Mutual fund share classes covered

Morningstar ratings

With a long track record of helping bring clarity to the investing world, our rating systems cut through complexity to help investors and financial professionals make well-informed decisions.

Morningstar ratings are a reliable, easy first step in the process of evaluating different investments. We cover a wide range of areas—funds, stocks, portfolios, and credit—and will work to continue innovating in response to investor demand and evolving market conditions.

Researchers across stocks, credit ratings, managed investments, and more

Public companies covered

Fund and portfolio ratings

Morningstar Rating for Funds

Evaluates a fund’s past risk-adjusted performance compared to its peers. The quantitative star rating identifies funds that are worthy of further research.

Morningstar Medalist Rating

Analyzes a fund’s ability to outperform its peers or a relevant index on a risk-adjusted basis. The forward-looking, qualitative and quantitative analysis simplifies the search for managed investments.

Stock ratings

Morningstar Rating for Stocks

Assesses a stock’s price compared to our estimate of its worth, adjusted for uncertainty. The quantitative star rating seeks to identify stocks that are undervalued.

Morningstar Economic Moat Rating

Indicates a firm’s potential to sustain excess profits over a long period of time. This qualitative and quantitative analysis seeks to identify competitively-advantaged companies.

ESG ratings

Morningstar Sustainalytics ESG Risk Rating

Measures a company’s exposure to and management of material environmental, social, and governance risks. The rating combines qualitative and quantitative assessments.

Morningstar ESG Risk Rating for Funds

Measures how well a fund’s holdings manage material environmental, social, and governance risks relative to its peer group, summarizing qualitative assessments into a quantitative rating.

Credit ratings

Morningstar DBRS Credit Rating

Forward looking opinions about credit risk which reflect the creditworthiness of an issuer, rated entity, security, and/or obligation.

