Sustainable Fund Flows Dip for the Quarter but Peak for the Year

Passive funds are dominating flows but active funds still hold the majority of assets.

/s3.amazonaws.com/arc-authors/morningstar/987376c2-20a0-406b-b3ec-df530324b39c.jpg)

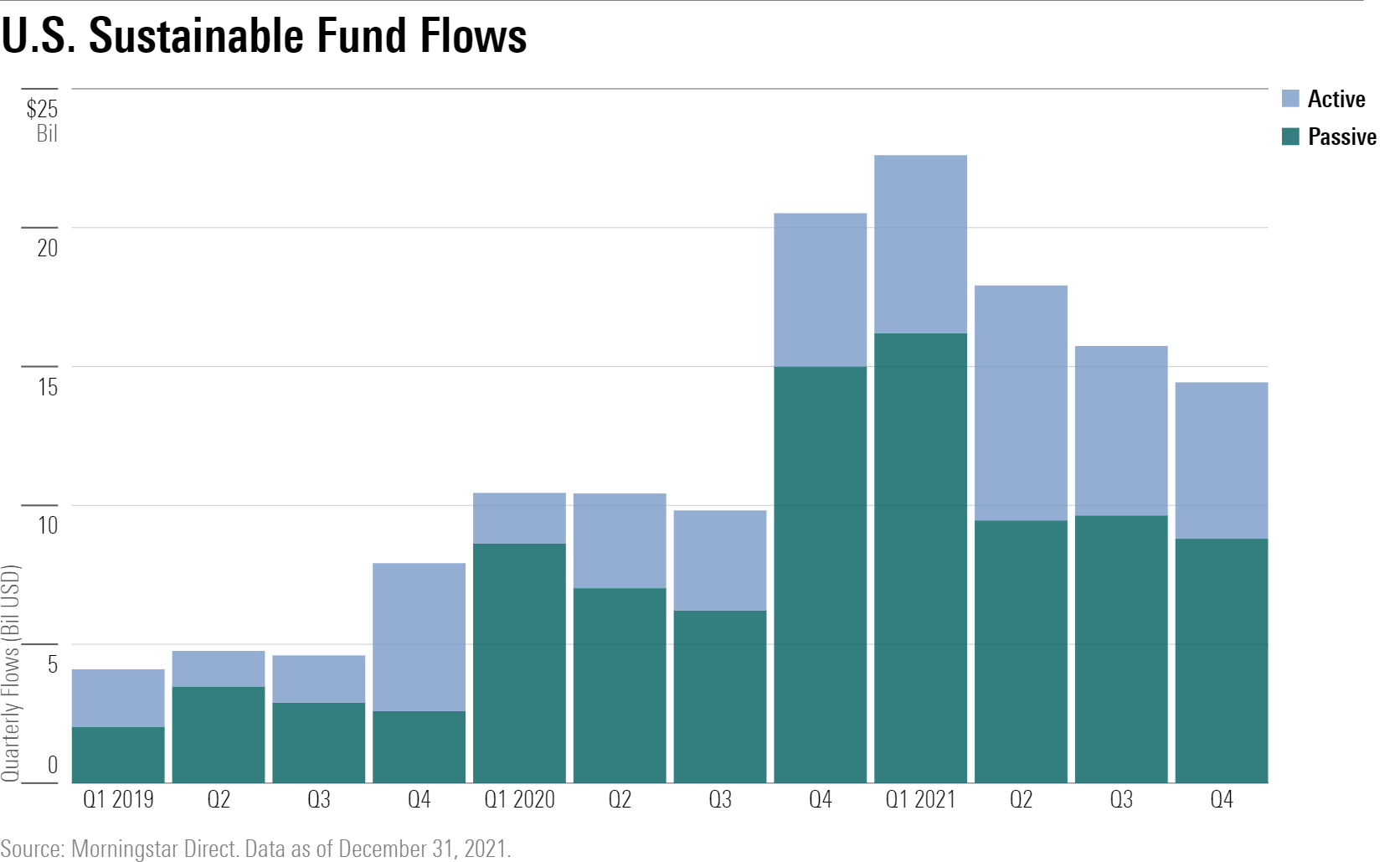

In previous years, the fourth quarter was the anchor of the race for sustainable fund flows, but flows in the fourth quarter of 2021 hit their lowest point of the year at $14 billion. By contrast, sustainable flows peaked in the first quarter at $22 billion.

