Sustainability Matters: Sustainable Equity Funds Turn In Another Strong Quarter

Of ESG index funds, 25 of 26 have outperformed for the year to date.

/s3.amazonaws.com/arc-authors/morningstar/42c1ea94-d6c0-4bf1-a767-7f56026627df.jpg)

Sustainable equity funds maintained their strong 2020 performance in the third quarter. Stocks continued to rebound during the first two months of the quarter before falling in September amid concerns over increasing coronavirus cases and uncertainty ahead of the U.S. election. Despite a 3.6% decline in September, the Morningstar US Market Index gained 9.2% for the quarter. Stocks outside the United States didn’t fare as well. The Morningstar Developed ex-US Market Index gained 5.8% for the quarter.

As was the case in the first two quarters of 2020, a large majority of sustainable equity funds finished in the top halves of their Morningstar Categories for the third quarter. Sixteen of 26 ESG-focused index funds outperformed conventional index funds that cover the same parts of the market.

For the year to date, 73% of sustainable equity funds rank in the top halves of their Morningstar Categories and 25 of 26 ESG-focused index funds have outperformed their conventional index-fund counterparts.

Sustainable Funds Bettered Their Conventional Peers in Third Quarter In assessing performance, it's important to keep in mind that sustainable stock funds come in all shapes and sizes. They may have a U.S. large-cap focus or they may invest in smaller-cap stocks. They may invest in non-U.S. stocks in developed markets or emerging markets. They may employ growth or value styles; they may be actively managed or passively track an index. Grouping sustainable funds with traditional funds that invest in the same parts of the market allows for apples-to-apples comparisons. We do this by assigning sustainable funds to Morningstar Categories based on the area of the market on which they are focused, just as we do for traditional funds.

