Commodities: Inflation Hedge or Fool's Gold?

The premium for inflation insurance may exceed the risk of inflation itself.

/s3.amazonaws.com/arc-authors/morningstar/0fa19b38-60f6-4a0f-9e06-9869d9c57d52.jpg)

A version of this article previously appeared in the November 2021 issue of Morningstar ETFInvestor. Click here to download a complimentary copy.

Investing in commodities always gains interest when the specter of inflation rears its ugly head. Research shows that commodities tend to be one of the asset classes that is most positively correlated with inflation, as calculated by the Consumer Price Index.

The CPI incorporates the prices of commodities like crude oil, natural gas, and agricultural commodities. Since 1991, energy-related commodities and broad commodity indexes, such as the S&P GSCI and Bloomberg Commodity Index, consistently exhibited the highest level of correlation with inflation of all commodities. Notably, gold did not exhibit any correlation with inflation over this period.

This trend continues today. In 2021, natural gas, oil, and broad commodity baskets have led the commodity universe in year-to-date returns, during a period where inflation fears have mounted. Investors have taken notice. Excluding precious metals, commodity exchange-traded products have garnered substantial inflows this year to the tune of over $6 billion, good for a 36.5% organic growth for the year to date.

Commodities also tend to be uncorrelated with the stock market, which could add a diversification benefit to portfolios. But commodities’ performance has been unpredictable during periods of duress in the stock market. In October 1987, the S&P GSCI, a broad index comprising 24 commodities, increased 1.05% while the S&P 500 dropped 21.54%. By contrast, in 2008 the S&P GSCI dropped 46% while the S&P 500 dropped 37%. Commodities may not diversify stock market returns when investors need it most.

Although commodities may not bail out drawdowns in the stock market, the S&P GSCI spot index managed to generate 6.24% in annualized returns over the past 20 years through October. This trailed the S&P 500 by 3.5% annually over the same period.

Given that they can hedge against inflation risks while generating decent returns and potentially diversifying stock market exposure, why aren’t commodities ubiquitous in portfolios? The short answer is roll yield.

Investing in Commodity Futures

The spot price of a particular commodity reflects the current price for immediate delivery of that commodity. Spot prices are broadcast in newspapers and via ticker tapes on TV, but they aren’t immediately relevant to investors. A commodity’s spot price may appear to compare closely to physically holding the commodity at first blush, but it fails to include the costs of storage and financing. Further, most commodities deteriorate over time. You would not be able to buy a bushel of corn and store it in your garage in the hopes of a big rally in corn prices next year because the corn would spoil, get eaten by vermin, and so on. Investors can’t simply buy and hold most commodities.

Aside from precious metals, the most common way to invest in commodities is through futures contracts. Futures contracts lock in a price at which you can buy or sell the underlying commodity at a specified future date. Investing in the nearest-to-expiration futures contract, also known as the front month-contract, is as close a proxy to the spot price there is. Continued investment in the front-month contract is achieved by selling the front-month contract and buying the next available monthly contract before the front month contract expires, a process known as rolling.

Rolling leads to roll yield. This is the positive or negative cost incurred when rolling from one futures contract into the next. Whether the roll yield boosts or drags on returns depends on the slope of the futures curve, specifically whether it is in contango or backwardation. Contango refers to when futures prices are above the spot price; backwardation refers to when futures prices are below the spot price. Contango decreases your purchasing power for the same commodity exposure by forcing you to sell the front-month contract for less than you pay for the next month’s contract. This causes a negative roll yield and creates drag on the total return of the investment. The opposite is true for backwardation, which can be a boon for returns.

ETPs track commodities using various methods. Some precious metals ETPs like SPDR Gold Shares GLD and iShares Silver Trust SLV are backed by physical gold and silver, respectively. ETPs tracking a single commodity that is perishable or expensive to store hold futures contracts instead. The most common commodity strategy is to track the front-month futures contract. Other funds make investments across two or more monthly contracts. For example, the United States 12 Month Oil Fund, LP USL holds an equal number of oil futures contracts across each of the front 12 months. Regardless of where ETPs invest along the futures curve, the impact of roll yield can cause deviations from a commodity’s spot price.

