The ESG Fund Universe Is Rapidly Expanding

Record flows, strong performance, and other takeaways from the 2019 Sustainable Funds U.S. Landscape Report.

/s3.amazonaws.com/arc-authors/morningstar/42c1ea94-d6c0-4bf1-a767-7f56026627df.jpg)

After having steadily gained prominence over the past decade, sustainable investing appears to be reaching a tipping point in the United States, with many prominent asset managers and public companies beginning the year by making significant commitments to sustainability.

From fund investors and their advisors, I often get three big questions about sustainable investing: What does the universe of sustainable funds look like? Do sustainable funds have any performance limitations? And, finally, how do we know that sustainable funds are doing what they say they are doing?

I addressed these questions and more in the 2019 Sustainable Funds U.S. Landscape Report. Here are the key takeaways:

The sustainable funds universe grew to 303 open-end and exchange-traded funds in 2019, up from 270 the year before. The group has grown considerably in the past five years. At the end of 2014, it totaled 111 funds, and a decade ago, 100 funds.

Today, sustainable funds are available in open-end (221) and exchange-traded (82) formats; most are equity funds (219), but investors now can consider 57 fixed-income funds and 27 allocation funds. Overall, sustainable funds can be found in 67 Morningstar Categories.

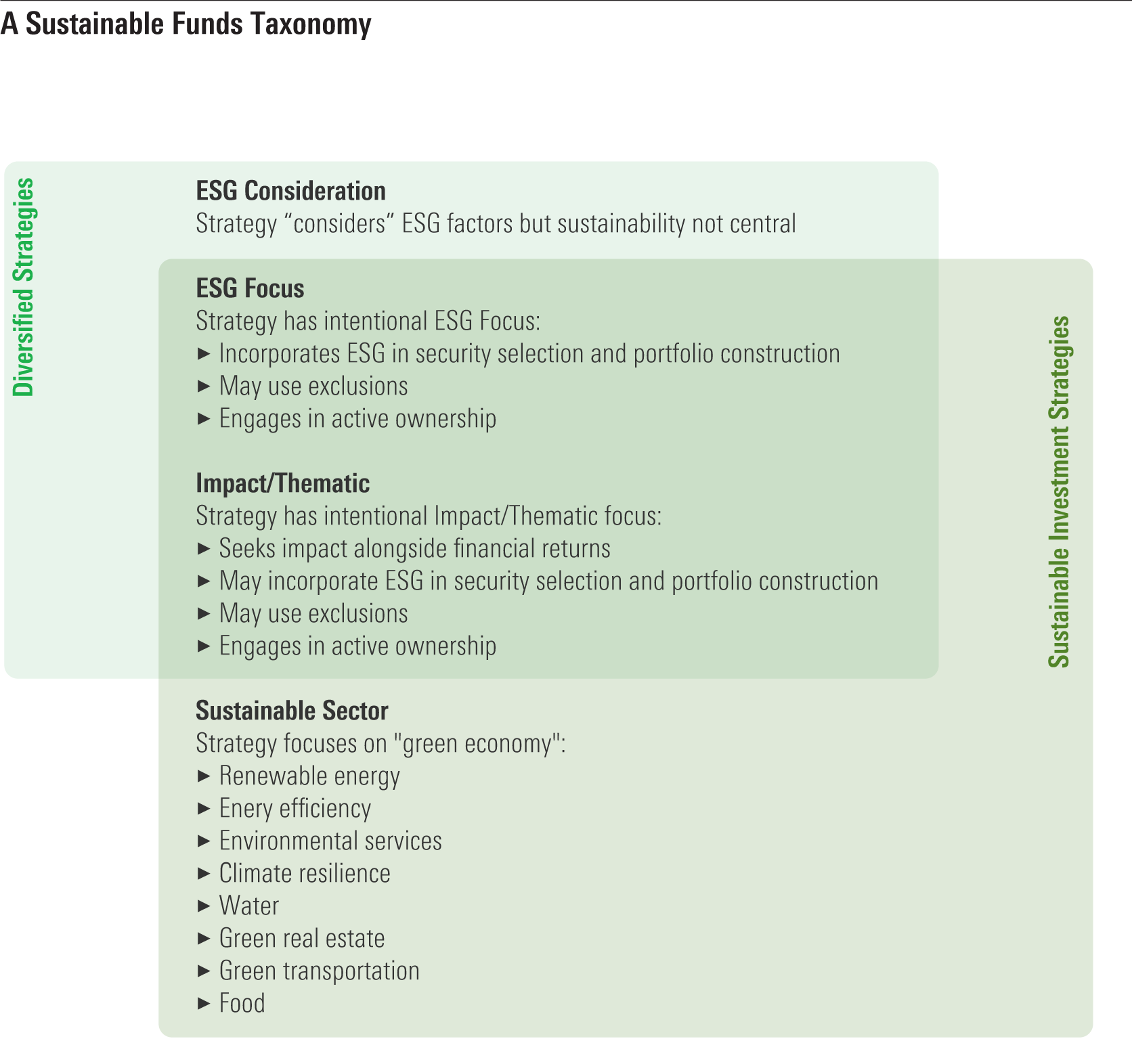

The taxonomy below describes three broad types of sustainable strategies: ESG Focus, Impact/Thematic, and Sustainable Sector. The first two are diversified approaches that can be used in lieu of conventional strategies commonly found in investor portfolios. While there is no discrete sustainable sector, Sustainable Sector funds are sectorlike portfolios focused on investing in companies associated with the growing "green" economy or focused on sustainability themes within an existing sector.

Source: Morningstar.

The number of otherwise conventional funds that now say they "consider" environmental, social, and governance factors has grown enormously, to 564 funds from 81 in 2018. To be clear, these funds don't appear to be marketing themselves as sustainable funds, and they do not claim that ESG is a focus of all their investment decisions. But the fact that nearly 500 funds added ESG consideration language to their prospectuses last year is an indicator that many asset managers are recognizing the importance of ESG in their investment process.

In selecting funds, then, sustainable investors might think of these so-called ESG Consideration funds as possible choices when an appropriate sustainable fund option is not available. Keep in mind, though, that all ESG Consideration funds are actively managed.

