Jack Bogle Was Not Entirely Wrong About ETFs

While ETFs aren’t perfect, their virtues clearly outweigh their sins.

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

Too Easily Exchanged?

Jack Bogle, infamously, detested exchange-traded funds. In 2012, for example, he thundered that ETFs were “what happens when you have marketing people instead of investment fiduciaries running money. The ETF is the magic word of the day, the greatest marketing innovation of the 21st century. [Hey, he was on a roll.] They are absolutely speculation, and they have hurt a lot of people.”

I write “infamously” because even those who typically agreed with Bogle shunned his attack on ETFs. Vanguard itself had no such qualms about the new fund structure, launching its first exchange-traded shares in 2001. The firm has since become the industry’s second-largest ETF provider, slightly trailing iShares. Nor were other index-fund proponents fazed by the invention.

The marketplace concurs that Bogle was wrong. Last year, U.S. ETFs received $600 billion of net new assets, while conventional mutual funds endured almost $1 trillion in net redemptions. As my colleague Syl Flood reminds me, that latter figure can be interpreted positively, as it includes withdrawals from retirees who have profited massively from their mutual fund accounts over the years. Still, there’s no doubt that ETFs have become the nation’s investment of choice.

Bogle’s error was understandable. When ETFs were launched, promoters touted their liquidity. Unlike mutual funds, which price daily, after the markets close, ETFs can be constantly traded, as with individual stocks. Bogle countered that this benefit was merely putative. Nothing good happens after 2 a.m., or with fund transactions made by those who can’t wait until the day’s end.

True enough. What Bogle missed, however, was that retail investors would refuse the bait. Most investors bought ETFs not for their liquidity (or transparency, another ETF feature that received early attention), but for their convenience and tax efficiency. ETFs could be purchased from any brokerage firm, as opposed to only those that had relationships with the fund sponsor, and they made even fewer capital gains distributions than did indexed mutual funds.

Risky Businesses

But Bogle was correct in his secondary attack on ETFs: Their taste for high-volatility strategies. In the same interview that began this column, Bogle also criticized ETFs’ investment strategies, which, he argued, provoked shareholders’ baser instincts. By indexing specific segments of the stock market, or even—God forbid—owning commodities, ETFs tempted investors to speculate.

The attraction of specialized ETFs is obvious. When the sun shines, they can make a whole lot of hay. In 2022, the 10 best-performing U.S. funds, headed by the suitably esoterically named MicroSectors U.S. Big Oil 3x Leveraged Exchange-Traded Note NRGU, were all either ETFs or their relatives, exchange-traded notes. They notched great profits even during an otherwise bad year. Big Oil returned 202%, while the 10th fund on the list, ProShares UltraShort 20+ Year Treasury TBT, returned 94% (by betting heavily against long Treasury bonds).