On average in 2021, sustainable funds attracted $17.3 billion in net flows each quarter, topping the $12.8 billion average seen in 2020 and leading to another record-setting year. In total, U.S. sustainable funds netted nearly $70 billion for the year, a 35% increase over 2020’s high-water mark.

The full analysis can be found in our quarterly sustainable flows report.

Passive Funds Continue to Dominate Sustainable Fund Flows

The chart below shows that sustainable passive funds still dominated their active peers, albeit by a smaller degree than in the past. Passive funds attracted net inflows of $8.8 billion for the period. This represented 62% of all U.S. sustainable flows, compared with the record 83% in the first quarter of 2020.

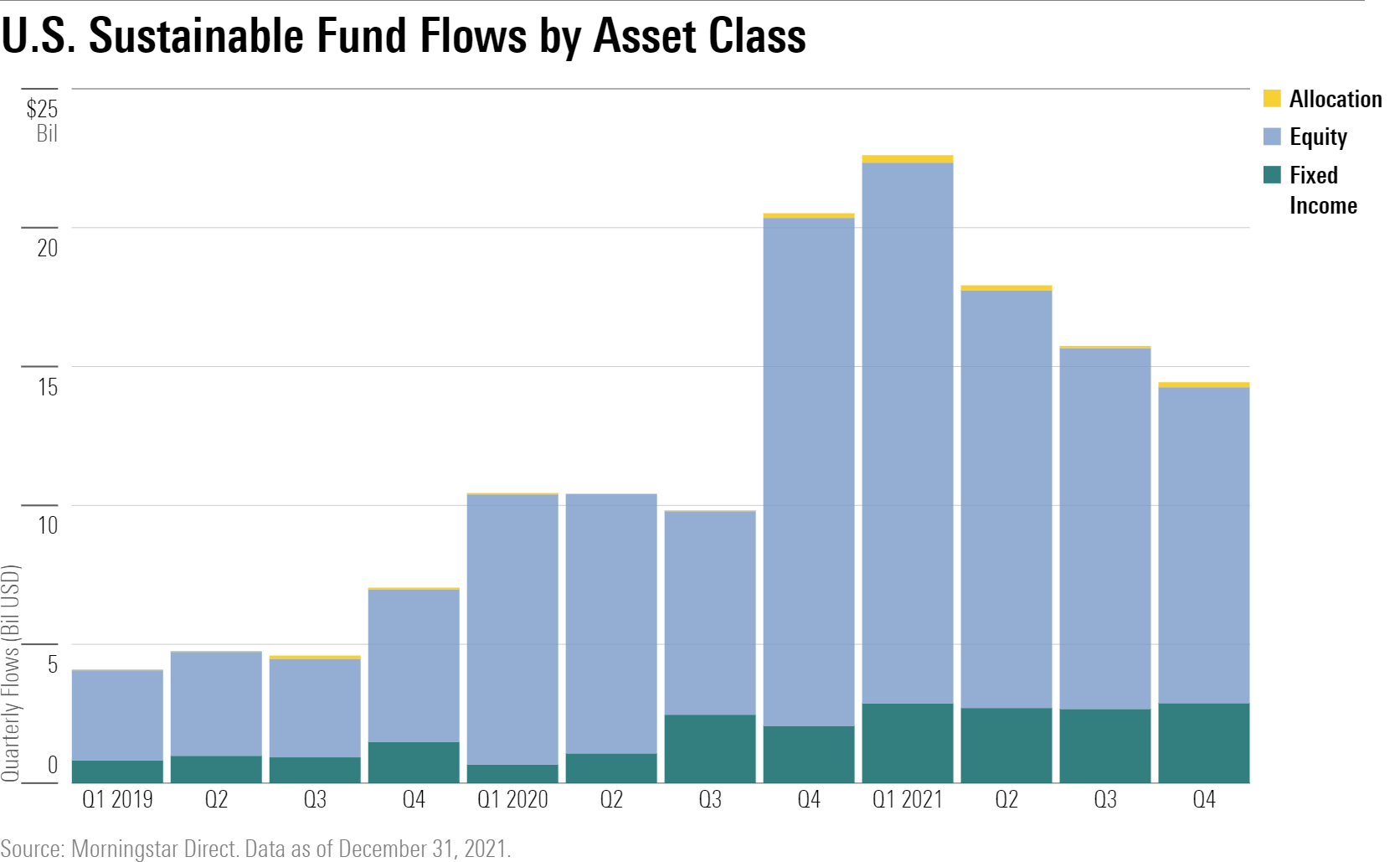

Equity funds made up the lion’s share of flows, as they typically do. In the fourth quarter, equity funds attracted $11.4 billion, or 79% of all sustainable fund flows.