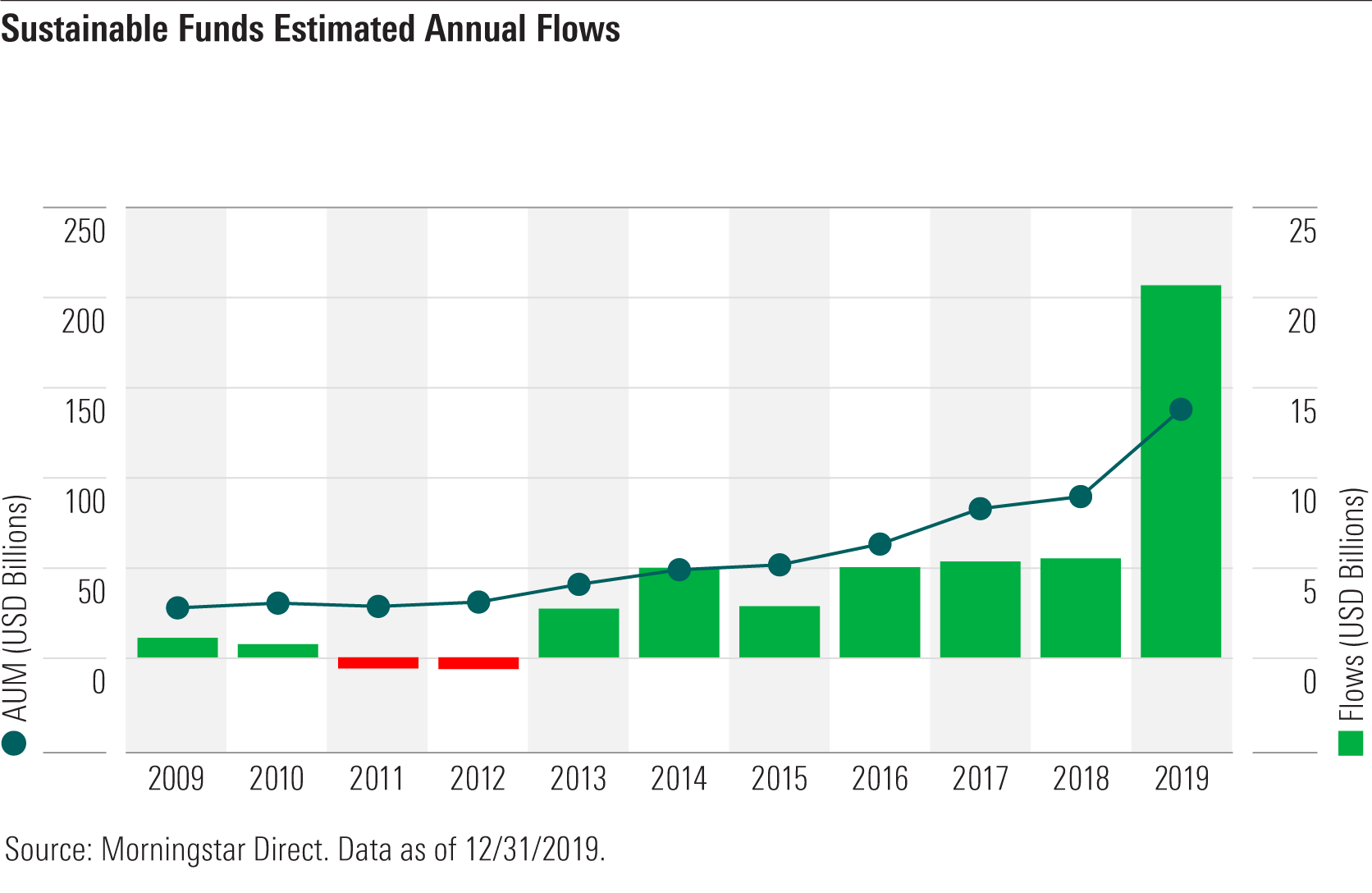

Flows into sustainable funds totaled $21.4 billion in 2019, a nearly fourfold increase over the previous calendar-year record, which was set in 2018.

Sustainable funds outperformed their conventional peers in 2019, with 35% finishing in the top quartiles of their categories and 66% in the top halves. Their three- and five-year trailing annualized returns showed a similar pattern.

Sustainable funds overwhelmingly have 4- or 5-globe Morningstar Sustainability Ratings, indicating that they have lower ESG risk in their portfolios relative to their peers.

Investors should not assume all sustainable funds are fossil-fuel-free. In fact, only 10% of sustainable diversified equity funds have no fossil-fuel exposure.

While most sustainable funds exhibited high levels of support for ESG-related shareholder proposals last year, individual fund support literally ranges from zero (two funds) to 100% (17 funds).

In sum, the universe of sustainable funds has grown significantly, but all sustainable funds are not the same. Thinking of them as ESG Focus, Impact/Thematic, or Sustainable Sector may help investors better understand the range of sustainable funds available. While not full-fledged sustainable funds, ESG Consideration funds reflect the growing acceptance of ESG issues as material investment factors by mainstream asset managers. Performance shows that there is no reason to think that sustainable funds should underperform. As evidenced by their globe ratings, such funds hold companies with lower ESG risks. And while many sustainable investors may think all sustainable funds avoid fossil fuels and always vote proxies in favor of ESG-related shareholder resolutions, that's not the case.

Jon Hale has been researching the fund industry since 1995. He is Morningstar’s director of ESG research for the Americas and a member of Morningstar's investment research department. While Morningstar typically agrees with the views Jon expresses on ESG matters, they represent his own views.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/FGC25JIKZ5EATCXF265D56SZTE.jpg)

/d10o6nnig0wrdw.cloudfront.net/04-25-2024/t_d30270f760794625a1e74b94c0d352af_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/DOXM5RLEKJHX5B6OIEWSUMX6X4.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/42c1ea94-d6c0-4bf1-a767-7f56026627df.jpg)