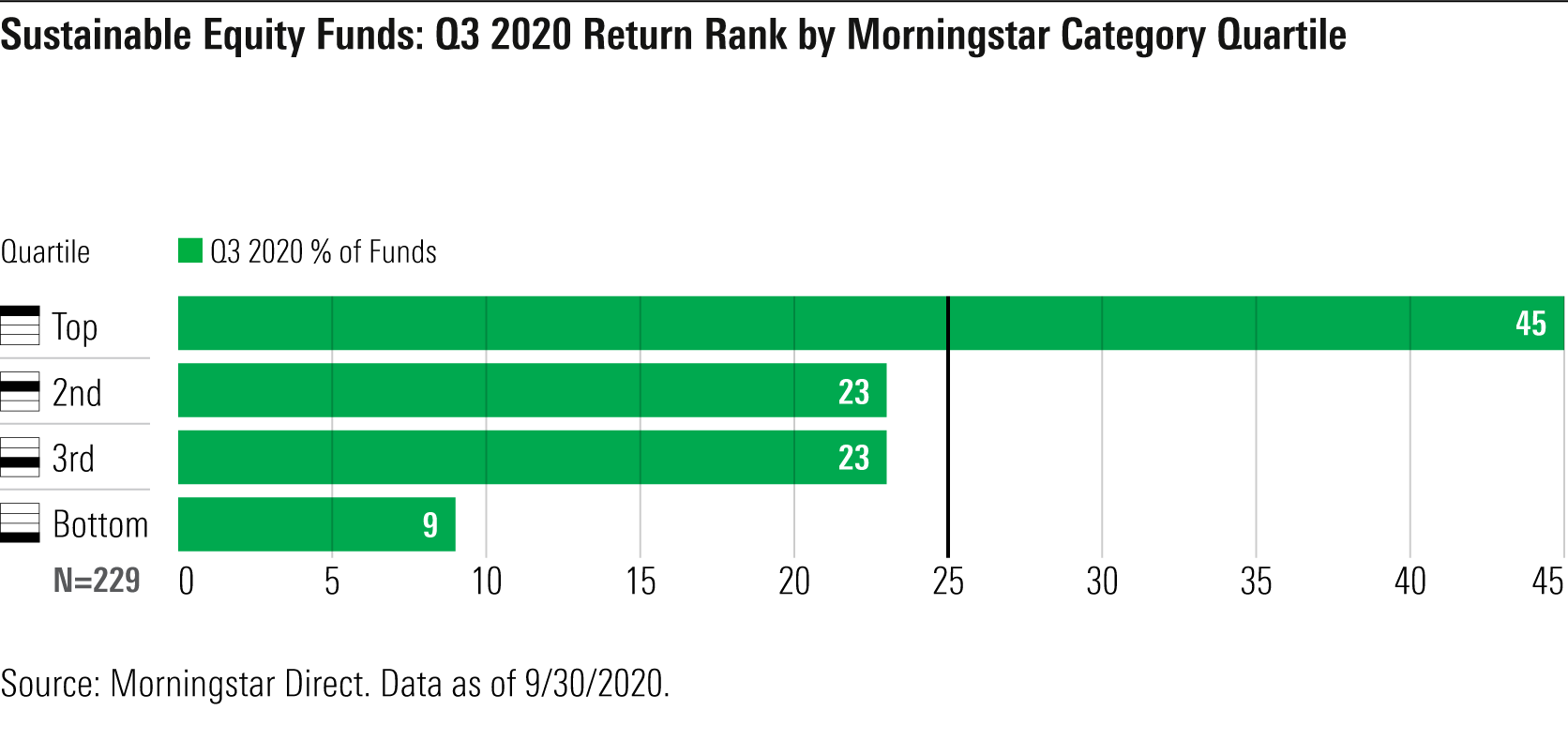

For the third quarter, the returns of sustainable equity funds placed them, as a group, in the upper ranks of their categories. Fully two thirds ranked in the top halves of their categories, and an impressive 45% had top-quartile rankings. In other words, while, by definition, 25% of the category ranks in the top quartile, 45% of the subgroup of sustainable funds did so. By contrast, only 9% of sustainable funds had bottom-quartile rankings. Sustainable funds were 5 times more likely to rank in the top quartile than in the bottom quartile in the third quarter.