Investing frameworks and tools

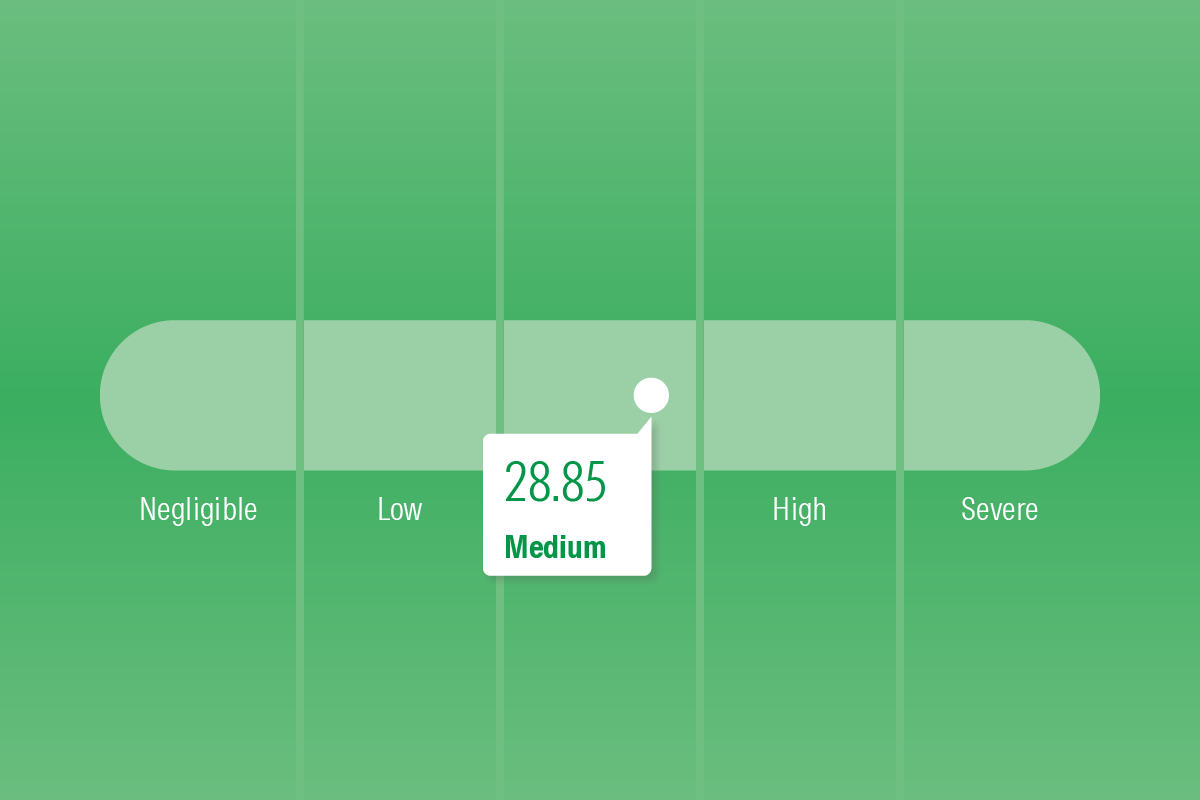

Portfolio Risk Score

Measures the estimated risk level of an investment portfolio. The quantitative tool can help an advisor match a portfolio to an investor’s risk profile.

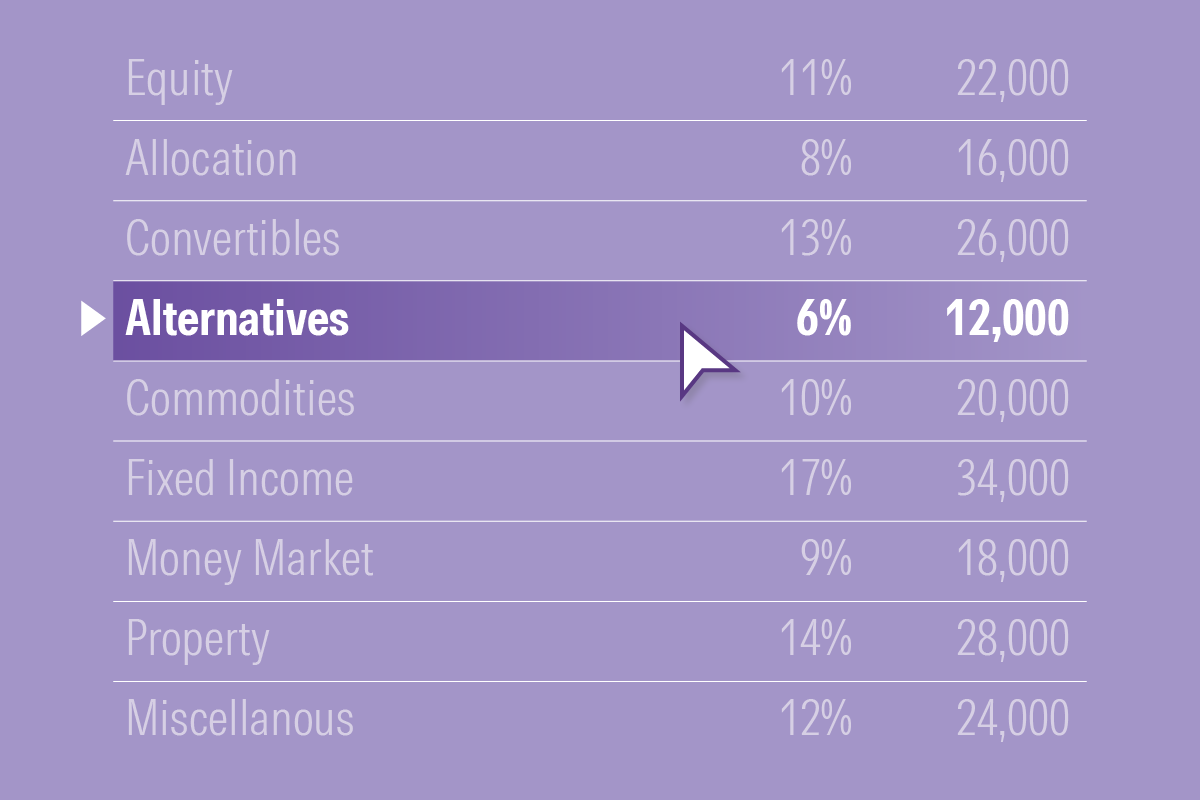

Morningstar Categories

Classifies portfolios by asset-class, risk, return, and behavior profiles of their holdings. The qualitative system shows similar investments by region.