Contango Effects

Through the end of October 2021, the top-performing unleveraged commodity ETP was United States Natural Gas Fund, LP UNG. UNG tracks the price of natural gas by holding the front-month futures contract and slowly rolling into the next month’s contract over a week-long period each month. As of Oct. 29, 2021, UNG was up 120% for the year to date. UNG’s recent performance and correlation with inflation could create high demand for UNG and similar natural gas products, but a long-term look paints a different picture.

According to data from the U.S. Energy Information Administration, natural gas futures have been in contango during 85.5% of all months since 1997. During this span, the monthly average roll yield was negative 2.36%, while the median was a slightly less painful negative 1.39%. This means that the median roll will cost you an additional 1.39% per month on top of the fund’s already sky-high 1.35% annual expense ratio. This compounds to a negative annual roll yield of negative 18%. Ouch.

Natural gas futures experienced periods of extreme contango in 2020, as uncertainty about demand and the coronavirus pandemic led to a surge in volatility. Exhibit 1 illustrates the divergence of the S&P GSCI Natural Gas Spot Index from the S&P GSCI Natural Gas Total Return Index, which includes roll yield, in 2020. While the spot price of natural gas increased by 13% in 2020, the total return index lost 45%, highlighting the potentially swift repercussions from rolling up a futures curve in steep contango.