Even so, the chart below shows that flows into sustainable fixed-income funds have been growing steadily. They crossed the $2 billion threshold for the first time in the third quarter of 2020, and they have stayed above that mark since.

In the fourth quarter of 2021, they netted nearly $2.9 billion, a new record for the asset class. The best-selling sustainable fixed-income fund was Invesco Floating Rate ESG AFRAX, which attracted nearly $316 million for the period. In fact, Invesco Floating Rate ESG was the top-selling sustainable fixed-income fund in all of 2021, knocking TIAA-CREF Core Impact Bond TSBIX out of first place for the first time since 2013.

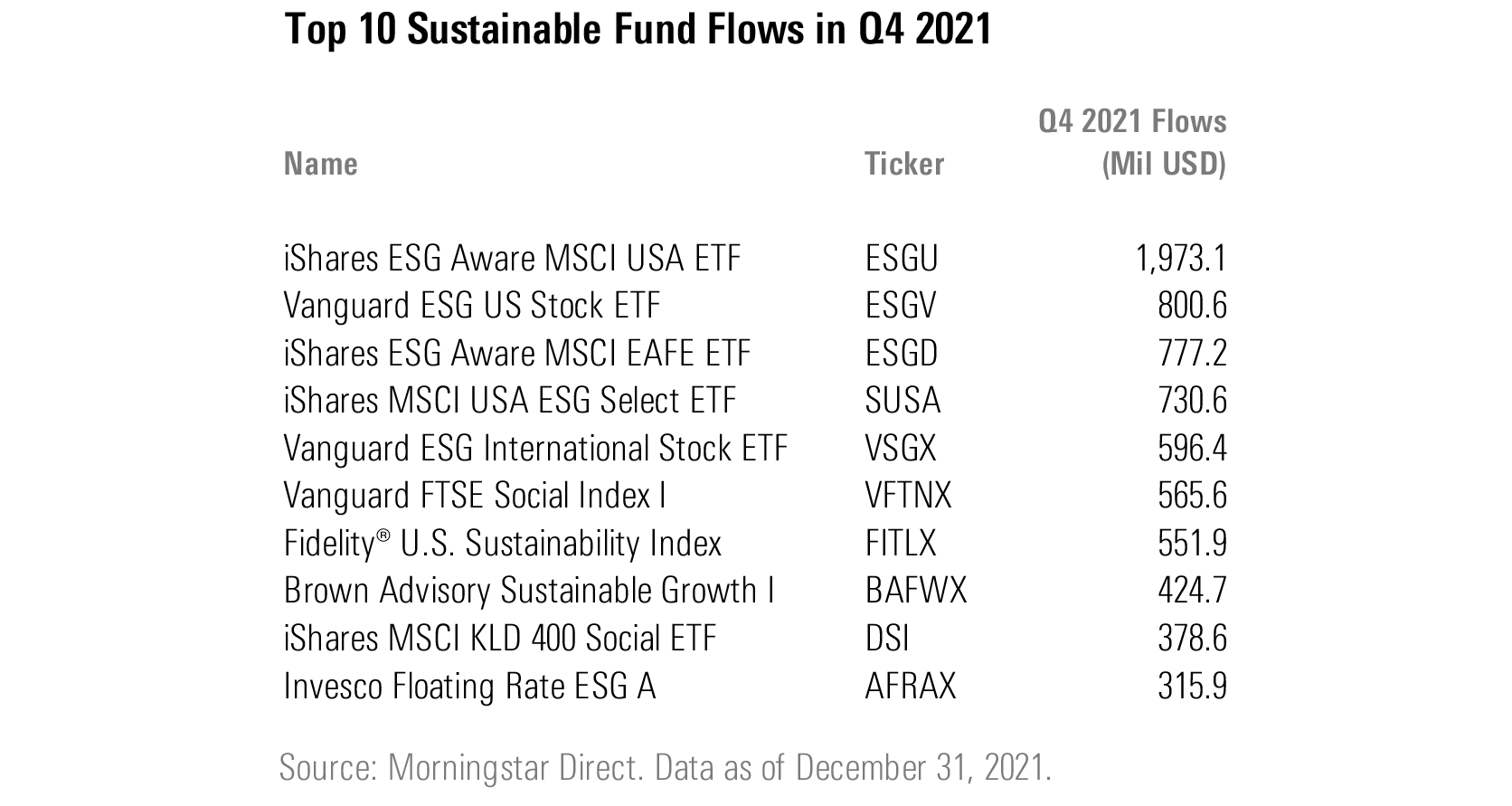

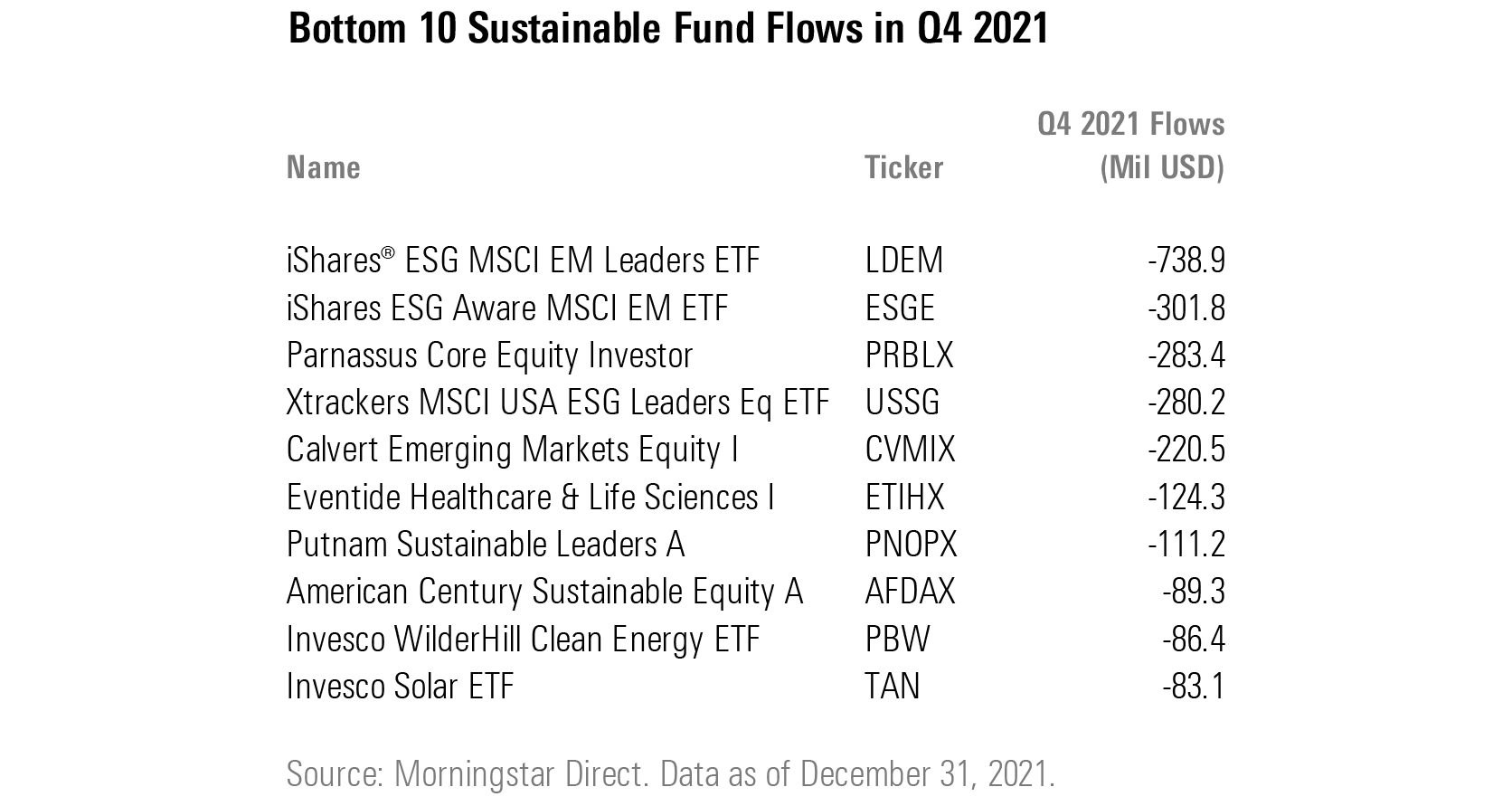

Sustainable Fund Flows Leaders and Laggards

Invesco Floating Rate ESG was the only nonequity fund to make the fourth-quarter leaderboard. Of the top 10 flow-getters (shown below), it is also the most recent fund to adopt a sustainable mandate, having transitioned its strategy in the third quarter of 2020.