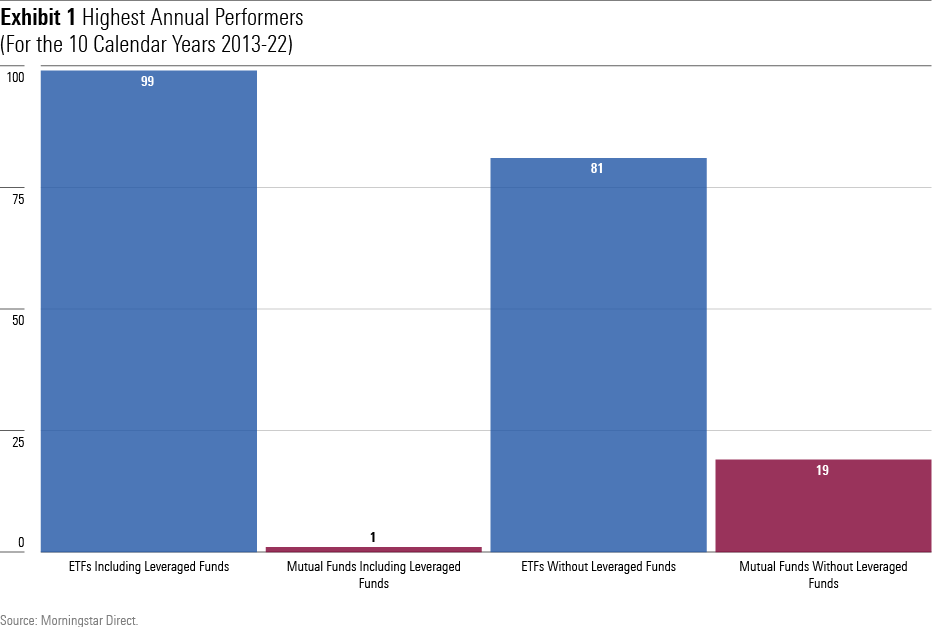

Stripping the leaders’ list of leveraged funds, which are mostly exchange-traded, reduces ETFs’ dominance of the leaders’ list but does not eliminate it. As shown by the chart below, which illustrates how many ETFs and mutual funds have been top-10 performers over the past decade, ETFs blitz the field when leveraged funds are included. Even when not, they still account for 81% of the winners.

(As the chart’s labels can be difficult to read, I will briefly explain. The blue bars represent ETFs and the purple bars mutual funds. The first set of bars includes leveraged funds in the count, while the second set omits them.)

All fine and good—but we realize the corollary. What volatility giveth, volatility taketh away. Sure enough, that triple-leveraged Big Oil note lost almost 94% of its value two years previously. Which means that the combination of its 165% rebound during the succeeding year and even larger 2022 gain has enabled the ETN to recoup only half its losses. It now sells at 50 cents on its original dollar.

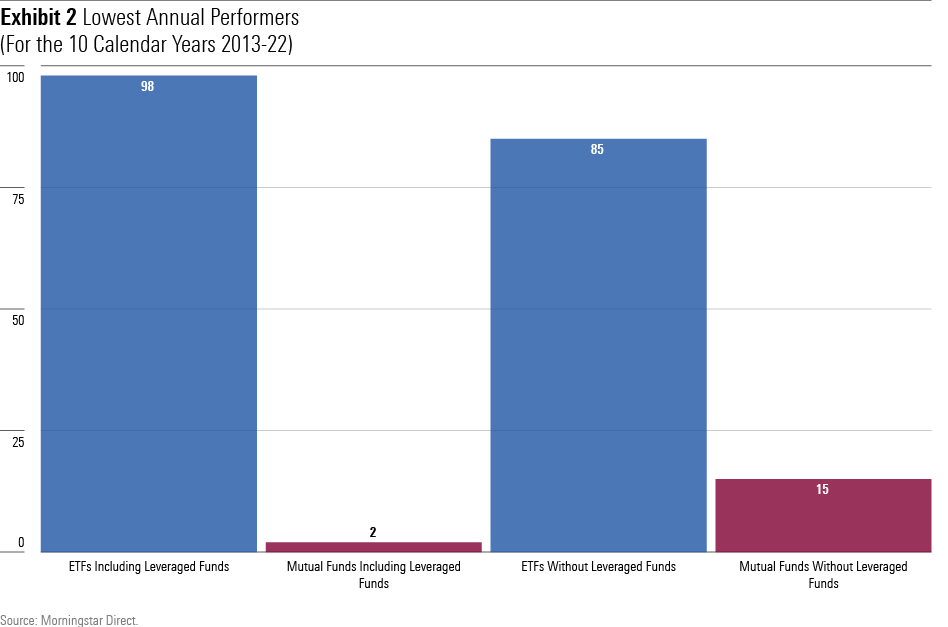

Unsurprisingly, the losers’ list also dramatically favors ETFs.

Going to Zero

Such highly volatile funds pose two problems. One is that shareholders use them badly. They buy high, sell low. Consequently, specialized funds consistently record poor investor returns, as discussed in this article from Morningstar’s Amy Arnott.

