Emerging-Markets Stock Fund Managers Face Tough Choices With Ukraine War

Here's what managers of Morningstar Medalist funds are saying about the outlook for Russian stocks.

/s3.amazonaws.com/arc-authors/morningstar/b41a1177-9e6e-486c-bb45-434ac569d47e.jpg)

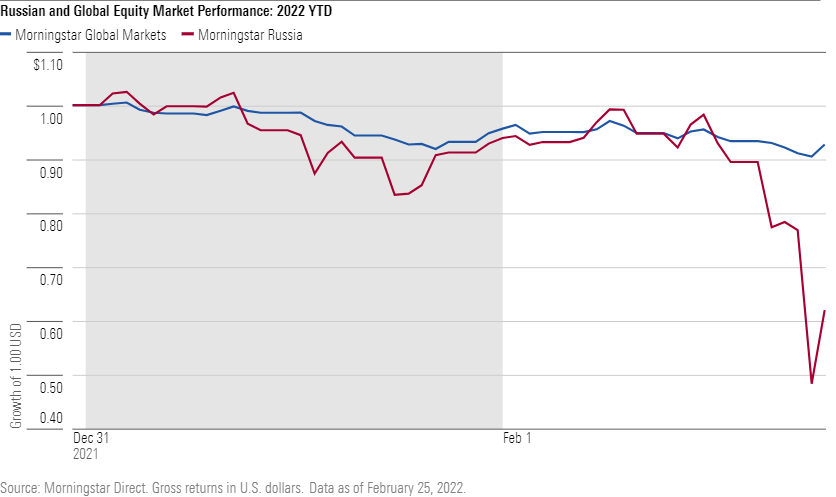

Russia's invasion of Ukraine has put active equity managers and their portfolios through a real-time stress test. Some, including at least one noted global stock-picker who had a lot invested in Russia, have dramatically trimmed their stakes. Others have adjusted the assumptions undergirding their investment theses and valuation estimates but stood pat.

