Where to Invest Amid Higher Interest Rates

History provides a guide for adapting your portfolio.

/s3.amazonaws.com/arc-authors/morningstar/0fa19b38-60f6-4a0f-9e06-9869d9c57d52.jpg)

Interest rates were extremely low for a long time—so long that a federal-funds rate near 0% started to feel normal. Foreign sovereign debt was issued with negative yields; Austria even sold a 100-year bond with a 0.85% coupon that matures in 2120. However, history tells us near-zero interest rates are anything but normal.

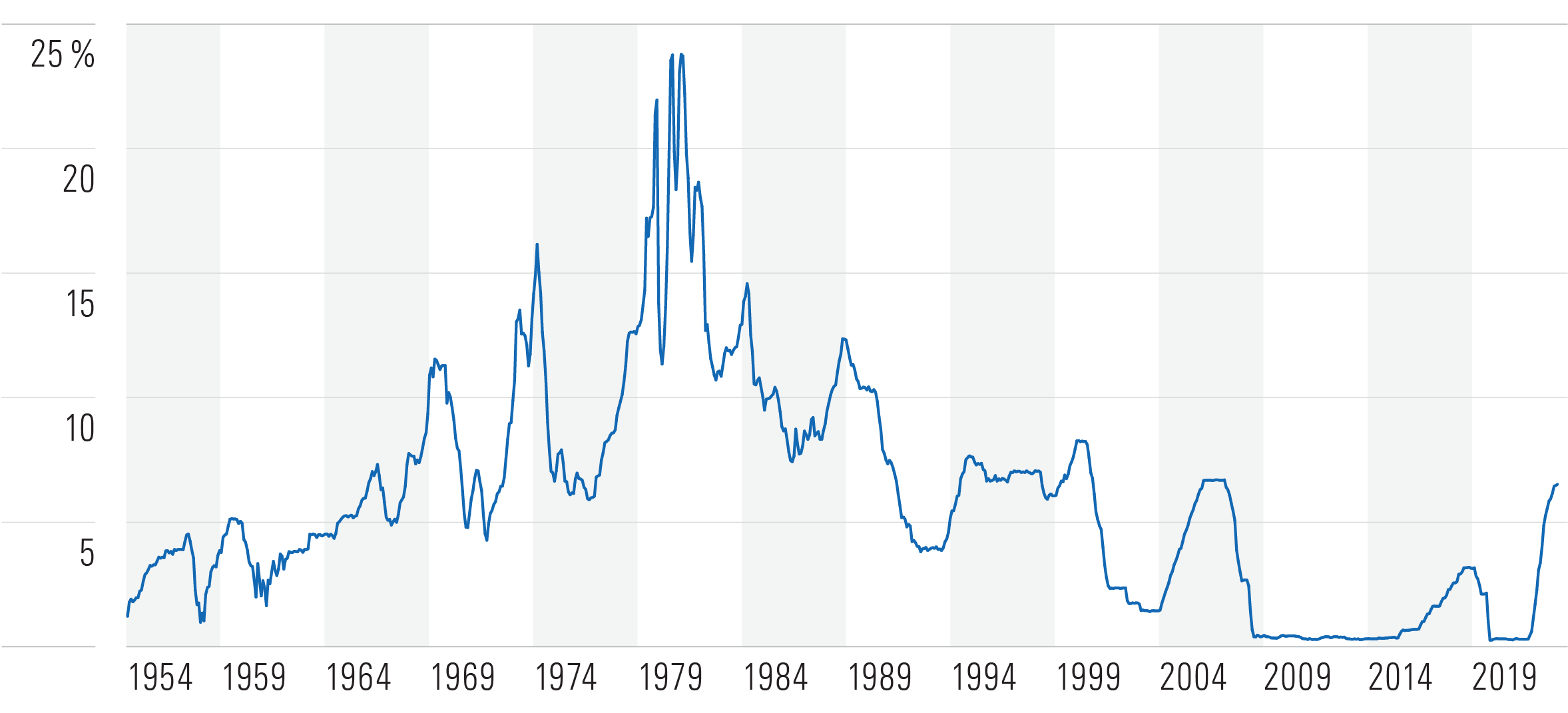

Since 1954 (the earliest date that data was available on the St. Louis Federal Reserve website), there have been 123 months when the effective federal-funds rate was below 0.60%. All 123 observations came during or after the global financial crisis in 2008. Prior to 2008, there were more months with a federal-funds rate above 15% than there were below 1%. The current rate of 5.25%-5.50% falls in the 33rd-highest percentile of observations. While high by recent standards, current interest rates are not even approaching historical extremes.

The Fed-Funds Rate Has Been a Tale of Two Generations

Based on the yield curve, it appears that the market expects interest rates to fall back down to normal levels, but “normal” is a misnomer for interest rates. History gives us little guidance on where steady-state interest rates lie. The bond market certainly believes it is lower than the current target rate offered by the Federal Open Market Committee. The yield curve has already priced into future rate cuts, some of which are in the not-so-distant future. This has led to an inverted yield curve—one in which short-term rates are higher than long-term ones.

Since the Fed began hiking interest rates in earnest, bond traders have continuously had to push back their predictions of when the first rate cut would take place. The Fed remains hawkish, and its position is somewhat understandable. There is little incentive for it to cut rates. Inflation has proved somewhat sticky, albeit declining. The jobs market continues to run hot. Calls for a recession are starting to wane.

For all the reasons above, I don’t see the Fed substantially cutting rates anytime soon. A wide range of outcomes still exists for the market over the short to medium term. Rates could push incrementally higher if inflation stays above the Fed’s target. Rates could also drop if there is a shock to markets, the economy, or jobs that require Fed intervention. But I expect that interest rates will remain elevated for a while as a base-case scenario. Investors can position their portfolios to take advantage of current interest-rate levels and the investments that work best here, while also hedging their bets against higher or lower interest rates.

What Investments Perform Better When Interest Rates Are High(er)?

