Private Equity and Target-Date Funds: An Unrequited Love Story

Private equity managers long for target-date funds, but the asset class’ high fees and operational challenges keep it in the friend zone.

/s3.amazonaws.com/arc-authors/morningstar/af89071a-fa91-434d-a760-d1277f0432b6.jpg)

According to the 2021 Investment Company Factbook, private equity managers haven’t yet managed to crack the $7 trillion U.S. 401(k) defined-contribution market. The U.S. Labor Department created an opening in 2020, though, when it said defined-contribution plans could offer private equity if it’s within a professionally managed multi-asset-class fund, like a target-date strategy.

This has spurred speculation of private equity's imminent arrival in target-date funds. As part of a broader review of target-date funds, the U.S. Government Accountability Office in looking at how much target-date funds use private equity. Spoiler alert: It's almost nonexistent.

None of the 10 largest target-date providers, which make up approximately 90% of the $2.8 trillion target-date market, use private equity in their mutual funds or collective investment trusts. Some, like T. Rowe Price Retirement, may hold some private companies through underlying active equity funds, but those exposures are typically less than 0.25%.

Conversations with the largest target-date providers indicate that private equity isn't coming to target-date funds anytime soon.

Private Equity Love Does Cost a Thing

The first hurdle to adding private equity to target-dates are fees. Plan sponsors are notoriously cost-conscious and private equity fees are notoriously high.

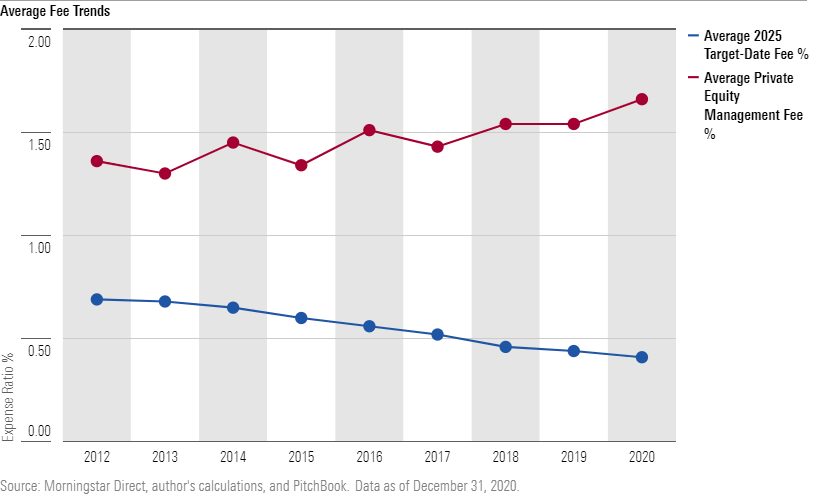

The chart below shows the average prospectus adjusted expense ratio trend for the cheapest share class of 2025 target-date funds and the average private equity fund management fee, according to PitchBook. Like private equity management fees, the cheapest share classes of target-date funds exclude intermediary fees.

At the end of 2020, the average 2025 target-date fund fee was 0.44%, down from 0.69% in 2012. Private equity fees have trended in the opposite direction. At the end of 2020, the average management fee was 1.66%, up from 1.36% in 2012. That doesn't include performance fees, which are typically around 20%. Current regulations also prohibit charging a performance fee that’s not asymmetrical in a mutual fund, so it's possible the private equity management fees within a target-date fund could be higher than the current average to make up for those lost fees.

Target-date fees are important to plan sponsors and investors. In 2020, the cheapest decile of target-date fund share classes--those costing less than 0.26%--claimed nearly 70% of net inflows.

If a target-date manager were to allocate 10% to private equity throughout the glide path, it would add about 0.16% to the overall expense ratio. That may not sound like a lot, but for the cheapest series like Schwab Target Index and Fidelity Freedom Index (both 0.08%) or Vanguard Target Retirement (0.09%), that would triple the cost.

Lower-cost investment strategies not only tend to outperform more expensive ones, but they also reduce the threat of excessive-fee lawsuits. The number of lawsuits filed against 401(k) plans jumped from 19 in 2019 to almost 100 in 2020, according to mutual fund industry news source Ignites.

Fee competition and legal threats should cool plan sponsors' ardor for strategies that may increase their series' fees, even if there's a sound investment rationale.