Still, eight of the 10 funds attracting the most flows in the fourth quarter of 2021 were passive funds, and six were ETFs. Seven of those were also in the top 10 in the previous quarter: iShares ESG Aware MSCI USA ETF ESGU, Vanguard ESG US Stock ETF ESGV, iShares ESG Aware MSCI EAFE ETF ESGD, iShares MSCI USA ESG Select ETF SUSA, Vanguard ESG International Stock ETF VSGX, Vanguard FTSE Social Index VFTNX, and Brown Advisory Sustainable Growth BAFWX. Notably, iShares ESG Aware MSCI USA ETF topped the list for the third consecutive quarter.

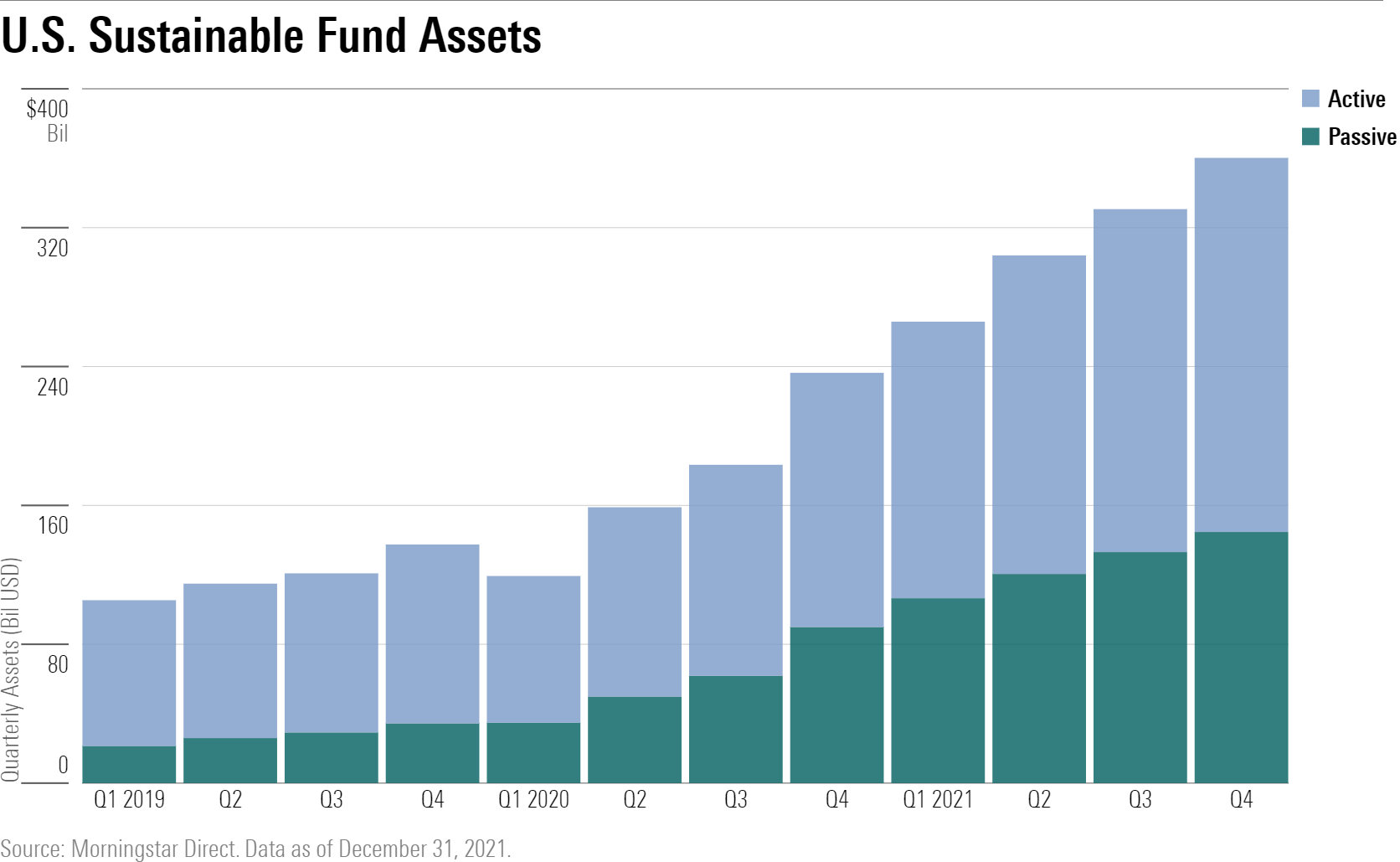

Active Funds Hold the Majority of Sustainable Assets--But Are Shrinking

Assets in U.S. sustainable funds crossed a new high-water mark in the fourth quarter of 2021. As of December 2021, assets totaled $357 billion, as shown