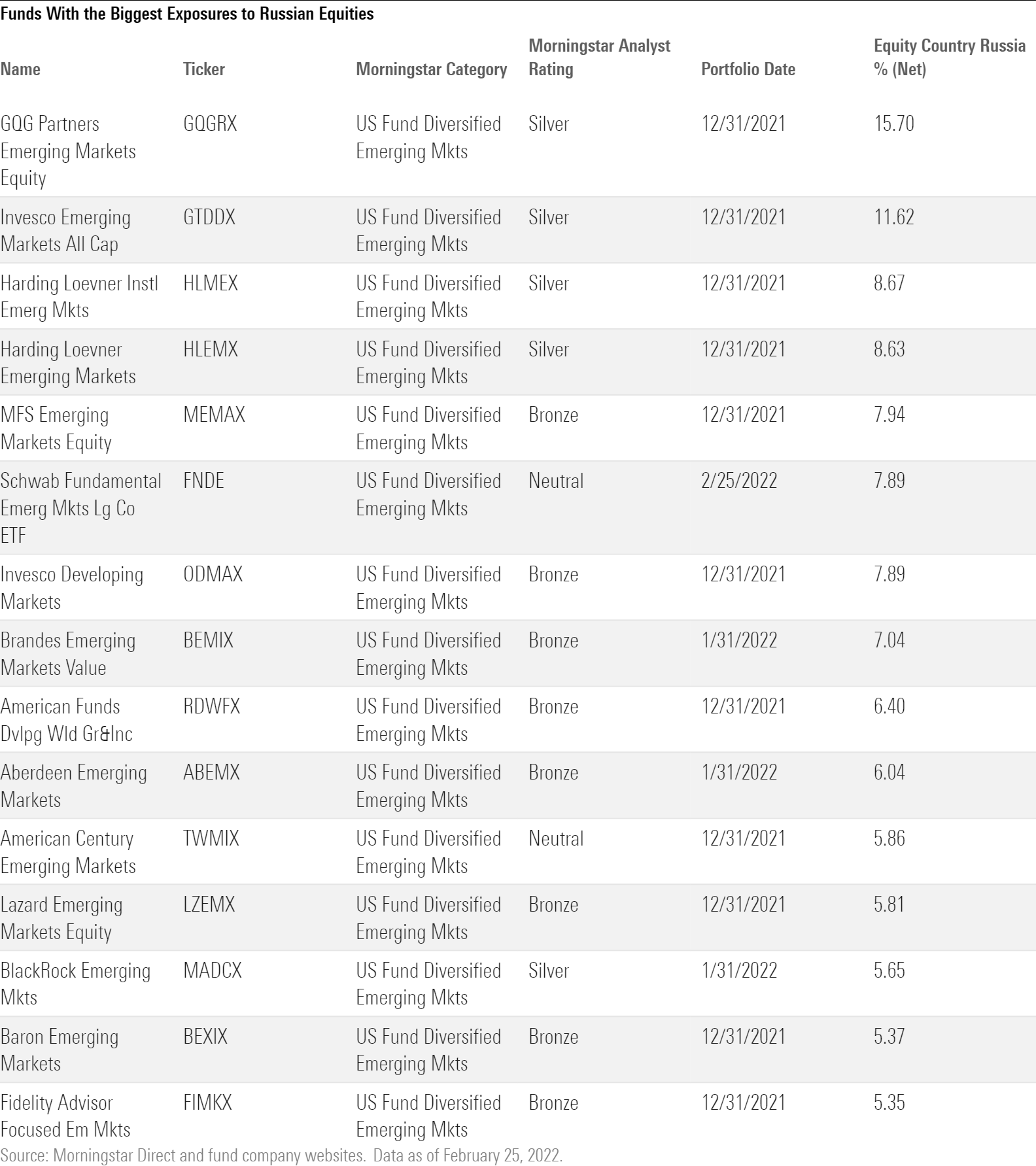

Last week we asked the managers of Morningstar-rated funds that had some of the largest stakes in Russian companies for their thoughts on the war and its market and portfolio ramifications. Those who had responded, as of Friday, Feb. 25, agreed the conflict and its consequences are frightening, foggy, and still fluctuating. "The events of the past week are clearly in the realm of the pessimistic outcomes we considered, and there is great uncertainty in how this will continue to play out," said Invesco Developing Markets ODMAX manager Justin Leverenz.

Indeed, no manager ventured an opinion on the possible course of the hostilities, and the group expected the number and severity of sanctions against Russian individuals, interests, and businesses to continue changing hour to hour and day to day. But many managers saw an increased likelihood of some broad effects, according to commentaries issued on Feb. 25:

- Markets will stay volatile.

- Current and potential sanctions will hurt but not permanently harm Russia's businesses and the global economy.

- The crisis has stoked rising energy prices and inflation and also increases pressure on central banks to tighten monetary policies.

- Russian equities have very low valuations, but the range of outcomes is wide.

- The managers we contacted said they would continue investing in Russian stocks as long as they had access to them and their fundamentals looked attractive, even as other big institutional investors moved toward divesting Russian equities.

- This is a long way from over, and investors must remain attentive, patient, and wary.

"Thus far, sanctions have been carefully crafted to avoid targeting energy markets as to avert the threat of global recession," said Invesco's Leverenz.

Brandes Emerging Markets Value's BEMIX managers cautioned, however, that the "sanctions imposed may continue to fuel a rise in energy prices and may further exacerbate inflationary pressures globally. That, in turn, may influence the pace and scale of global central-bank tightening, particularly in Europe."

The Fog of War

As for Russian stocks, "much will depend on how the situation in Ukraine plays out, over what duration and what the ultimate resolution is--clearly impossible to predict," wrote Pzena Emerging Markets Value's PZVEX management team. "It remains to be seen how direct and penal impending sanctions from the United States and its allies will be, and what effect they will ultimately have on the Russian economy. It is unclear which companies will be most impacted and whether sanctions will be as punitive as restricting ownership of existing debt and equity."

The proclaimed and promised penalties cut wide and deep, managers acknowledged. The decrees build on sanctions ordered after Russia's 2014 foray into Crimea and eastern Ukraine, touching a wider array of institutions and individuals, banning new debt and equity issuance, and forbidding the sale of advanced technology to Russia. Over the weekend global news organizations reported that the U.S., European Union, United Kingdom, and Canada would take steps to cut certain Russian banks off from the critical SWIFT global financial messaging and transaction network and to limit the Russian central bank's ability to access its foreign-currency reserves. Other countries banned Russian planes from their airspaces. So far, however, Western governments have not restricted Russian oil and gas purchases or barred investors from holding Russian securities. (An executive at index provider MSCI told Reuters on Monday, however, that it makes sense to remove Russian stocks from its benchmarks because the sanctions complicate buying and selling them.)

The fluidity of the circumstances convinced one prominent manager to chop his Russian stake. GQG Partners Emerging Markets Equity GQGRX, which has a Morningstar Analyst Rating of Silver, dramatically reduced its exposure to the country this year, a firm spokesperson said Friday. The fund's stake had been about 16% of assets in December 2021, according to fund disclosures, but the firm on Friday reported it only had about 3.7% of assets left in Russia. Fund manager, firm founder, and CIO Rajiv Jain told investors in a Feb. 24 conference call that he reduced the fund’s exposure to companies he thought would most feel the effect of sanctions. He did not name the specific stocks he had sold. At the end of December 2021, Russian companies, such as Sberbank, Gazprom, Lukoil, Rosneft, TCS Group were prominent positions in the portfolio. "The markets are obviously very volatile at the moment," the spokesperson said. "And we will aggressively add or cut risk as needed." Jain, a former Morningstar manager of the year, is renowned for his predilection for higher-quality stocks and vigilant risk control.