Operations: It's Complicated

Fees aren't the only roadblock. Unlike stocks and bonds, private equity is not readily available to managers. Funds must ramp up in size as managers seek and create new equity positions. Investors pledge dollar amounts to private equity funds that they gradually invest over their lives as they find opportunities. It often takes years for a private equity fund to be fully invested, but it charges management fees on the committed capital the whole time.

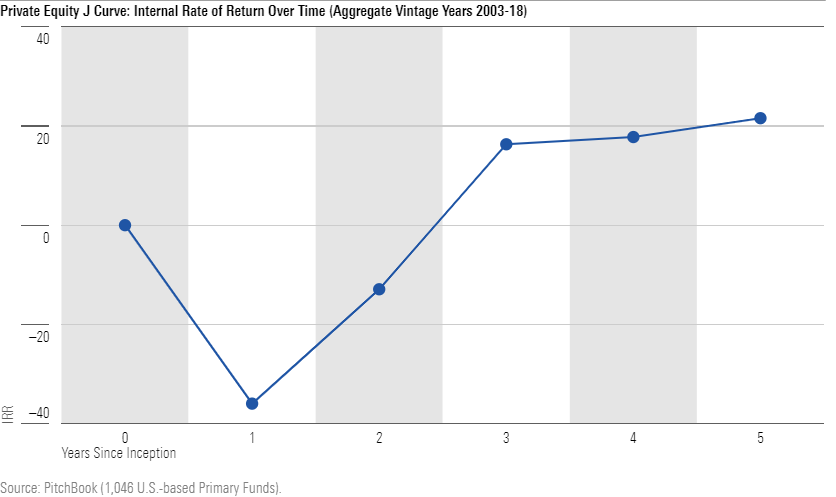

Paying high fees while management searches for investments leads to a performance pattern known as the "J curve" because private equity funds' performance dips in the first couple of years as they deploy cash before climbing again, as shown in this chart of the pooled internal rate of return for all U.S.-based private equity funds launched between 2003 and 2018.

The internal rate of return was almost negative 40% for the first year and still down about negative 10% after the second year, according to PitchBook. It wasn't until the third year that the internal rate of return turned positive. Investors who leave the fund at the bottom of this curve pay for nothing.

You could use a fund of funds that is already producing returns, but that adds another layer of management fees and raises the cost hurdle.

Valuation is another drawback. Privately held companies typically are valued quarterly. Target-date funds strike their net asset values daily. Some managers use baskets of publicly traded stocks resembling their private holdings to approximate valuations, but these are, at best, guesses. They need a better solution.

Will They or Won't They?

Private equity's historical returns are eye-catching. That's why target-date funds are at least flirting with them.

