Will Rising Rates Provide an Advantage for Value Stocks?

There’s more to consider.

/s3.amazonaws.com/arc-authors/morningstar/78665e5a-2da4-4dff-bdfd-3d8248d5ae4d.jpg)

After decades of mild price increases, inflation has reared its ugly head. The Consumer Price Index rose by 7.1% in 2021--the largest increase in any year since 1981. The Federal Reserve has indicated that it intends to raise rates several times this year to slow down economic growth and muzzle inflation.

We don’t know the path that interest rates will take. But the prospect of higher rates and the recent rebound among value stocks raises the question: Will rising rates provide an advantage for value stocks?

There is some evidence that value stocks perform well when interest rates and inflation are high. Value stocks outperformed their growth counterparts by almost 10 percentage points per year during the 1970s.[1] To begin to understand why, we can look at how stocks are valued, and the differences between growth and value names.

What’s a Stock Worth?

“What is a stock worth today?” ranks among the most difficult questions investors face. Analysts typically use discounted cash flow models to arrive at an estimate. While not precise, these models are a useful tool for understanding how various factors influence stocks’ value.

Discounted cash flow models weave together three inputs--future cash flows, discount rates, and time--to arrive at an estimate of value. While different measures of cash flow may be employed for various reasons, I’ll use dividends to simplify the discussion. The other two ingredients in the model, time and discount rates, will play a more important role.

The amount of time between the present and the date when a dividend is paid can greatly influence what a stock is worth today. All else equal, delaying a dividend payment further into the future decreases a stock’s present value. For example, a $1 dividend that an investor expects to receive five years from now, discounted at a rate of 5% per year, is worth $0.78 today. If that dividend were paid 10 years from now, its present value drops to $0.61.

Dividends are pulled to the present by accounting for a stock’s discount rate, or its expected rate of return. Interest rates are an input into stocks’ discount rates, which are a combination of a risk-free interest rate and an equity risk premium. The former is universal. The latter is a mashup of stocks’ market risk (beta) and stock-specific risks. Revisiting the previous example, if the $1 dividend payment received five years from today were discounted at a rate of 10%, its present value would be $0.62, or 16 cents (nearly 21%) less than the present value with a 5% discount rate.

Pulling both those levers further punishes a stock’s present value. If that $1 dividend was paid 10 years from now, and discounted at a rate of 10%, its present value would slip to a paltry $0.39.