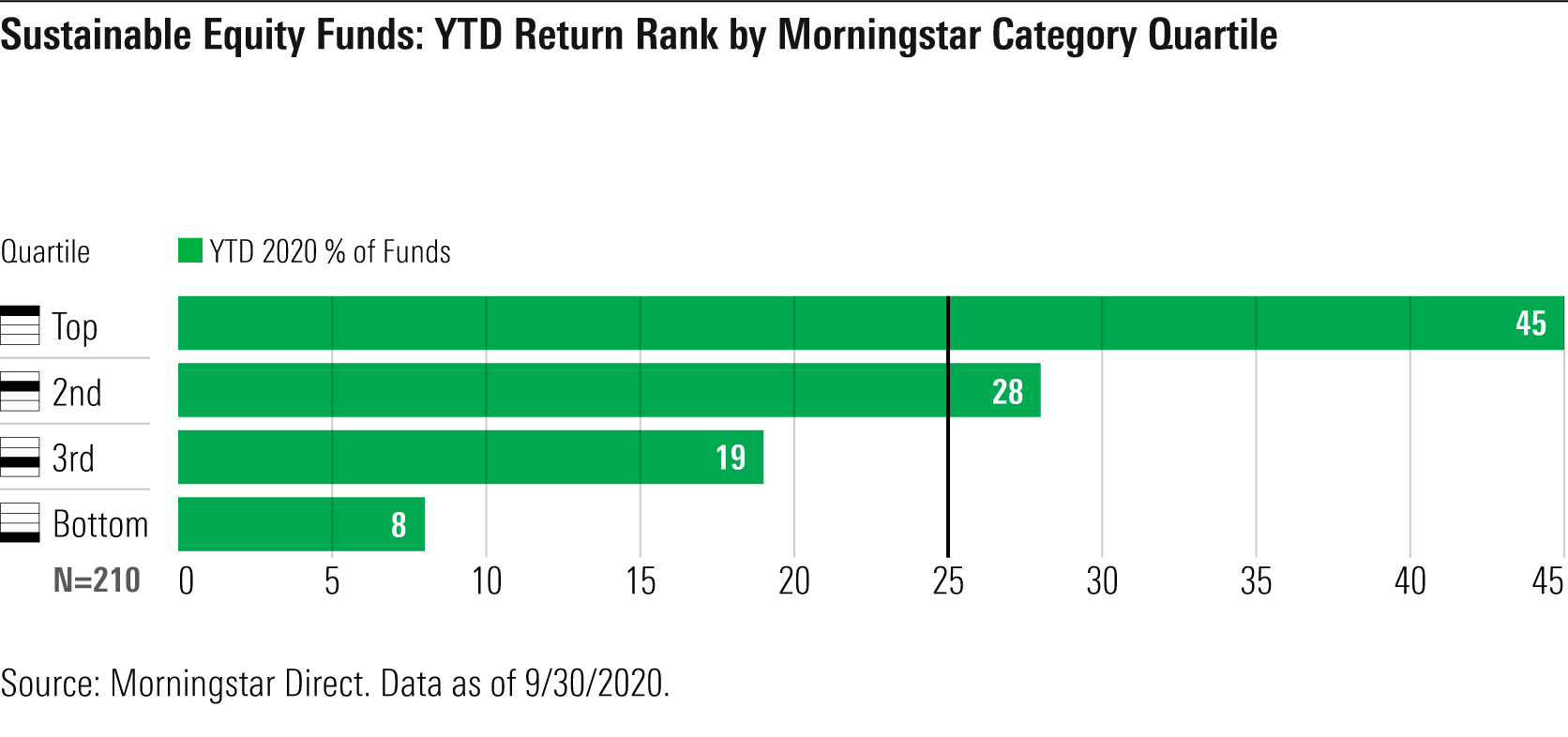

For the year to date, the comparisons are even more favorable for sustainable equity funds. Nearly three fourths, 73%, rank in the top halves of their categories. And the ratio of top-to-bottom quartile ranks is 45% to 8%.

Sustainable Index Funds Maintain Their Outperformance of Conventional Index Funds Investors in sustainable funds have increasingly shown their preference for index funds. Assets in passive sustainable funds have grown rapidly in recent years, and so far this year, passive sustainable funds have attracted more than twice the flows of actively managed sustainable funds. For that reason alone, it's relevant to take a closer look at sustainable index fund performance.

Beyond that, index funds can provide useful insights into why performance differs between sustainable and conventional strategies. While sustainable index funds are not all structured the same way or track the same indexes, they provide the same kind of broad, diversified exposure as conventional market-cap-weighted index funds do. The difference is that the sustainable index funds use company ESG ratings and screens to determine which stocks make it into the index and their weightings.

At the beginning of the year, I selected 26 sustainable index funds that provide close comparisons to conventional index funds that invest in the U.S., developed markets outside the U.S., and emerging markets. In the first quarter, 24 of the 26 outperformed a comparable conventional index fund, net of fees. In the second quarter, 18 did so.

In the third quarter, 16 of the 26 sustainable index funds outperformed a comparable conventional index fund, net of fees. For the year to date, 25 of the 26 sustainable index funds have outperformed.

U.S Large Cap. Among U.S stock index funds, seven of the 12 sustainable funds outperformed iShares Core S&P 500 ETF IVV for the quarter, net of fees. While iShares Core S&P 500 ETF posted an 8.9% return, the sustainable funds' average return was 9.4%, with five funds posting returns above 10%.

The top-performing U.S. sustainable index fund was IQ Candriam ESG U.S. Equity ETF IQSU, which posted a 10.9% return. Based on a proprietary index developed by IndexIQ for European asset manager Candriam, a subsidiary of New York Life, IQ Candriam ESG U.S. Equity ET is also the top performer for the year to date, with a 14.9% return. Calvert US Large Cap Core Responsible Index CISIX, based on a proprietary index, and Vanguard FTSE Social Index VFTNX, based on the FTSE4Good US Select Index, finished second and third, respectively, for the quarter among U.S. sustainable index funds.

For the year to date, all 12 U.S. sustainable funds are ahead of the S&P 500 index-tracking iShares Core S&P 500 ETF.