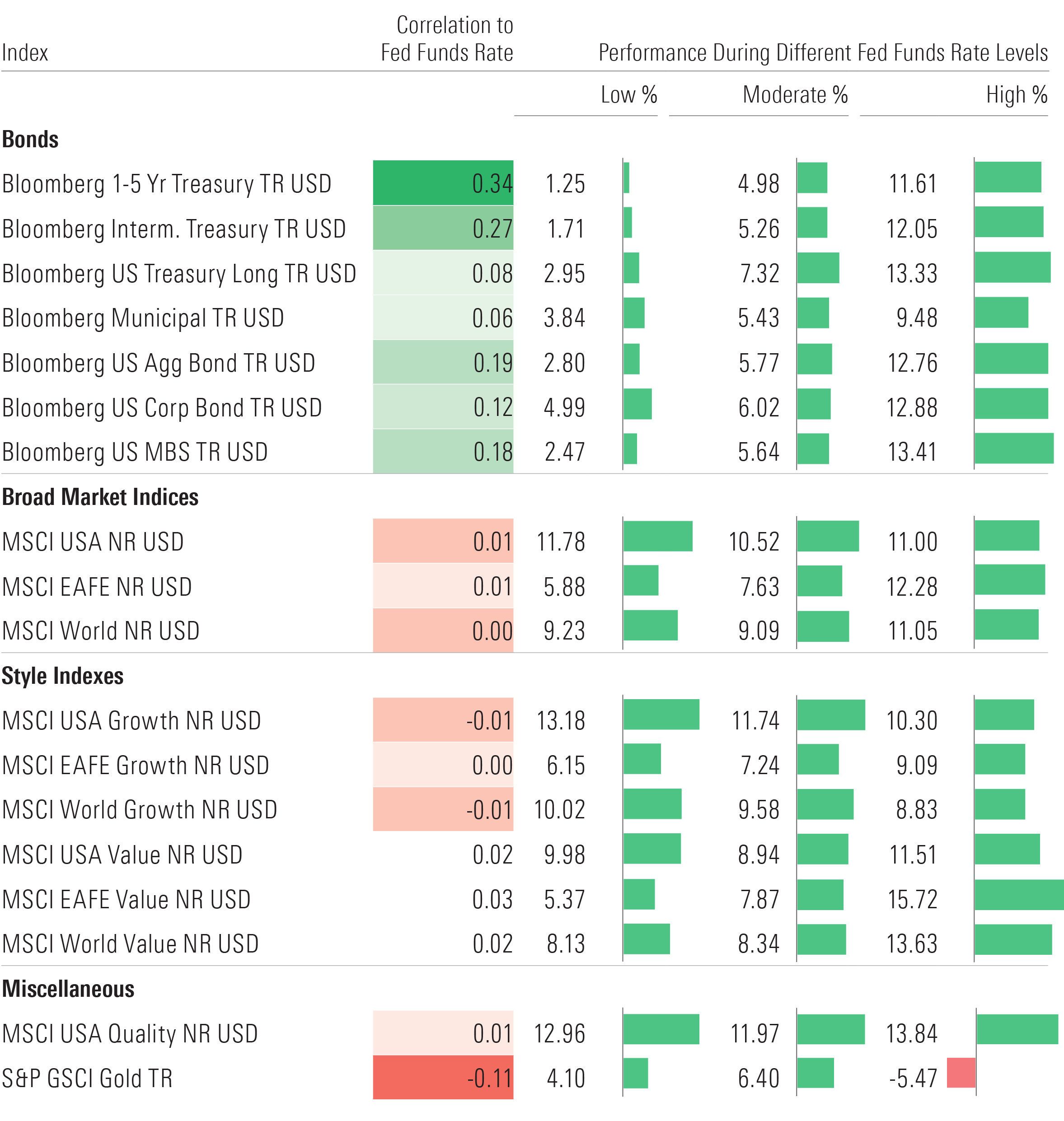

If higher interest rates stick, what does that mean for investors? To test this, I looked at the performance of several major indexes back to 1980 and averaged returns across different federal-funds rate levels. Rates falling in the bottom quartile were labeled “low,” the middle two quartiles “moderate,” and the top quartile “high.” The breakpoints were a federal-funds rate of 0.975% for the bottom quartile and 6.465% for the top quartile. I also tested the correlation of each index’s returns with federal-funds rates to look for high-level patterns that investors could profit from. The exhibit below details my findings.

Index Performance at Different Interest-Rate Levels

A disclaimer before we begin analyzing results: This backtest is indicative of the economies and markets of their time and may not be reflective of current conditions. Performance will not precisely repeat itself. But there are still patterns to be gleaned that should increase investors’ odds of success. With that said, here are the top findings.

Bond investors benefit from higher interest rates. Bond indexes were the only ones that clearly exhibit a positive correlation with the federal-funds rate. This is intuitive. Higher yields increase the odds of higher total returns for bonds. Bondholders also benefit when rates drop, which is much more likely at higher levels than low. The difference is starkest for Treasuries. The Bloomberg Intermediate Treasury Index returned just 1.71% when interest rates were low, but it jumped to 5.26% when they were moderate and exploded to 12.05% when interest rates were high. Investors should consider bonds a worthy component of their portfolios at current interest-rate levels, and they should consider adding more should rates jump higher.