The Value-Growth Tango

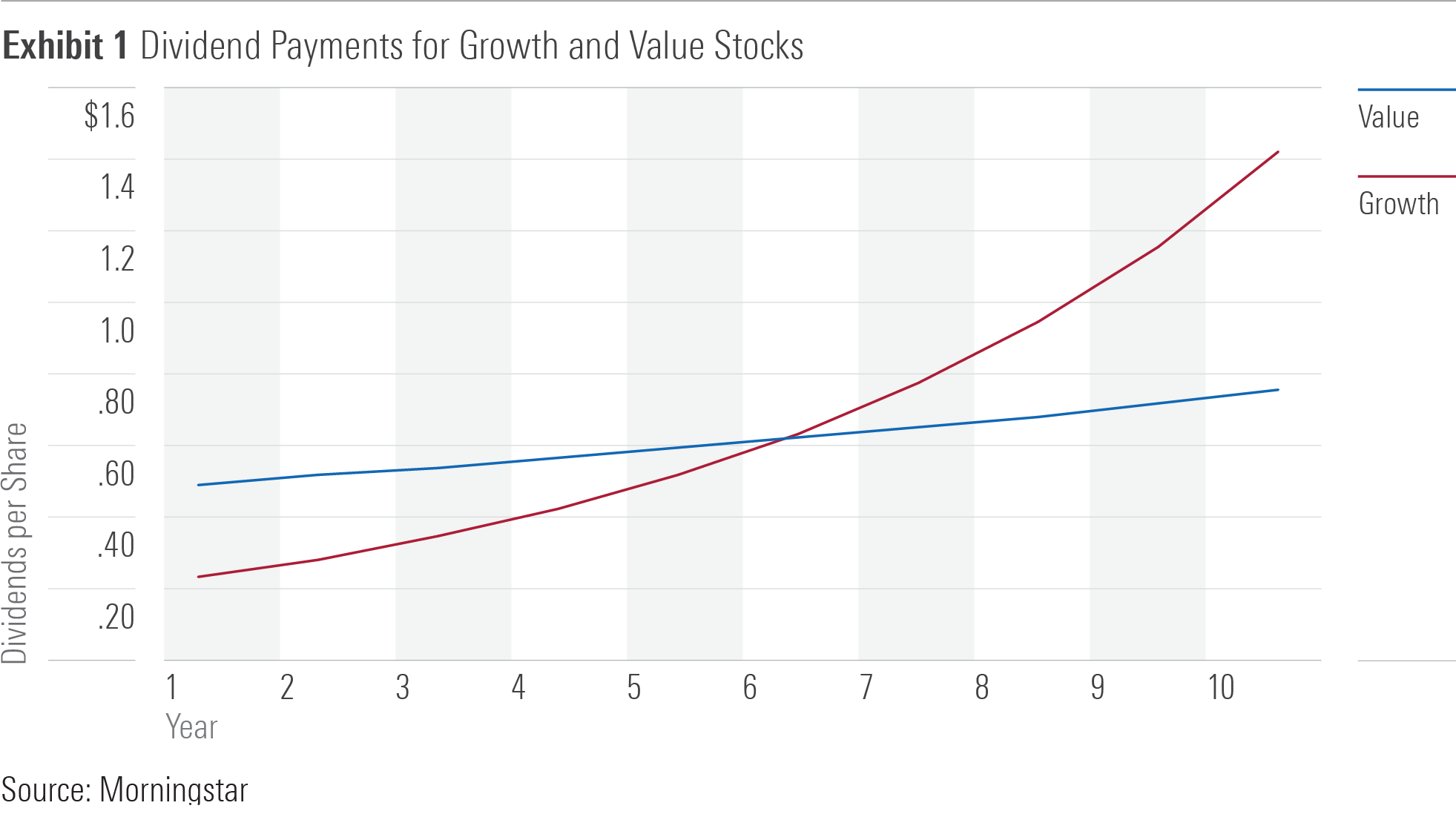

This basic dividend discount model can be applied to help understand what might happen as interest rates start to march higher, or interest rate expectations recalibrate. Let’s say two stocks currently trade at $10 per share. The first company has been around for decades and is highly profitable. It controls most of the revenue in its industry and has little competition, so its growth opportunities are limited. With few reinvestment requirements, it pays a healthy portion of its earnings back to shareholders through dividends: $0.50 per share over the next year for an expected yield of 4%. It slowly increases those dividend payments over time.

The second company is a young upstart that recently went public. Its products are disrupting its industry, and it became profitable only in the past year. It has tremendous opportunities to grow profits over time and reinvests most of its earnings back into its business. It will pay a smaller dividend of $0.23 per share next year (a 2.3% yield), but those payments are expected to grow at a faster clip over the next decade as profits increase.

Exhibit 1 shows what future dividend payments could look like for each stock over the next 10 years. The first company represents a value stock and the second company a growth stock. The dividends from the value stock are fairly steady over time, while most of the dividend payments received from the growth stock will occur further out in the future.