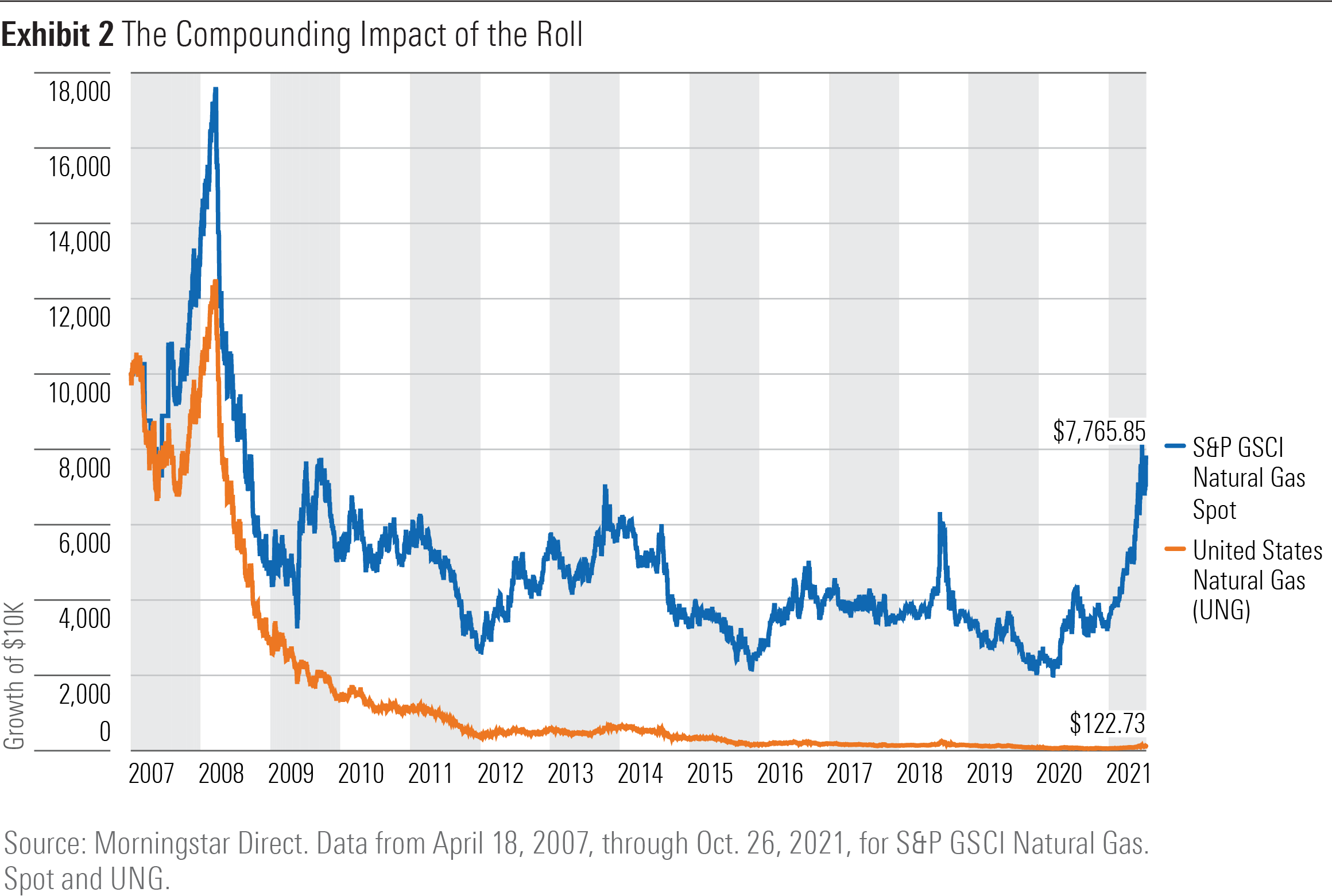

Given that UNG operates in much the same fashion as the S&P GSCI Natural Gas Total Return Index, it’s no surprise that the long-term implications of persistent contango have been extremely harsh for investors. Exhibit 2 illustrates the growth of a $10,000 investment in UNG compared with the S&P GSCI Natural Gas Spot Index since UNG’s inception in April 2007. Despite the tailwinds coming off a 119% increase year-to-date for UNG, the fund has still seen a cumulative decline of 99% since inception, while the spot index dropped 25%.

