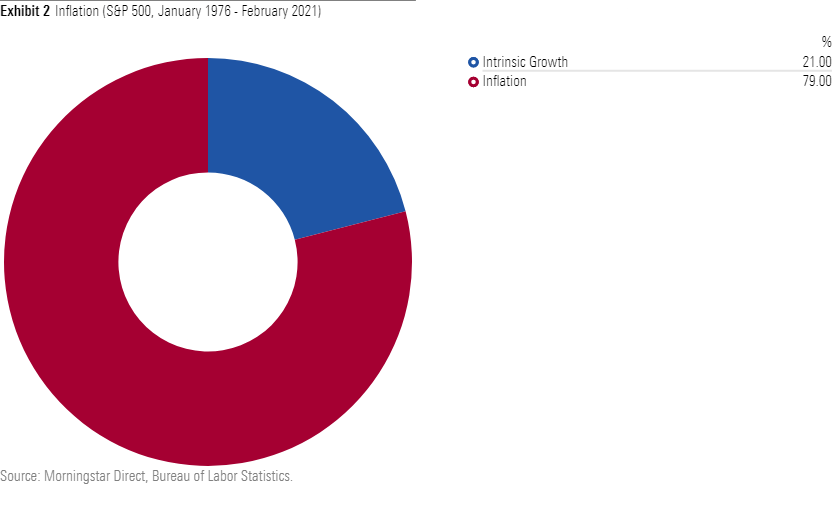

Fair enough. Let’s continue the analysis. Price/earnings ratios are not the only factor that affect stock prices. Another is inflation. Absent other changes, the value of the S&P 500 would nonetheless increase, because inflation would boost nominal earnings (in the same fashion that it does a loaf of bread). We can therefore measure what the cumulative effect of inflation has been on the price of the S&P 500, just as we did with the shift in price/earnings ratios.

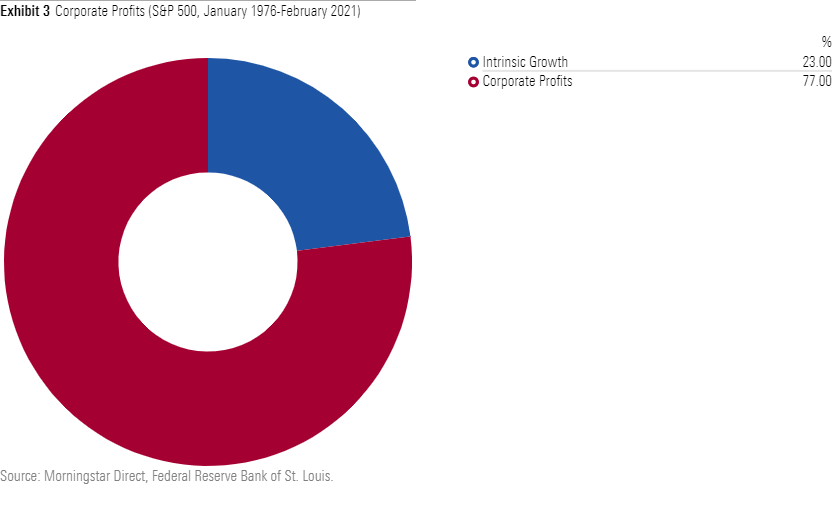

Curious. Not only did higher price/earnings ratios produce 63% of the index's appreciation, but inflation apparently contributed another 77%. And we haven't yet discussed corporate earnings. Real earnings did not in fact remain static; today's businesses are more profitable than those of 1976. Specifically, American companies have hiked their after-tax earnings by an inflation-adjusted 276%, meaning that profit growth caused 77% of the S&P 500's increase.

We have now accounted for 219% of the growth of the index’s value. How could that be? No doubt there is a name for this mathematic fallacy, but I don’t know it. However, I can provide an analogy. In 1790, the population of the founding 13 states was 3% of its current level. Today, those 13 states possess 28% of U.S. population. Thus, we can simultaneously argue, with equal accuracy, that 1) 97% of the country’s population growth has come from within its original borders, and 2) 72% of the country’s population growth owes to adding another 37 states.