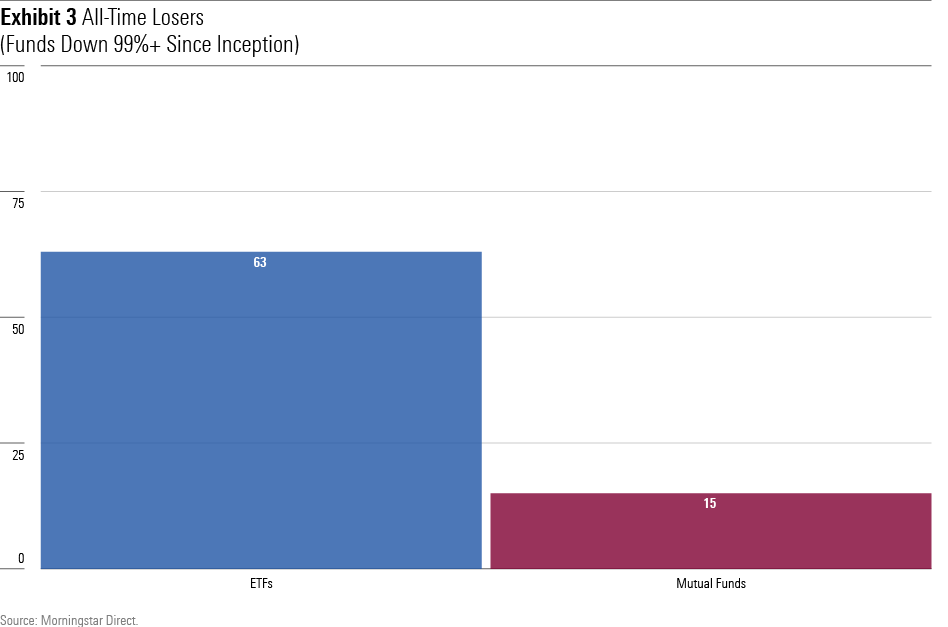

The other is that performance does not always revert to the mean. Sometimes—especially with leveraged funds—returns keep spiraling downward until they descend too far to ever recover. Since 1980, 78 funds have posted cumulative total returns of less than negative 99%. (Yes, really.) Most of them have been ETFs. Indeed, 1% of all ETFs that ever existed have suffered that fate. Ouch!