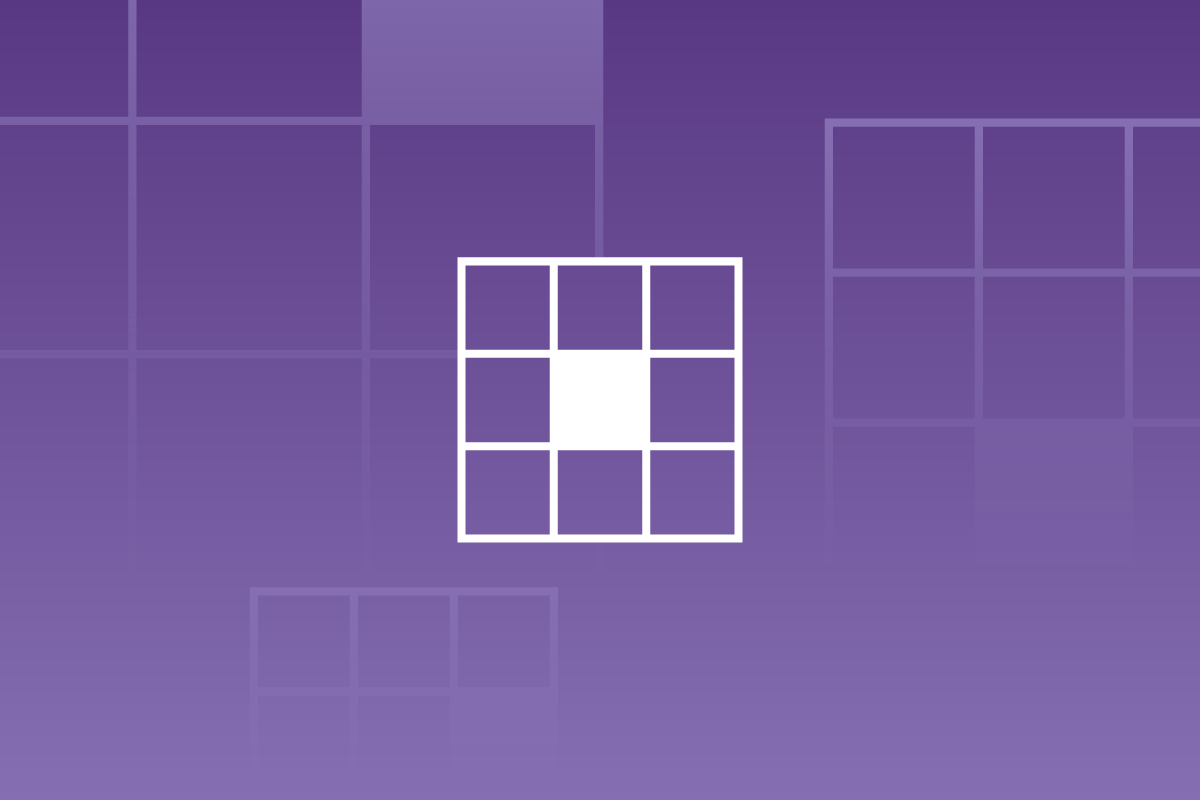

Morningstar Equity Style Box

Visually represents fund characteristics based on its stock holdings. The quantitative tool reveals the true positioning of a fund.

PitchBook VC Exit Predictor

Examines if a venture-backed company is headed toward a successful IPO or acquisition. The AI-powered, quantitative tool creates exit predictions that help identify potential investment opportunities.

PitchBook Manager Performance Scores

Analyzes the performance of private capital fund families by strategy compared to their peers. The quantitative approach evaluates the track record of fund managers.

PitchBook Portfolio Forecasting

Models cash flows of private market funds to help inform portfolio construction. The quantitative tool helps streamline investment decision-making.

PitchBook Private Capital Return Barometers

Assesses the current return environment for private market funds. The quantitative approach helps investors gather performance insights faster, before quarterly returns are available.

Frequently asked questions

All investments involve risk, including the loss of principal. There can be no assurance that any financial strategy will be successful.

Morningstar, Inc.'s general copyright disclosure includes the following:

The information, data, analyses and opinions contained herein (1) include the confidential and proprietary information of Morningstar, (2) may not be copied or redistributed, (3) do not constitute investment advice offered by Morningstar, (4) are provided solely for informational purposes and therefore are not an offer to buy or sell a security, and (5) are not warranted to be correct, complete or accurate. Except as otherwise required by law, Morningstar shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, this information, data, analyses or opinions or their use.

All statistics above are sourced from Morningstar’s 2024 Annual Report with data as of December 2024.