Inside a Tough Year for Primecap

One of my favorite Vanguard fund managers fell well behind in 2020.

/s3.amazonaws.com/arc-authors/morningstar/fcc1768d-a037-447d-8b7d-b44a20e0fcf2.jpg)

The article was published in the January 2021 issue of Morningstar FundInvestor. Download a complimentary copy of FundInvestor by visiting the website.

Primecap has beaten its peer group handily for much of the past decade and all the way back to when its first fund launched in 1984. For sure, there have been off years, but not many like 2020, when the fund’s 16% gain massively lagged the 37% gain of the average large-growth fund and 39% for the Russell 1000 Growth Index. It was so bad that the fund’s three-, five-, and 10-year returns are now pedestrian relative to peers as well.

Who Is Primecap? Primecap is a Pasadena, California-based firm founded in the 1980s by growth managers who left Capital Group, the firm behind American funds. Its emphasis on deep fundamental research in an area often given over to Wall Street hype has proved remarkably successful. It has a team of managers who select stocks independently of one another and seasoned analysts who are continually ahead of the curve.

The team runs three funds for Vanguard and three under its own Primecap Odyssey label, all of which have Morningstar Analyst Ratings of Gold. They’ve been so successful that only Primecap Odyssey Stock POSKX and Primecap Odyssey Growth POGRX are open to new investors. The basic growth-oriented strategy is the same across the board with two variations. Primecap Odyssey Stock and Vanguard Primecap Core VPCCX are slightly more valuation-conscious and thus land in large blend. Primecap Odyssey Aggressive Growth POAGX has more small- and mid-cap exposure and thus lands in mid-growth.

Because of closings and different options in different accounts, I own three: Primecap Odyssey Aggressive Growth, Vanguard Primecap Core, and Vanguard Capital Opportunity VHCOX. In other cases, I usually wouldn’t own three in order to avoid overlap; here, it underscores my conviction. Management has conviction, too. The three most experienced managers have more than $1 million each in all six funds.

So, What Went Wrong? In 2020, the fastest-growing companies took an overwhelming share of investor attention. Zoom ZM, Tesla TSLA, Square SQ, and most of the FAANGs (Facebook FB, Amazon.com AMZN, Apple AAPL, Netflix NFLX, and Alphabet GOOG [aka Google]) posted stratospheric gains. Primecap did have some of the big winners. It had modest positions in Tesla and Amazon, plus low-tech winner FedEx FDX, which profited from the massive move to online ordering caused by the coronavirus pandemic. (I'm using Vanguard Primecap for illustration purposes, but the story is similar for the rest of the lineup.)

But overall, they were modestly underweight in technology in a year when tech was the only place to be and massively underweight the big winners like Apple and Amazon, which represent 11% and 8%, respectively, of the Russell 1000 Growth Index. Instead, Primecap was overweight more modestly priced names like Adobe ADBE and Intel INTC. Adobe was a winner, but Intel was in the red in 2020.

A second problem was they owned travel stocks that few of their peers owned in a meaningful way. Needless to say, COVID-19 crushed some of their holdings like Southwest Airlines LUV and United Airlines Holdings UAL.

A third weak spot was big biotech names like Biogen BIIB and Amgen AMGN, which have been big winners in the past but lost money in 2020. If you pick out the best years for Primecap performance, they are often years in which biotech fared well, because Primecap has long been a big investor there.

Has It Changed? This is the central question to ask of a good fund that's had a bad year.

Let’s start with people. Primecap's MO is to find the smartest people at a school, hire them without much regard to background, and then let them work. It is able to do this because the firm is a partnership in which ownership is very lucrative for those successful in the long run. It’s a big part of Primecap’s competitive advantage. Sometimes a slump is accompanied by or preceded by an exodus of talent.

Good news: The people here haven’t changed. The funds are run by five managers and 14 analysts. Over the past five years, no managers have left. Only three analysts have left, while four have been hired. Management has a good spread of experience levels from co-founder Theo Kolokotrones on down. That’s important because you don’t want to face a cliff edge when a couple of people approach retirement age.

On to process. To see what has changed, two things I look at are historical industry weights and style trail.

The story on industry and sector weights is very much a steady picture, where weightings typically change at a measured pace. They can, however, shift substantially during extreme periods. The fund’s preference for technology, healthcare, and industrials stocks has been consistent, but its tech weighting seesawed from the late 1990s to the early 2000s and again more recently. Overall, I see less change than at the typical actively managed fund.