Value stocks benefit from higher rates, while growth stocks trend in the opposite direction. Various ideas have been floated about why value should outperform growth amid higher interest rates. One theory claims that the cash flows of growth companies are more distant, therefore a higher discount rate affects their present value more than value stocks. Others center around the increasing difficulty and cost of raising cash for companies that burn through it. Performance trends support this: The MSCI World Value Index’s performance increased from low to high interest rates, while the MSCI World Growth Index’s performance declined between each level. But interest rates are not the only factor for growth and value stocks, and the growth index still beat the value index at moderate interest-rate levels. Based on trends, now is a good time to tilt toward value stocks, but it is not a panacea. Investors should not rid themselves of growth stocks just because of moderately high interest rates. Diversification still matters, and growth stocks are still worthy of long-term allocation.

Credit risk tends to pay off most when interest rates are low. Treasuries do the trick at higher interest-rate levels, when duration risk dictates much of performance. Alternatively, buying corporate bonds works best when spreads widen, which often comes after the Fed pumps markets full of cheap money at low rates.

Credit spreads tend to blow out when economic conditions deteriorate, after which the Fed is likely to cut rates to the bone to help boost the economy. We, as investors, tend to exaggerate extremes, which causes prices to swing past rational risk-adjusted expectations, both to the upside and downside. Often the best time to buy credit-risky bonds is when risks are highest, and vice versa. As Warren Buffett said, be “fearful when others are greedy, and greedy when others are fearful.” Credit risk is not at fearful levels. Ultrashort- to short-term Treasuries provide ample yield and are a better hedge for stocks.

Quality worked in all environments. The MSCI USA Quality Index was among the top two performing indexes when interest rates were low, moderate, and high. Steady and solid performing companies don’t often receive buzz on Twitter or at cocktail parties, but they performed extremely well for investors over the past 40-plus years. A tilt toward quality can smooth out returns for investors across many market scenarios and should play a central role in portfolios.

Relative performance of foreign markets is a mixed bag. The MSCI EAFE Index performed best when the United States had high interest rates. Yet, of its best 26 months relative to the MSCI USA Index, 24 came in the 1980s and early 1990s. This was during a period of extreme volatility for the U.S. dollar versus foreign currencies, which overshadowed local-currency performance. Likewise, foreign stock funds were decimated by a strengthening dollar over the past decade while interest rates were low. The test period was too noisy to draw conclusions given the high impact of currency fluctuations.

Setting Up a Portfolio for Success Amid Higher Interest Rates

Historical performance under different interest-rate environments gives us clues for how best to position portfolios. Trends suggest investors should increase their allocation to bonds, value stocks, and quality companies. Here are a few ways to best apply these trends in a portfolio:

- When steering their asset-allocation mix, investors should treat their portfolio like a cargo ship—not a kayak. Don’t try turning on a dime. Making small tweaks can improve the odds of success without becoming overly dependent on what appear to be rational outcomes. Overtrading and poor diversification can become a significant problem for investors when making large-scale tactical changes.

- Investors can hold a core lineup and make changes around the margins to increase value and quality exposures, or they can look for core exchange-traded funds that tilt toward those factors. A few of our favorite core ETFs with built-in value and quality tilts include DFA U.S. Core Equity 2 ETF DFAC, Schwab U.S. Dividend Equity ETF SCHD, and Vanguard Dividend Appreciation ETF VIG.

- Fixed-income investors should keep an eye on the U.S. Treasury yield curve. Ultrashort bonds carry the highest yields right now and deserve a bigger chunk than in recent years. But curves don’t typically stay inverted for long. Holding some longer-dated Treasury bonds adds convexity to a bond portfolio and does a better job offsetting a downturn in stocks should interest rates decline in tandem. A small allocation could go a long way in protecting against a recession.

This article first appeared in the August 2023 issue of Morningstar ETFInvestor. Download a complimentary copy of ETFInvestor by visiting this website.

4 Big Dividend ETF Upgrades in 2023

The author or authors own shares in one or more securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/24UPFK5OBNANLM2B55TIWIK2S4.png)

/d10o6nnig0wrdw.cloudfront.net/04-25-2024/t_29c382728cbc4bf2aaef646d1589a188_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/0fa19b38-60f6-4a0f-9e06-9869d9c57d52.jpg)