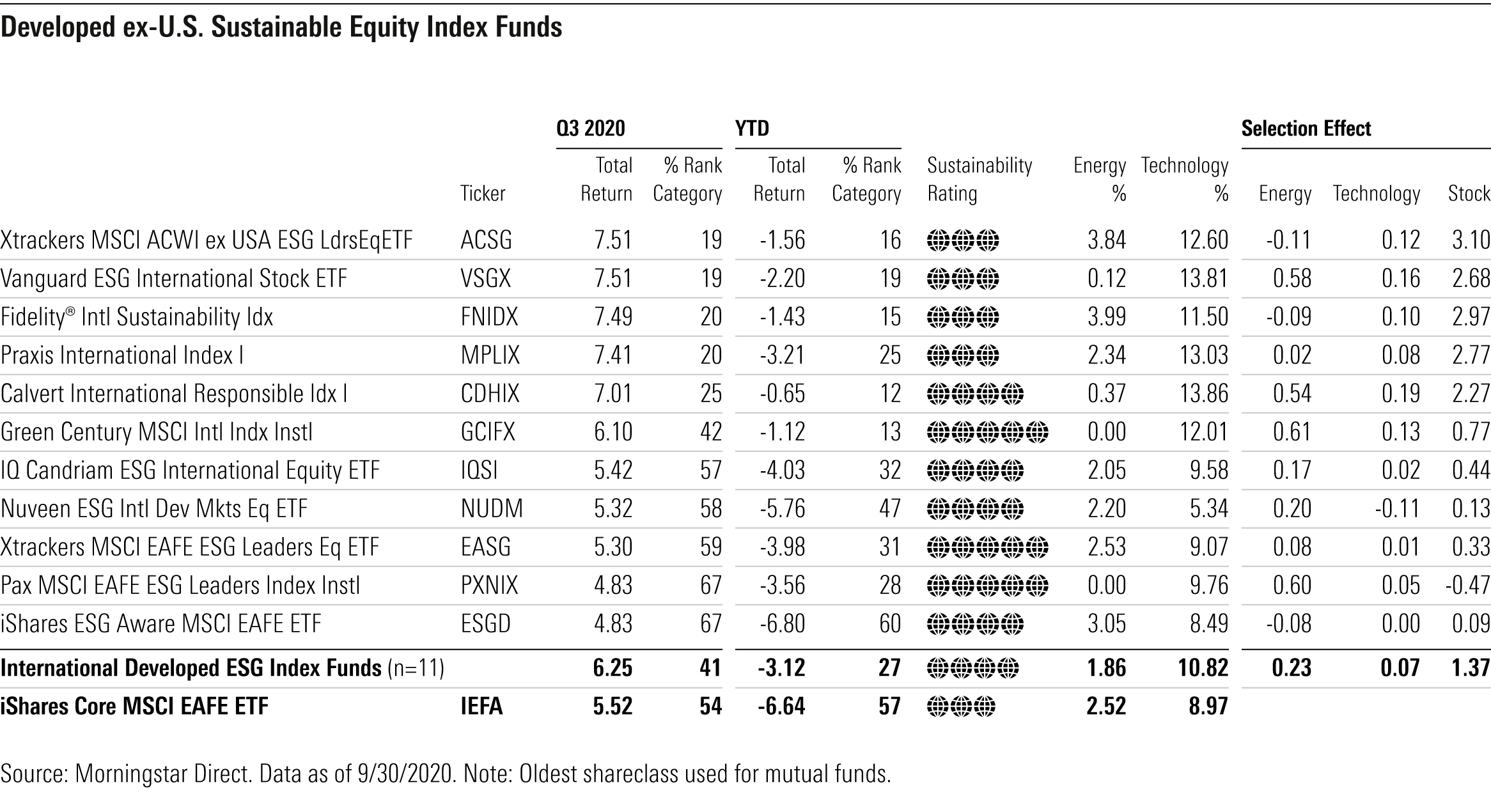

Developed Markets-ex U.S. Among developed markets-ex U.S. index funds, six sustainable index funds outperformed iShares Core MSCI EAFE ETF IEFA for the quarter and five lagged it. On average, though, the outperformers beat iShares Core MSCI EAFE ETF by 1.7%, while the underperformers lagged it by only 0.4%.

The top-performing funds in this group were Xtrackers MSCI ACWI ex USA ESG Leaders Equity ETF ACSG, Vanguard ESG International Stock ETF VSGX, and Fidelity International Sustainability Index FNIDX. All posted returns of 7.5%. The Xtrackers and Fidelity funds track nearly identical MSCI ESG indexes, while the Vanguard fund tracks the FTSE Global All Cap ex US Choice Index.