Pessimism Prevalent

Bronze-rated Invesco Developing Markets' Russia stake also shrank from 9% at the end of 2021 to about 4% as of Feb. 24. The Russian market's steep year-to-date drop probably had as much to do with the decrease as manager Leverenz's decisions. Despite the turmoil, Leverenz still likes the two stocks that accounted for 80% of the fund's Russia exposure--Yandex and Novatek--which have both plunged.

The market is giving Russian Internet and e-commerce company Yandex's search business a single-digit price/earnings ratio and ascribing no value to its other businesses, which include market-leading food delivery, classified advertising, media, and logistics ventures, Leverenz said on Feb. 25. Meanwhile, gas producer Novatek, which the fund has owned for 15 years, derives strong competitive advantages from its low-cost liquefied natural gas projects in northern Russia and had an attractive valuation even before the war jolted oil prices. "It has a strong balance sheet and what we consider to be unparalleled assets that we believe will support growth for years to come," Leverenz said.

Some managers were not pessimistic enough before the incursion. The team running Silver-rated BlackRock Emerging Markets MADCX thought the odds of warfare were unlikely after some team members visited Russia in late January as the country mustered more than 150,000 troops on its neighbor's boarder. The fact that the population did not seem primed for a full-scale invasion and other factors, including cheap valuations, argued in favor of maintaining the strategy's long-term positions in Russia, the team said on Feb. 16.

The team members quickly admitted they were wrong after Russian forces commenced their Feb. 24 assault but explained why they had doubted Russian President Vladimir Putin would follow through on his saber rattling. "This attack will lead to a significant loss of human life, something that we believe will be deeply unpopular in Russia, where many citizens have friends and relatives living in Ukraine," they said. The team also questions how Russia would ever truly exit the conflict.

The team is monitoring current and possible future sanctions' impact but does not think there will be "a blanket ban on owning Russian equities." Sanctions against individual companies, such as Sberbank and VTB Bank, would force them to reduce "residual exposure" (the fund did not own VTB at the end of January 2022 but had about 1.4% in Sberbank). The managers think, however, that the impact of any sanctions will be minor for their holdings, which included Lukoil, Gazprom, Magnit, and TCS, on Jan. 31. "Valuations are extremely distressed and therefore we have not sold significant amounts of Russia exposure in any funds on the platform," they said. But they also reserved "the right to change this stance as the facts emerge"--as they've done before.

Sberbank, one of the more widely held Russian stocks, is one of the sanctions' biggest targets because the state owns half of it. The bank has managed to operate under the capital-raising and debt-selling limits of sanctions imposed after Russia's 2014 annexation of Crimea and belligerence in eastern Ukraine. The restrictions leveled last week, however, prevent the institution from transacting with U.S. banks (European banks are expected to ordain similar injunctions), which could affect its intrinsic value, many of the managers said. That value could fall even further if the bank is one of the institutions booted off SWIFT, as many expect.

Permanently Impaired?

Sberbank, however, is still Russia's dominant bank with a strong balance sheet supported by mostly local deposits and a 22% return on equity before the crisis. And Russia could resort to its own, albeit inferior, payment system, or China's network. "Therefore, we believe the probability of permanent impairment of Sberbank's business is low," Pzena said on Feb. 25.

Pzena and other managers also noted "that Sberbank saw a similar decline in 2014 when Russia invaded Crimea, and the stock price rebounded up sevenfold the following eight years." Pzena Emerging Markets Value did not own Sberbank during that rally, though, according to Morningstar data. It added it in late 2021, however.

Besides Sberbank, Bronze-rated Brandes Emerging Markets Value owned a large oil company and some local firms that should be less vulnerable to direct sanctions, such as telecommunications company Mobile TeleSystems, holding company Sistema, and children's retailer Detsky Mir.

Sizing up the Risks

The odds of more rough markets ahead are high. The managers quoted said they had increased discount rates when valuing Russian businesses and were limiting the sizes of Russian and related holdings in their portfolios to account for their risks. While no one seemed ready to load up on Russian stocks, many echoed this observation from Brandes' team:

"[T]he initial market sell-off before wars or significant geopolitical events is often sharp, but … subsequently the market has often recovered, so it is important to be watchful and not over-react."

Morningstar analysts Gregg Wolper, Bill Rocco, Samuel Lo, Eric Schultz, Christopher Franz, and Andrew Daniels contributed to this report.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/FGC25JIKZ5EATCXF265D56SZTE.jpg)

/d10o6nnig0wrdw.cloudfront.net/04-25-2024/t_d30270f760794625a1e74b94c0d352af_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/DOXM5RLEKJHX5B6OIEWSUMX6X4.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/b41a1177-9e6e-486c-bb45-434ac569d47e.jpg)