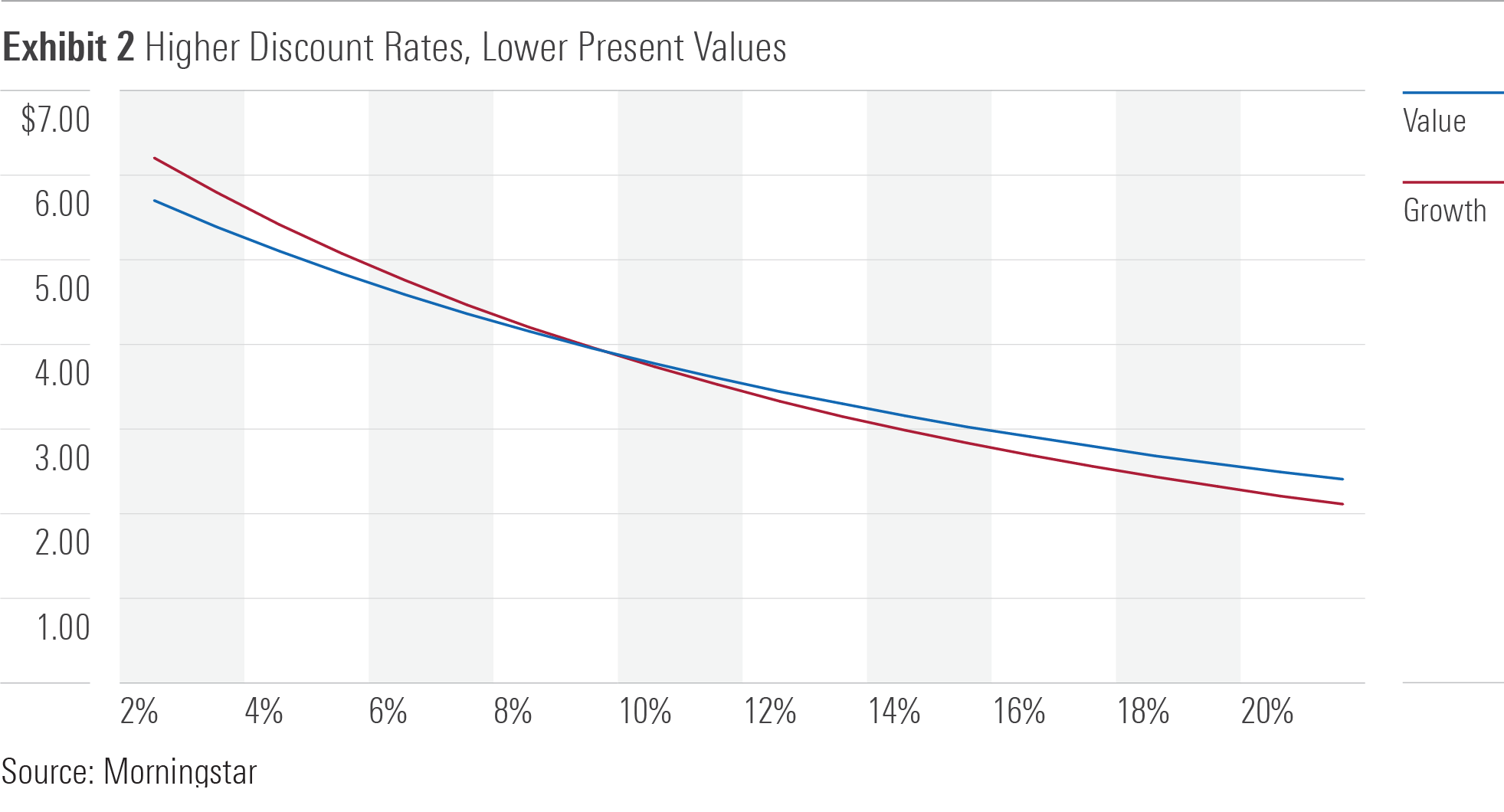

Exhibit 2 shows what happens when those dividends are discounted back to today across a range of discount rates. For both stocks, the present value is highest when discount rates are low, and it declines as discount rates increase.

The results highlight another subtlety. As discount rates rise, the growth stock’s present value declines at a faster rate than the value stock. Said another way, the growth stock is worth more than the value stock when discount rates are low, and less when discount rates are high.

The reason ties back to the earlier example of the $1 dividend. Most of the growth stock’s dividend payments occur further out in the future, making them more sensitive to higher interest rates than those of the value stock. That implies growth stocks’ present value, and subsequent performance, should be hurt more than that of value stocks when interest rates rise. More generally, growth should underperform value when interest rates rise and outperform when interest rates fall.