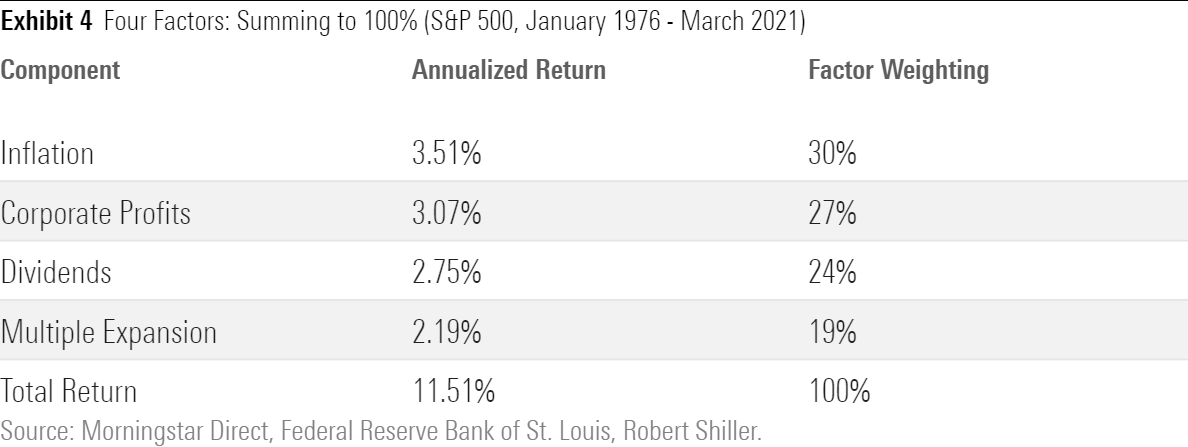

The 100% Solution

This will not do. Let’s eliminate this problem of ever-escalating percentages by forcing the answer to sum to 100%. We have already discussed the three items that determine the S&P 500’s price movement: 1) inflation, 2) corporate profits, and 3) change in the price/earnings multiple. For evaluating the index’s total returns, we must add a fourth factor: dividend payments. The table below depicts the S&P 500’s annualized total return from January 1976 through March 2021 (the final date for which corporate profits are available), along with the influence of each of the four factors.

Inflation was the largest cause. Its power, regrettably, is entirely illusory. If the S&P 500 had gained 50% annually, with inflation averaging 51%, then stock-market investors would have gained 9,292,433,624% over those 45-plus years, while shedding 26 cents on every dollar of their purchasing power. Talk about a Pyrrhic victory! Fortunately, although inflation led, it did not dominate, as the index's real annualized return was an outstanding 8.01%.

Of that amount, corporate-profit growth chipped in just over 3%, dividends slightly less, and multiple expansion 2.19%. In other words, although from one perspective higher price/earnings ratios caused 63% of the index’s increase in value, from another, more useful angle they contributed only 19% of total returns. Of course, when I wrote “only” I did not mean to dismiss the objections. Removing one part in five from the S&P 500’s total returns would have slowed the stock market’s party. However, it would not have negated my argument: Equities, not salary growth, were the most powerful force for wealth creation.

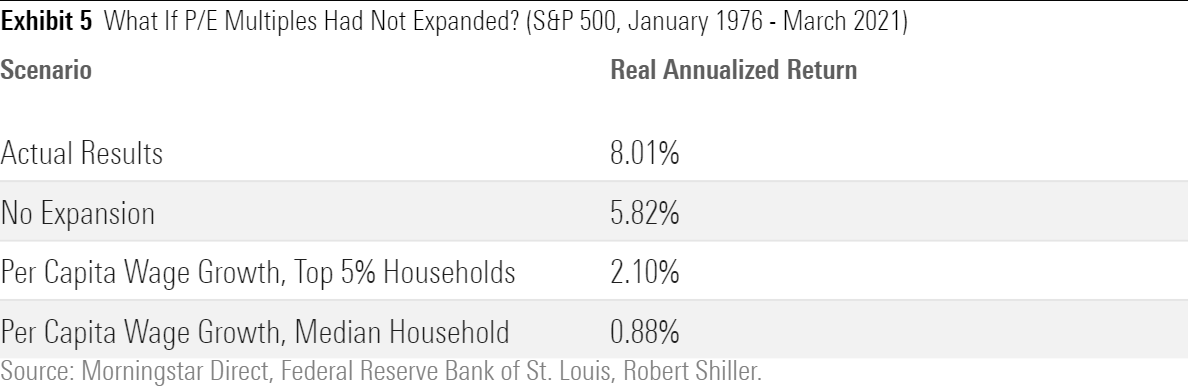

What If?

The final table supports that statement. It shows: 1) the S&P 500’s actual real total returns; 2) what its performance would have been would the index’s price/earnings multiple remained at 11.5*, 3) the growth in real per-capita income for top 5% households, and 4) the equivalent figure for median households. Even without the benefit of increased popularity, equity returns easily outstripped all varieties of wage growth.

(*This claim is not strictly correct. If stock prices had been lower, then equity investors would have received additional shares when reinvesting their dividends. Consequently, their future dividend receipts would have increased, which in turn would have permitted them to buy more shares, and so forth. However, as this detail strengthens rather than weakens my argument, I will set it aside.)

The analysis is incomplete. We have learned that equities would have fared well without their tailwind, but we cannot say how they would have performed had they faced an outright headwind. However, although those results can not be forecast precisely--even if we knew future price/earnings ratios, we could not predict either corporate-earnings growth or dividend schedules--they can be estimated to reasonable accuracy. An upcoming column will do just that.

John Rekenthaler (john.rekenthaler@morningstar.com) has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar's investment research department. John is quick to point out that while Morningstar typically agrees with the views of the Rekenthaler Report, his views are his own.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/GJMQNPFPOFHUHHT3UABTAMBTZM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZYJVMA34ANHZZDT5KOPPUVFLPE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LDGHWJAL2NFZJBVDHSFFNEULHE.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

{kind=link}