below. That’s an 8% increase over the previous quarter and more than 4 times the total three years ago. Active funds retain the majority (roughly 60%) of assets, but their market share is shrinking. Three years ago, active funds held 80% of all U.S. sustainable assets.

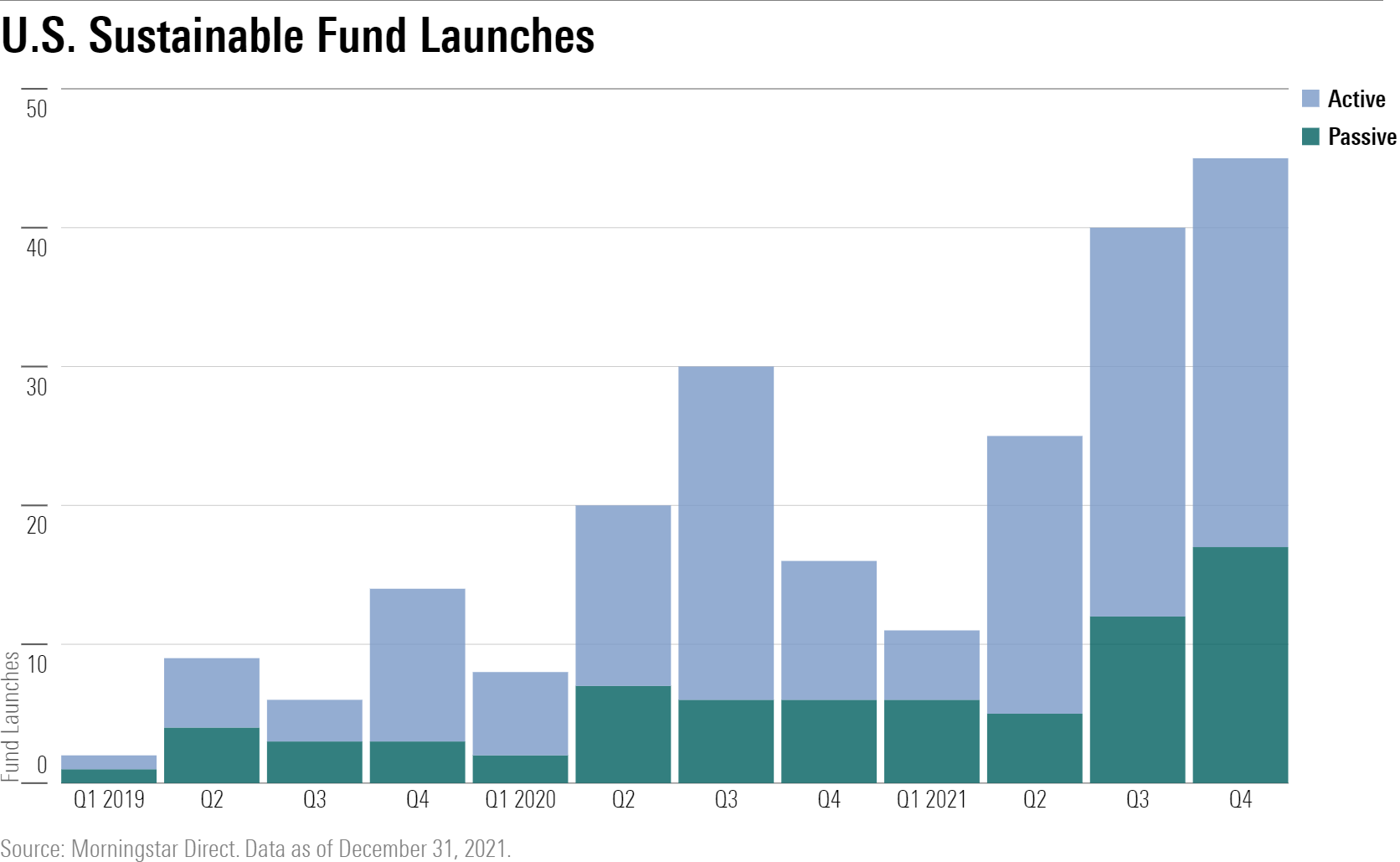

Sustainable Launches Reach New Heights

As U.S. flows into sustainable funds have gained traction, asset managers have responded by expanding their sustainable fund lineups. The chart below shows that in the fourth quarter of 2021, 45 funds were launched in the United States with sustainable mandates. This is the highest number of sustainable funds launched in one quarter, handily beating the previous record of 38 funds set the previous quarter. Of those 45, 35 were equity funds, and 26 were ETFs.