Fool’s Black Gold

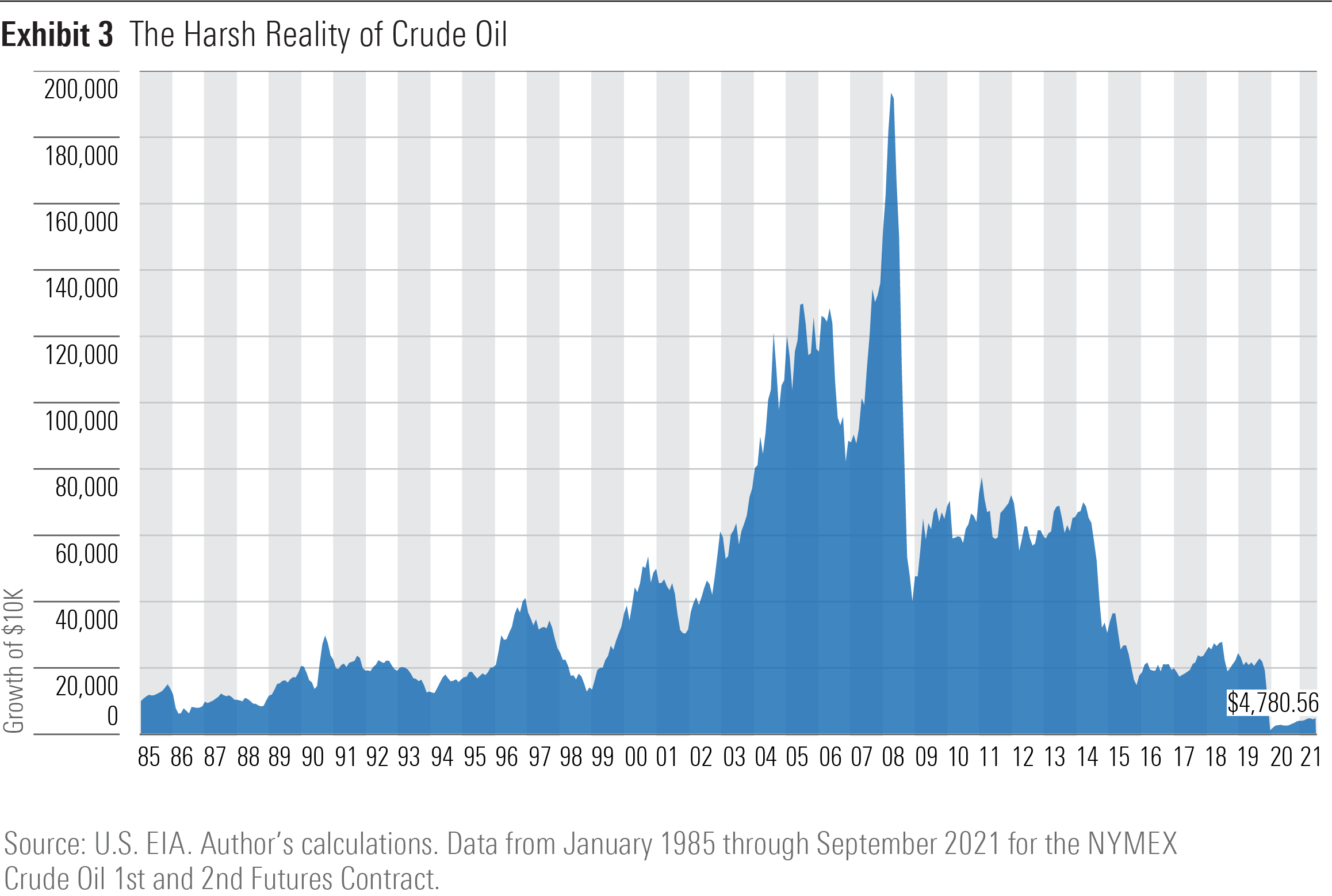

Of all commodities, crude oil has exhibited the highest correlation with CPI over the past 30 years.[1] It has also garnered the most investment of all commodity ETPs outside of gold and silver. Between January 1985 and June 2008, the total return from tracking the front-month crude oil futures contract was more than 12% per year, largely attributable to crude oil futures being in backwardation during 62% of all months during this stretch. This created an average positive roll yield of 0.52% per month on top of an appreciating crude oil price.

But backwardation in the crude oil futures market ceased after the price of crude oil tanked in late 2008. Since July 2008, crude oil futures have been in contango during 77% of all months. The average monthly roll yield over that span has been negative 1.12%. The total return of tracking the front-month crude oil futures contract since July 2008 was negative 27.5% annually, on average. The past 13 years have cratered crude oil’s overall performance since 1985, as illustrated by the growth of $10,000 chart in Exhibit 3.

Despite crude oil’s poor track record since 2008, United States Oil Fund, LP USO still holds more than $2 billion in net assets under management, the highest AUM for a single-commodity ETP excluding gold and silver ETPs. This has not benefited the fund, as USO averaged annual returns of negative 13.95% since its inception in 2006, resulting in a cumulative loss of 90.23% over its lifetime.

High Costs, Diminishing Benefits

USO and UNG illustrate the significant downside with buying and holding commodity ETPs. Investing in futures has resulted in significant deviations from the oil and natural gas spot prices that appear in monthly CPI. Oil and natural gas served as prime examples of the long-term implications of roll yield, but the same risk affects other commodities as well.

As originally stated, the S&P GSCI spot index returned 6.24% annually on average over the past 20 years. Switching over to the S&P GSCI total return index, which includes roll yield, reduces the average annualized return to negative 0.22% over the same period. Investing in commodities instead of ticker-tape spot prices (which aren’t investable) would have resulted in 240% less cumulative return over the past 20 years. Even worse, it came at a huge opportunity cost. Investing in the S&P 500 instead of the broad basket of commodities would have netted a cumulative return that was 550 percentage points higher.

Using commodities to hedge inflation and diversify equities exposure is akin to investing in a high-premium insurance policy: While you may eventually file a claim, the long-term premiums will likely dwarf the payout. Commodities may be useful as a tactical asset class in the face of inflationary pressure, but this strategy invokes the harsh reality of market-timing, where it’s often too late to capture the gains once you recognize the opportunity. This asset class best serves speculators, market makers, and arbitragers. Investors can find better options for managing inflation risk.

[1] For the purposes of this article, crude oil refers specifically to West Texas Intermediate (WTI) light sweet crude oil delivered to Cushing, Oklahoma, the main benchmark for oil traded in North America.

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Morningstar, Inc. does not market, sell, or make any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/XF7WENSYN5BFBFLPPFH7BJYUHE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/G3DCA6SF2FAR5PKHPEXOIB6CWQ.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/VUWQI723Q5E43P5QRTRHGLJ7TI.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/0fa19b38-60f6-4a0f-9e06-9869d9c57d52.jpg)