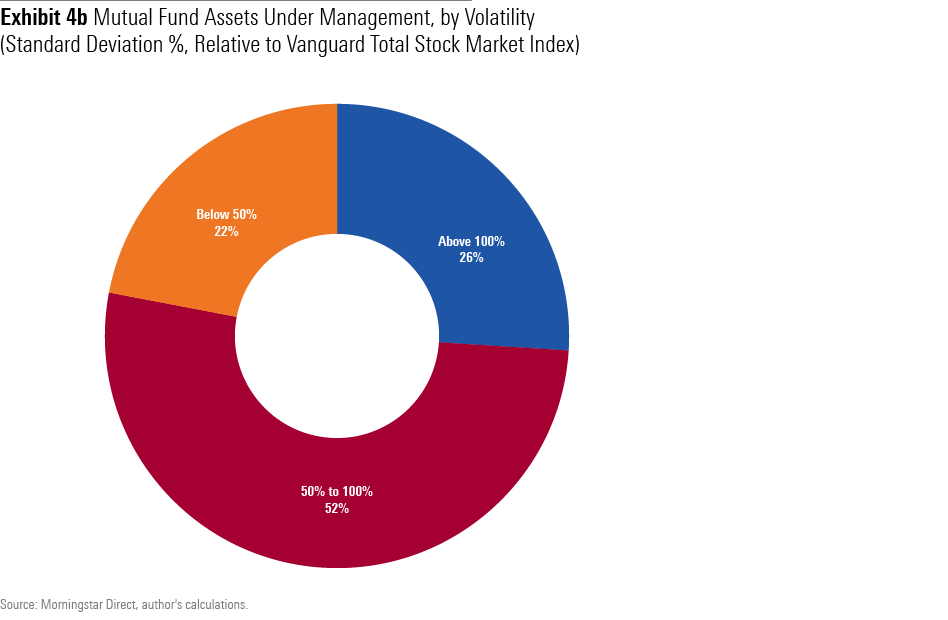

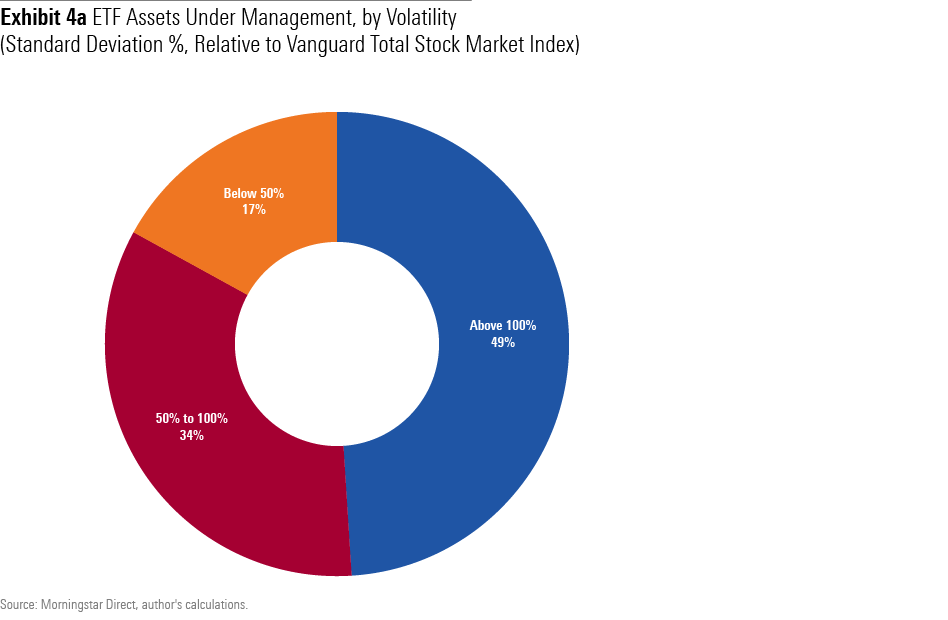

It will be protested that the riskiest ETFs pose little practical threat, since they possess few shareholders. Yes and no. It is true that retail buyers typically shun such funds, which, if used at all, tend to be institutional trading vehicles. But, in aggregate, ETFs are invested much more speculatively than are mutual funds.

The blue slices in the charts below represent assets in funds that have been riskier than U.S. equities, as measured by the trailing three-year standard deviation of Vanguard Total Stock Market Index VTSMX. Only 26% of mutual fund shares qualify. However, 49% of ETF moneys surpass the mark. An investment-management constituent that holds half its assets in funds that are more volatile than a 100% equity portfolio is an aggressive constituent indeed.

Conclusion

There’s no question that ETFs were a happy invention. They have assisted in the index fund revolution, which has benefited investors (although not fund companies) by reducing costs, minimizing taxable distributions, and encouraging shareholder patience. Most ETF owners use their investments appropriately.

That said, ETFs also qualify for a less prestigious honor: the home of the industry’s riskiest funds. Mutual funds occasionally hit walls that ETFs cannot, by owning private-placement securities that are off limits to ETFs (because of their pricing mechanisms). In general, though, speculators prefer ETFs, as Bogle feared. Fortunately, there also been far fewer speculators than he anticipated. In this case, he surely would be pleased with his mistake.

The author or authors own shares in one or more securities mentioned in this article. Find out about Morningstar’s editorial policies.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/G3DCA6SF2FAR5PKHPEXOIB6CWQ.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/6ZMXY4RCRNEADPDWYQVTTWALWM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)