Once again, most of the new sustainable funds available in the U.S. are actively managed offerings. Eleven of the new funds focus on climate action, such as J.P. Morgan Climate Change Solutions ETF TEMP, which targets environmental sustainability themes including renewable energy and electrification, sustainable construction, and less carbon-intense forms of agriculture. One of the new offerings focuses on plant-based innovation companies--VegTech Plant-based Innovation & Climate ETF EATV--but it isn’t the first of its kind. US Vegan Climate ETF VEGN launched in the third quarter of 2019.

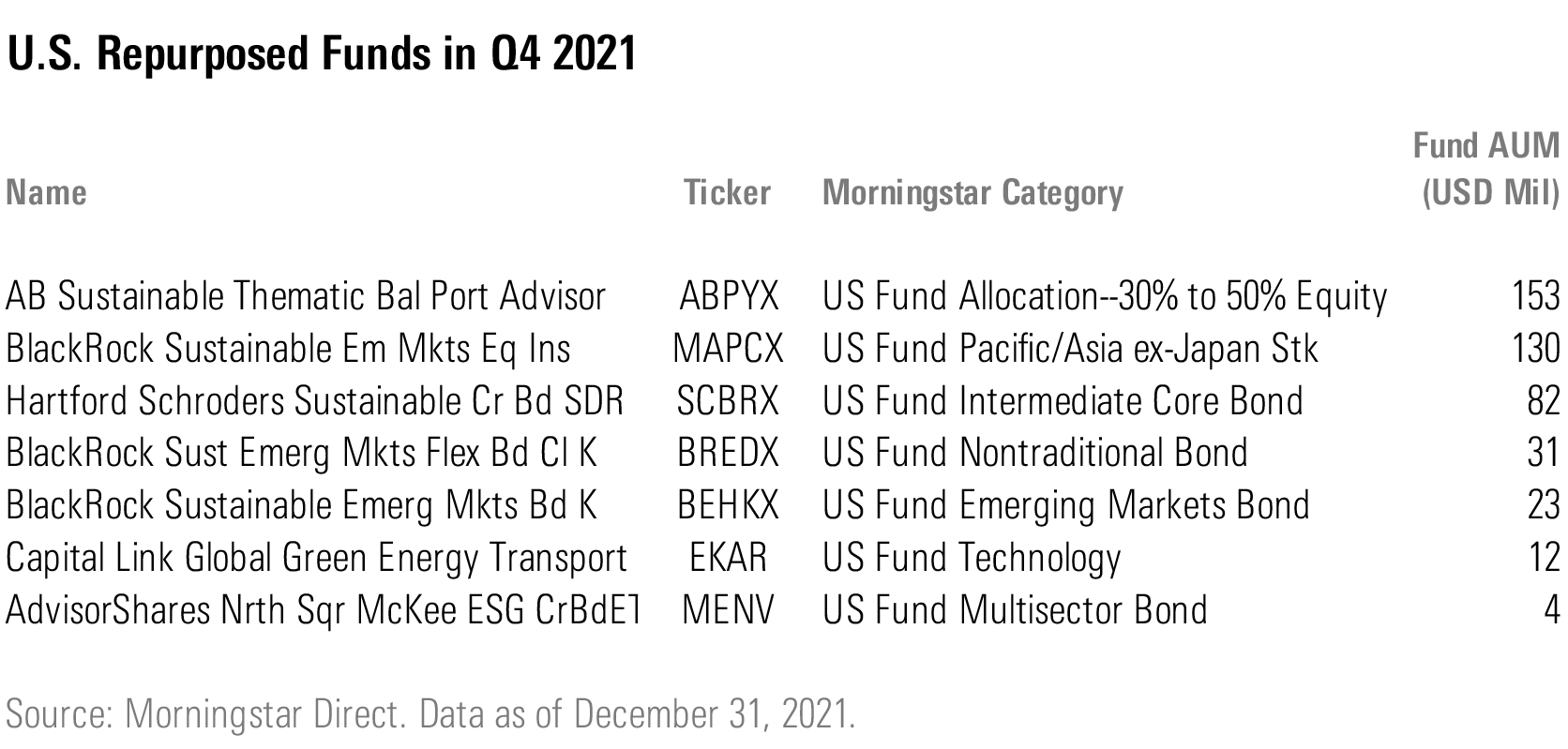

This Quarter Saw Seven Repurposed Funds

Most of the new options available to investors were launched with sustainable mandates, but firms also occasionally change the investment strategies of existing funds to target sustainable outcomes.