A Cloudy Crystal Ball

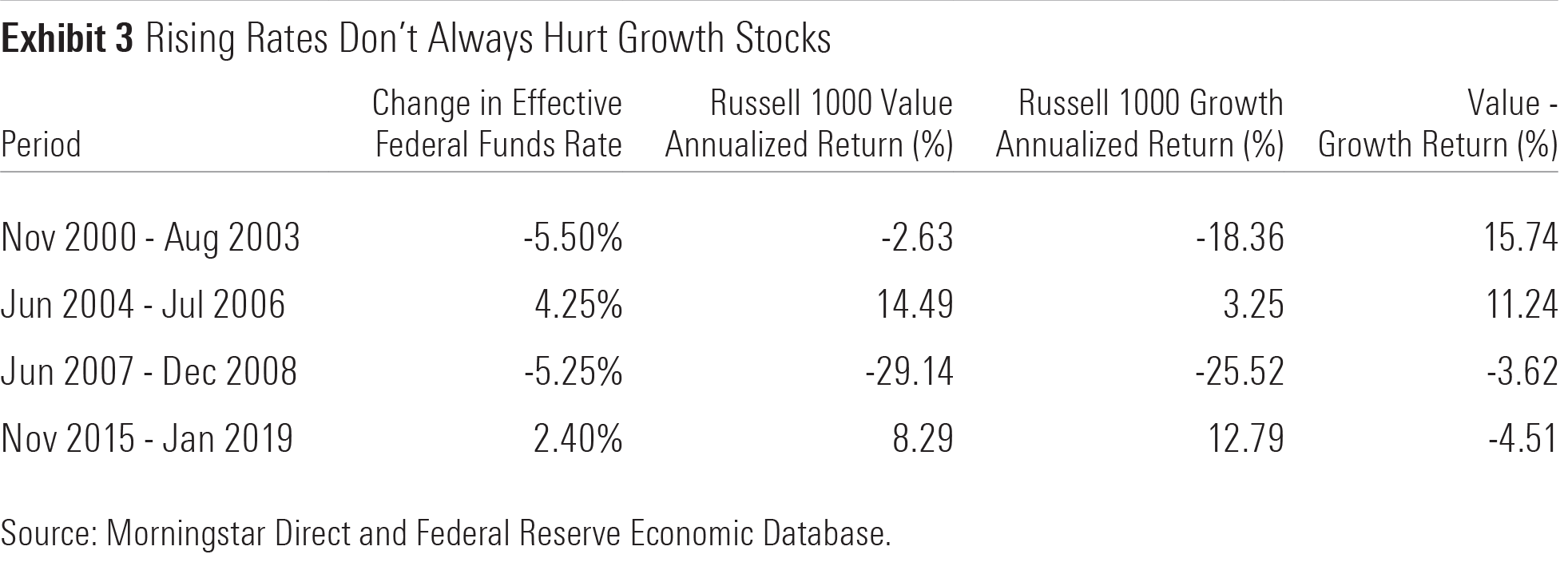

History tells us that financial markets almost never function in such a clear-cut way. Exhibit 3 shows the last four periods of interest-rate changes and the subsequent performance of the Russell 1000 Growth and Russell 1000 Value indexes.

Over these four periods, stocks performed poorly when interest rates were falling. Both value and growth indexes turned in negative total returns in the first and third periods. But that pattern is expected. Central banks typically lower interest rates to stimulate growth when the economy is struggling, which tends to coincide with poor stock market performance. Rising interest are meant to keep inflation in check by cooling down a booming economy and stock market.

In this limited sample, there does not appear to be a link between interest-rate changes and the advantage conferred to value or growth. The Russell 1000 Value Index outperformed the Russell 1000 Growth Index when interest rates dropped between November 2000 and August 2003. It also outperformed in the rising interest-rate environment between June 2004 and July 2006. The growth index outperformed in the latter two periods, regardless of the direction interest rates moved.

Admittedly, there are two shortcomings in this analysis that are worth touching on. First, I ignored the influence that interest rates have on future dividend payments. Such a connection is difficult to draw, though it seems reasonable to assume that the two are linked. Rising interest rates increase a company’s cost of borrowing, potentially denting future profits and dividends. The opposite may occur when interest rates decline.

Second, I assumed that stocks’ performance reasonably reflects their underlying value. But markets tend to be the least rational during exuberant booms and devastating drawdowns--the same periods when interest rates are likely to be changing.

Do interest-rate changes hold any power in predicting the relative performance between value and growth? Maybe. But interest rates are just one piece of the puzzle.

1) Using data from Ken French’s Data Library, stocks in the cheapest 30% of the market by price/book ratio outperformed the most expensive 30% by 9.97 percentage points per year between January 1970 and December 1979.

A version of this article previously appeared in the March 2022 issue of Morningstar ETFInvestor. Click here to download a complimentary copy.

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Morningstar, Inc. does not market, sell, or make any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/24UPFK5OBNANLM2B55TIWIK2S4.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

/d10o6nnig0wrdw.cloudfront.net/04-18-2024/t_34ccafe52c7c46979f1073e515ef92d4_name_file_960x540_1600_v4_.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/78665e5a-2da4-4dff-bdfd-3d8248d5ae4d.jpg)