For the year to date, 10 of 11 non-U.S. developed-markets funds are ahead of the MSCI EAFE Index-tracking iShares Core MSCI EAFE ETF. The one laggard in the group is iShares ESG Aware MSCI EAFE ETF ESGD. It is based on the MSCI EAFE Extended ESG Focus Index, which tilts toward firms with better ESG practices but keeps tracking error low relative to the MSCI EAFE Index.

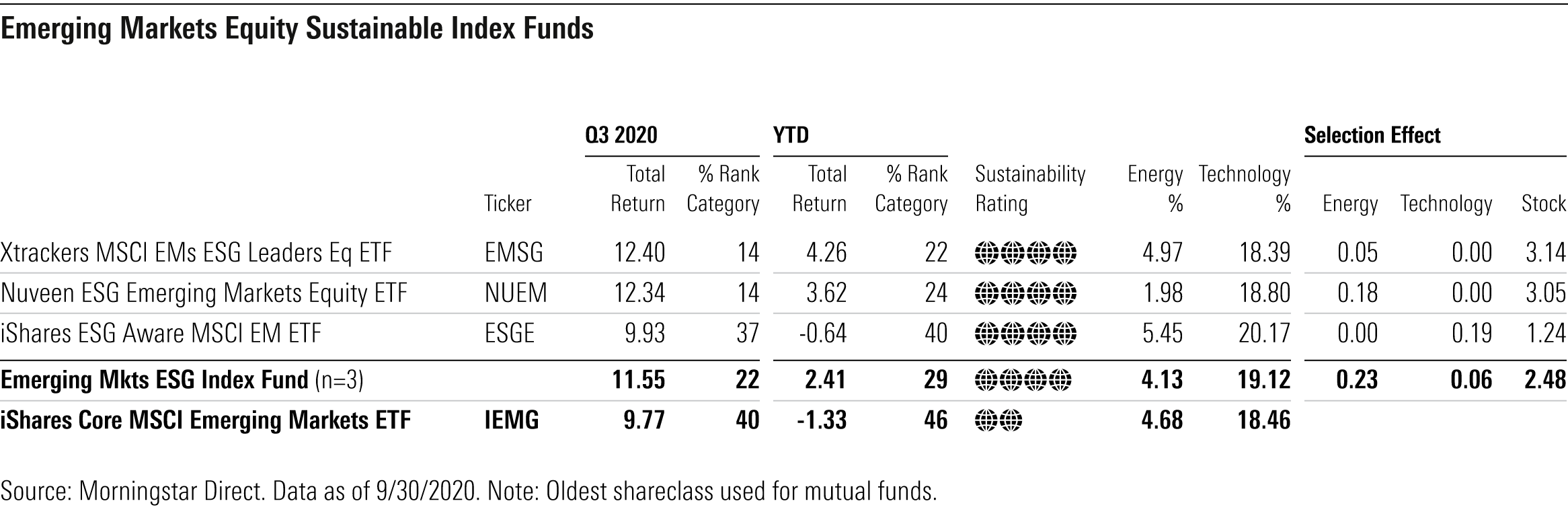

Emerging Markets. All three sustainable emerging-markets index funds outperformed iShares Core MSCI Emerging Markets ETF IEMG for the quarter and have also done so for the year to date. Topping the group is Xtrackers MSCI EMs ESG Leaders Equity ETF EMSG, which gained 12.4% for the third quarter and 4.3% for the year to date. It is based on the MSCI Emerging Markets ESG Leaders Index. Nuveen ESG Emerging Markets Equity NUEM has similar returns and is based on the proprietary TIAA ESG Emerging Markets Equity Index. Still ahead of iShares Core MSCI Emerging Markets ETF, but tracking closer to it, is iShares ESG Aware MSCI Emerging Markets ETF ESGE. Similar to its sibling iShares ESG Aware MSCI EAFE ETF, which was discussed in the prior section, this fund is designed with minimal tracking error to the conventional index. It follows the MSCI Emerging Markets Extended ESG Focus Index.