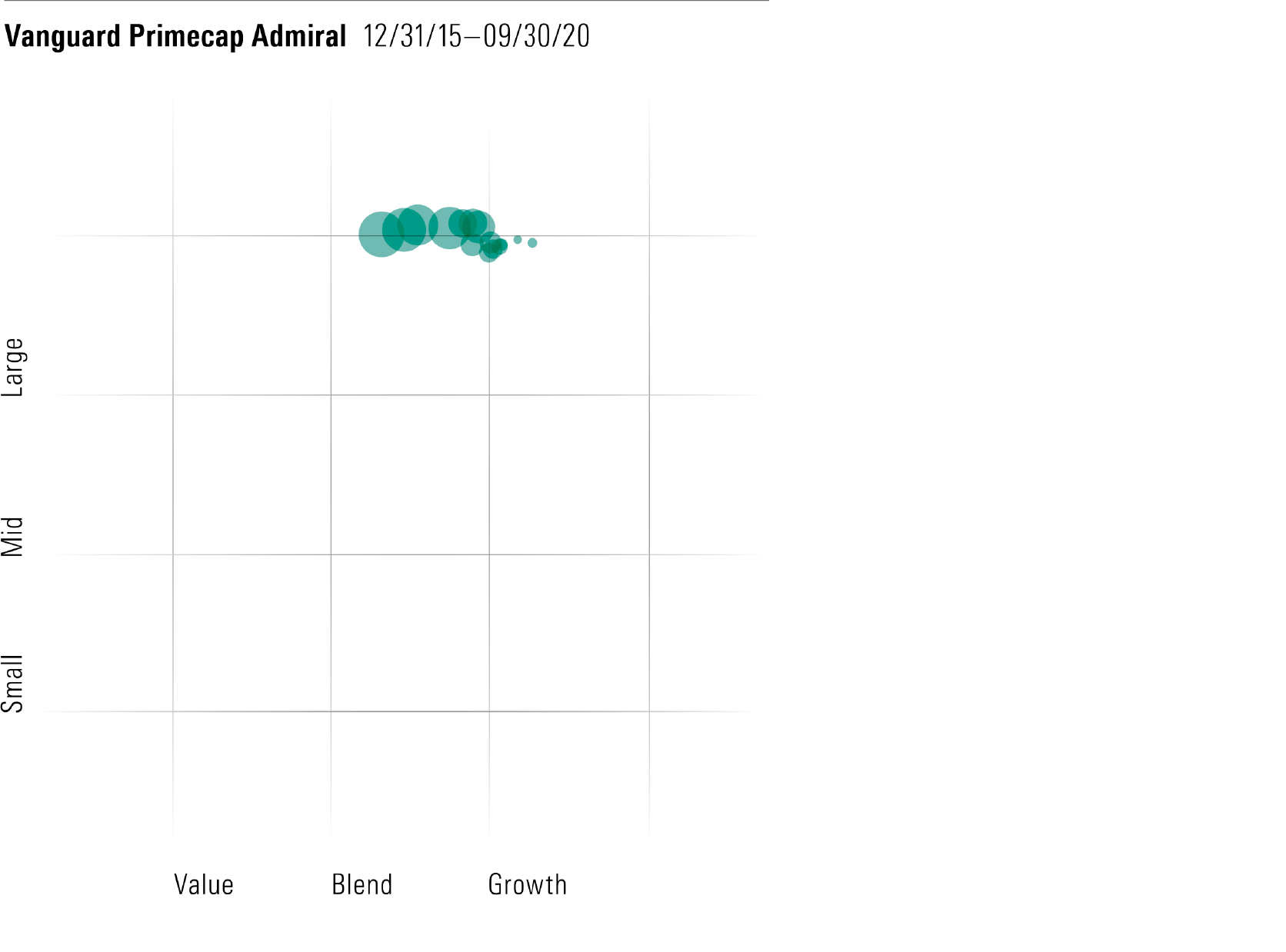

The story on style is a little tricky, though. I’ve graphed the style trail across the Morningstar Style Box over the past five years. The smaller circles are from the beginning of the time period, and the bigger are the most recent. The circles represent the middle of the portfolio, or the centroid.

As you can see, the centroid has moved from the middle of growth to the middle of blend in just five years. But in this case, the fund didn’t change so much as the market around it. FAANG stocks have exploded and dominate the large-growth corner of the style box. Yet Primecap has stayed with the stocks it likes. At last check, annual portfolio turnover at Vanguard Primecap was just 6%.

By holding on to its favorite stocks and industries, Primecap didn’t follow the rising valuations and growth rates that would have kept it in growth even as most of its large-growth peers did. The Primecap managers clearly value growth and competitive advantages, but they don’t give much thought to peers or the Russell 1000 Growth. The funds are benchmarked to the S&P 500, and managers are compensated based on it--though those designated as growth funds have consistently been in the growth side of the style box. Primecap’s long-term focus also means the managers worry less about one year’s underperformance.

That’s where they diverge from most growth fund managers. The typical growth fund manager is benchmarked to a growth index, and that makes it much harder for them to not own or even underweight the biggest growth names. Growth managers are largely paid to beat growth indexes, so avoiding those names is a big risk for wallet and employment.

So, no, it doesn’t look like Primecap has changed its stripes. But one of the more dramatic moves in market history has put some distance between Primecap and most large-growth peers.

Conclusion On a yearly basis, much of what at first seems to be skill or stupidity is really just a fund's industry biases shining through. Given that Primecap has succeeded over the long run, I'll be sticking with it.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

/d10o6nnig0wrdw.cloudfront.net/07-25-2024/t_56eea4e8bb7d4b4fab9986001d5da1b6_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/BU6RVFENPMQF4EOJ6ONIPW5W5Q.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/fcc1768d-a037-447d-8b7d-b44a20e0fcf2.jpg)