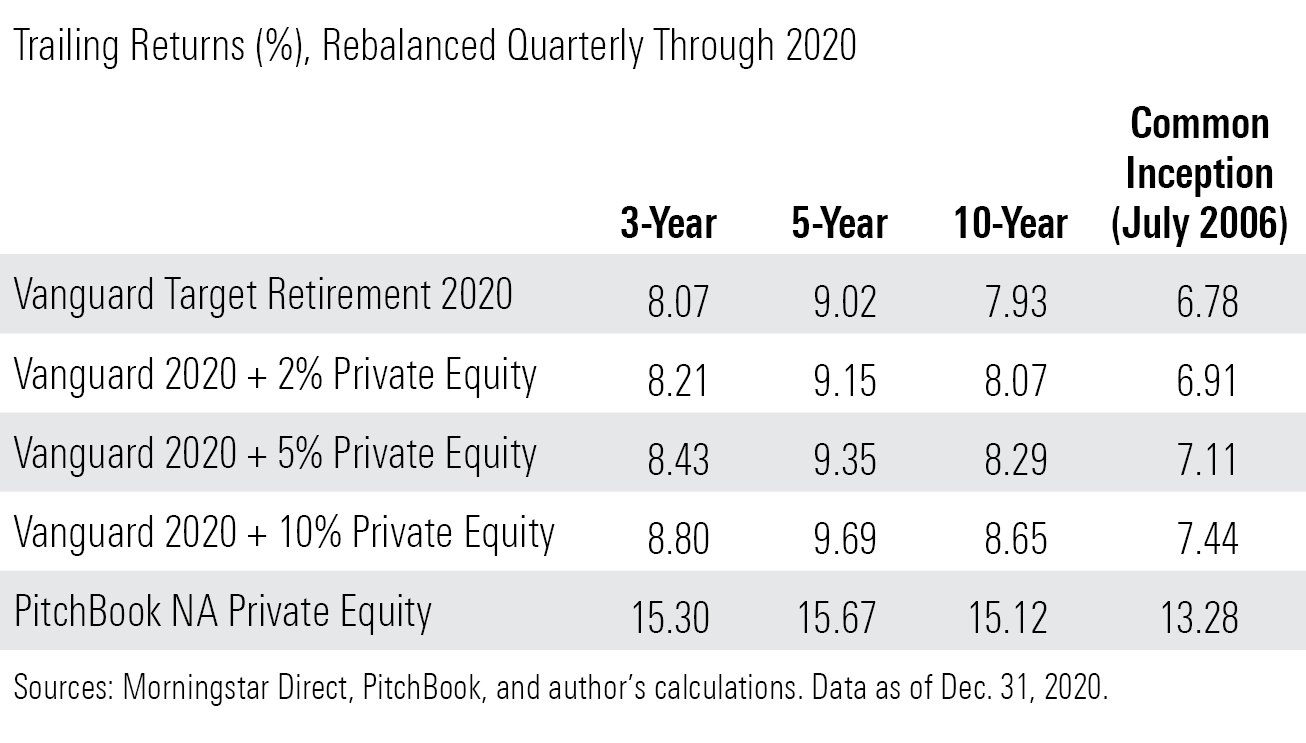

To see how private equity could impact a target-date fund's long-term returns we ran a couple simple simulations using Vanguard Target Retirement 2020 and PitchBook's quarterly private equity returns. There was no way for anyone to capture these average private equity results, and past performance isn't indicative of future results, so this is a hypothetical exercise.

This table shows the trailing returns for the target-date fund, private equity, and different combinations of both, rebalanced quarterly through 2020, the most recent data available for private equity returns.

From Vanguard Target Retirement 2020's inception in July 2006 through 2020, private equity boosted returns with as little as a 2% allocation. Given the limits on investing in illiquid assets (funds can own up to 15% in illiquid securities under the 1940 Act), we think 10% is the most likely cap on private equity allocations in target-date funds.

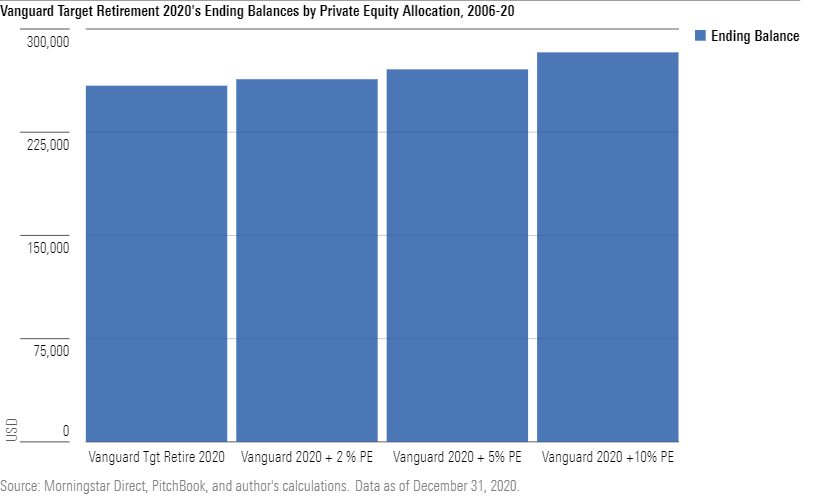

A 5% allocation is probably big enough to make a decent impact on returns, but not big enough to flirt with the 15% illiquid threshold. A 5% allocation would have added about an additional $11,800 to an account that started with a $100,000 balance if held for the full period, as shown below.

The Course of True Love Never Did Run Smooth

It’s likely that private equity’s high fees and real-world implementation challenges will continue to outweigh the asset class’ enticing return potential. Some smaller target-date providers may use private equity to differentiate themselves, but unless it gets cheaper and easier to use, most target-date funds won’t include private equity anytime soon.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

/d10o6nnig0wrdw.cloudfront.net/07-25-2024/t_56eea4e8bb7d4b4fab9986001d5da1b6_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/BU6RVFENPMQF4EOJ6ONIPW5W5Q.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/af89071a-fa91-434d-a760-d1277f0432b6.jpg)