In the fourth quarter of 2021, two equity, four fixed-income funds, and one allocation fund were repurposed to adopt sustainable mandates. The largest fund repurposed to incorporate sustainability was AB Sustainable Thematic Balanced Portfolio ABPYX, with $153 million in assets. The fund seeks to invest in companies that the firm believes are aligned with the United Nations Sustainable Development Goals, especially those focused on the themes of health and climate.

The new offerings and the repurposed funds brought the total number of sustainable open-end and exchange-traded funds in the U.S. to 534 at the end of the quarter.

Regulators Move to Reverse Trump-Era Guidance on Sustainability

- ESG Options for Retirement Savers. The U.S. Department of Labor proposed a new rule in October that should make it easier for employers to offer sustainable funds in their workplace retirement plans. This proposal would lift rules that made it difficult and risky for employers that wanted to use ESG-focused investment options as default investments for workers automatically enrolling in a qualified plan. If the rule is finalized, as expected in 2022, it may nudge employers to integrate ESG considerations in making investment selections, which would give retirement plan participants more opportunity to select funds with ESG mandates. In turn, this could spur more investment managers to consider ESG risks as part of the effort to maximize long-term risk-adjusted returns.

- No Shirking Shareholder Rights. This same DOL proposal includes adjustments to Trump-era guidance on the fiduciary duty to vote proxies and exercise other shareholder rights. Among other things, the proposed rule would remove statements such as "the fiduciary duty to manage shareholder rights appurtenant to shares of stock does not require the voting of every proxy or the exercise of every shareholder right" from the Department of Labor's regulation. By doing so, the Biden-era DOL would encourage plans to exercise their rights as shareholders, which may increase participation in proxy-voting activities on behalf of investors. The public comment period for these proposals closed in mid-December, and we expect the guidance to be finalized in early 2022.

- The SEC Joins the Battle Against Greenwashing. In early 2022, we will also keep an eye on the SEC's efforts to mandate disclosures related to climate risk and human-capital management. In September, the SEC's Division of Corporation Finance shared a sample letter outlining comments related to climate change disclosure, which the division may issue to a public company after reviewing its SEC filings. Comments indicate that the SEC may request explanations of any discrepancies between a company's SEC filings and that company's Corporate Social Responsibility report or Net Zero Asset Managers commitment, among other things. Over time, this may lead public companies to expand the scope of their SEC filings, a win for ESG investors who rely on public disclosures.

- Social Policy Significance Supersedes Corporate Specificity. The SEC's Division of Corporate Finance issued a staff legal bulletin in early November that reverses Trump-era guidance that limits the types of issues shareholders can address via corporate proxy ballots. The previous guidance raised the chances that shareholder-filed ballot measures would be excludable under the long-standing "ordinary business rule," which allows companies to omit resolutions that may impact their day-to-day business management and operations, unless the issue has a broader social policy relevance. The Trump-era interpretation narrowed the scope of shareholder resolutions that are deemed to have social policy relevance by advising that the proposal also needed to be demonstrably relevant to the specific company. This led to the omission of several shareholder resolutions requesting climate change disclosures from energy companies. The new stance states that "staff will no longer focus on determining the nexus between a policy issue and the company, but will instead focus on the social policy significance of the issue that is the subject of the shareholder proposal. In making this determination, the staff will consider whether the proposal raises issues with a broad societal impact, such that they transcend the ordinary business of the company." This opens the door for resolutions on climate change and social justice issues to make it to a vote in coming proxy seasons, which we see as a win for the end investor.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZKOY2ZAHLJVJJMCLXHIVFME56M.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IGTBIPRO7NEEVJCDNBPNUYEKEY.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HDPMMDGUA5CUHI254MRUHYEFWU.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/987376c2-20a0-406b-b3ec-df530324b39c.jpg)