Energy Underweights and ESG Stock Selection Helped Performance The energy sector has had a terrible year overall, and it was by far the worst-performing sector in the third quarter. That generally helped sustainable funds because they typically have lower carbon-based energy exposure or none at all (although only six of the 26 funds have energy exposure of 0.12% or less). On average, attribution analysis shows that energy sector weightings had a positive effect of 0.35% for U.S. sustainable index funds and 0.23% for those that invest outside the U.S. However, for U.S. outperformers (remember, seven of 12 outperformed iShares Core S&P 500 ETF, the S&P index tracker), energy underweights had a positive impact of 0.47%, while for underperformers, it was only 0.17%.

Although sustainable funds are typically overweight technology, the attribution effects of technology overweights were only modestly positive in the third quarter. Of course, stocks like Apple AAPL, Amazon.com AMZN, and Alphabet GOOGL, which many think of as tech stocks, now reside in other sectors, and sustainable index funds typically have overweight positions in these names. For the quarter, overweights to Apple and Amazon were positive, as both stocks outperformed the market. (Facebook FB is a much different story, as only six of the 12 U.S. sustainable index funds own it, and only one has an overweight position relative to the S&P 500.)

Among the 26 sustainable index funds, all but four have Morningstar Sustainability Ratings of 4 or 5 globes, and three of the four with 3-globe ratings barely fall short of receiving 4 globes. Higher globe ratings are an indicator of sustainable index funds’ tilt toward companies with better ESG profiles and lower ESG risk. Looking at the stock-selection effects for these funds provides some evidence on whether a focus on ESG characteristics was helpful or harmful.

Throughout the year, stock selection has been positive for sustainable index funds. For U.S. funds in the third quarter, stock selection was just modestly positive, averaging 0.12%. But for the outperforming U.S. funds, stock selection effects averaged 0.75%, while for underperforming funds, stock selection averaged negative 0.76%. Stock selection effects were much stronger for funds investing outside the United States. Developed markets ex-U.S. funds averaged a positive 1.37% stock selection effect while emerging-markets funds averaged 2.48%. In sum, based on attribution analysis, sustainable index funds were helped in the third quarter by energy underweights and ESG stock selection.

ESG Insights Lead to Long-Term Stakeholder-Centric Focus The better relative performance of sustainable funds in the first three quarters of this year is tied to their focus on companies with stronger ESG profiles and lower levels of material ESG risk. As I concluded in last quarter's review, good performance helps make the case that investing with an eye toward how a company addresses ESG risks and, more broadly, how it manages all its stakeholders, can produce better returns than those of conventional funds, especially during periods of market and economic turmoil.

Of course, that doesn’t mean sustainable funds are always going to outperform. Although carbon-based energy is in long-term secular decline, energy stocks could and likely will rebound at some point. Likewise, Apple, Amazon, and Alphabet won’t always lead the market, and the latter two companies face growing ESG-related risks.

ESG insights can help analysts and portfolio managers develop a more holistic view of a company. They no longer have to rely on financial indicators alone. ESG insights can help us understand how sustainable a firm’s long-term business model is and how well it treats its stakeholders, and it can provide an early warning on environmental and social risks before they affect company value.

For companies, recognizing that more of their investor base consists of sustainable investors will hasten the move away from a short-term decision-making approach focused mainly on shareholders to a longer-term perspective that focuses on creating value for all stakeholders, with better outcomes for society and the planet.

We’ve seen this year that companies that already have this perspective are performing better amid the coronavirus epidemic for all their stakeholders. As we’ve seen, sustainable investing is perfectly capable of holding its own on the performance front while also having a broader impact.

Jon Hale (jon.hale@morningstar.com) has been researching the fund industry since 1995. He is Morningstar’s director of ESG research for the Americas and a member of Morningstar's investment research department. While Morningstar typically agrees with the views Jon expresses on ESG matters, they represent his own views.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/FGC25JIKZ5EATCXF265D56SZTE.jpg)

/d10o6nnig0wrdw.cloudfront.net/04-25-2024/t_d30270f760794625a1e74b94c0d352af_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/DOXM5RLEKJHX5B6OIEWSUMX6X4.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/42c1ea94-d6c0-4bf1-a767-7f56026627df.jpg)