Rating Foreign Small-Cap Index Funds

An updated review of process and price led to some changes in these Morningstar Analyst Ratings.

/s3.amazonaws.com/arc-authors/morningstar/78665e5a-2da4-4dff-bdfd-3d8248d5ae4d.jpg)

Morningstar rates three exchange-traded funds in the foreign small/mid-blend Morningstar Category, and earlier this year the Morningstar Analyst Ratings for all three changed.

The Morningstar Analyst Ratings reflect our level of confidence in a fund’s ability to outperform its category peers on a risk-adjusted basis over a full market cycle. This assessment rests on the same five pillars used to evaluate mutual funds: Parent, People, Performance, Process, and Price.

Broadly speaking, Process and Price are the most important pillars for rating index funds because they capture what an investor is getting and how much they’re paying. The assessment of an index fund’s investment process centers around its index construction methodology. Because the managers seek to track the index as closely as possible, they don’t have nearly as much influence on the fund’s category-relative performance as they would on an actively managed strategy. That said, it is still important to do due diligence on the index management team to ensure they can provide high-fidelity index-tracking with no surprises. All three rated foreign-stock small-cap index funds have Positive People ratings. They are managed by fully capable teams with access to similar technology and global trading desks.

These three funds also all have Positive Parent Pillar ratings. The Parent Pillar rating assesses the larger organization behind a fund, ensuring that fund sponsors are good stewards of investors' money. It is important to hold funds from responsible organizations, but the Parent Pillar rating has a smaller impact on the Analyst Rating because the characteristics of the fund itself have a greater impact on future performance.

With respect to performance, SCZ’s historic risk-adjusted return was among the best in the foreign small/mid-blend category, making it worthy of a Positive Performance Pillar rating. By comparison, SCHC and VSS had more exposure to firms from the materials and energy sectors than SCZ. Consequently, their category-relative performance suffered more when commodity and oil prices declined in 2012 and 2015, respectively. So, their risk-adjusted returns wound up near the bottom of the category, warranting a Negative Performance Pillar rating. That said, for index-tracking funds, past performance is typically used to determine if a strategy has performed as expected but carries less weight for determining what will happen in the future. Past is seldom prologue.

So, while People, Parent, and Performance are inputs in the Morningstar Analyst Ratings, they don’t move the needle nearly as much as Process and Price.

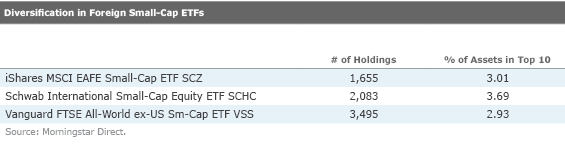

Process & Portfolio Morningstar generally takes a positive view of broadly diversified, market-cap-weighted equity funds. Strategies like these effectively diversify stock-, sector-, and country-specific risk, while mitigating turnover and trading costs. As a result, all three of these funds have a Positive Process Pillar rating. Each fund covers stocks from a different collection of countries, but all of them are well-diversified, both in terms of the number of stocks in each portfolio and their concentration (as measured by the percentage of assets in their 10 largest names).

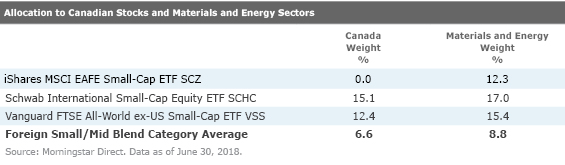

SCZ excludes Canadian stocks, which differentiates it from SCHC and VSS. Exposure to the Canadian market usually isn’t a concern with most foreign index-tracking funds because it accounts for a small portion of the international stock market. As of July 2018, Canadian stocks made up 6.6% of the MSCI ACWI ex USA Index. But their share in the small-cap segment is more pronounced, at roughly 12.5%. This is important because Canadian small caps carry a unique form of sector risk. More than 40% of the Canadian small-cap market is allocated to energy and materials firms--companies that are exposed to volatile commodity prices--making them riskier than many other industries.

Exposure to these sectors is consistent with each fund’s exposure to the Canadian market. Table 2 highlights each fund’s weights in Canadian stocks and its corresponding exposure to the materials and energy sectors. All three funds overweight these commodity-based sectors relative to the category average, but VSS and SCHC have heavier tilts because they include Canadian small caps.

It is important to remember that all three of these funds are well-diversified. That said, heavy exposure to commodity-centric industries reduces our confidence in their ability to outperform their peers. While we don’t take a view on sector-relative returns, we do know that the level of risk in the materials and energy industries is likely to be elevated by their commodity exposure. A bias toward these sectors means that all three of these funds--and VSS and SCHC in particular--are likely to be more volatile than the category average and have lower risk-adjusted returns as a result.

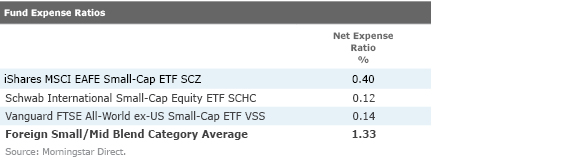

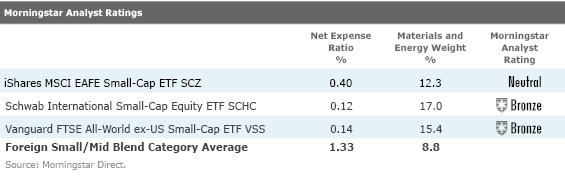

Price Cost is one of the best predictors of future performance, and it is especially important when deciding among similar funds. All three funds are cheap compared with the category average, which stood at about 1.33% as of July 31, 2018. SCHC is the cheapest in the category while VSS is only 2 basis points behind, so both have a Positive Price Pillar rating. SCZ is cheap compared with the category average and also rates Positive, but it isn't competitive with the other two.

Major considerations with these funds are their exposure to stocks from volatile sectors and their expense ratios. All three overweight stocks from volatile sectors relative to the category average, which detracts from their appeal in a big way. SCZ is cheap compared with the category average but expensive next to SCHC and VSS. For this reason, it ends up with a Neutral rating. The ultra-low expense ratios charged by SCHC and VSS partially redeem their bias toward volatile industries, so they both receive a Bronze rating.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/24UPFK5OBNANLM2B55TIWIK2S4.png)

/d10o6nnig0wrdw.cloudfront.net/04-25-2024/t_29c382728cbc4bf2aaef646d1589a188_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/78665e5a-2da4-4dff-bdfd-3d8248d5ae4d.jpg)