An 8% Retirement Withdrawal Rate?

A radio host advocates no small plans.

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

Thinking Big

Recently, a radio talk show host named Dave Ramsey recommended that retirees invest 100% of their assets in equities, from which they would withdraw 8% per year of the portfolio’s starting value, with each year’s expenditures adjusted for inflation. Thus, if inflation is 3%, the retiree would withdraw $40,000 in Year 1 from a $500,000 portfolio, $41,200 in Year 2, $42,436 in Year 3, and so forth.

If you listen to Ramsey’s statement, you will realize two things. First, nobody has ever been as certain of anything as Ramsey is about the accuracy of his counsel. (Or he’s acting—he is a performer, after all.) Second, he is deeply wrong. His argument relies on the overwhelmingly false assumption that stocks will consistently and regularly deliver double-digit returns.

Consequently, a host of “supernerd” researchers (to use Ramsey’s term for his critics) have dismantled his suggestion. This article, however, will take a different angle, by identifying the conditions under which Ramsey’s advice succeeds. The failures of his strategy will become quite apparent. But when does it work?

Time Horizon

The obvious way to withdraw aggressively from an investment portfolio without depleting it is...to die early. While generally not regarded as a desirable solution, expiring quickly does permit retirees to follow Ramsey’s advice. Even with Morningstar’s conservative assumptions, investors can safely withdraw almost 10% annually, inflation-adjusted, over a 10-year period. Easy pickings.

While that response sounds glib—and it is—the underlying point is serious. The only method for achieving a safe portfolio-withdrawal rate that is also satisfyingly high is to assume a short time horizon. Otherwise, something has to give. Guaranteed income provides security, but nothing approaching an 8% lifetime withdrawal rate. And risky portfolios are, well, risky. They might meet the need if the financial markets oblige. Or they might not.

The Great Depression

Let’s view history’s verdict on the viability of a 100% equity portfolio while funding 8% inflation-adjusted withdrawals. For each rolling 30 calendar-year period since 1926, I calculated the annual returns of a portfolio that invested 80% of its assets in U.S. large company stocks and 20% in U.S. small company stocks. (Generating the numbers necessitated, among other tasks, copying and pasting several dozen strings of total returns. Being a supernerd sometimes lacks glamour.)

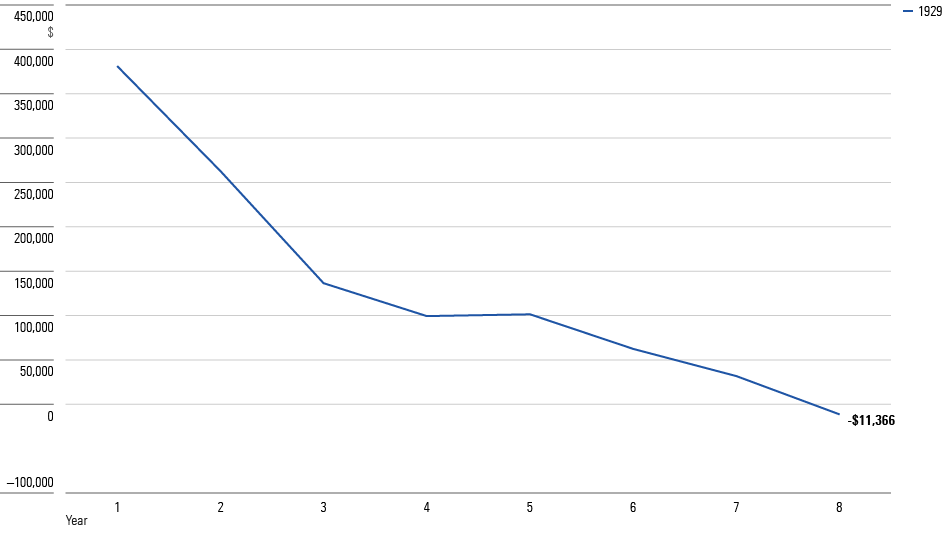

Below we see the outcome for those unfortunate souls who retired in January 1929, with an 8% portfolio-withdrawal strategy.

The Class of '29

Oh, dear. Remember when I wrote that achieving an inflation-adjusted 8% withdrawal rate for a decade was “easy pickings”? I omitted the fine print. Doing so calls for at least a modicum of bonds/cash to protect against stock market collapses. Of all possible portfolio strategies, short of employing leverage, Ramsey’s approach is the one that is likeliest to lead to immediate ruin.

Yes, you might respond, betting the house on stocks failed miserably when Herbert Hoover was president. Fortunately, things have since changed. When recessions commence, the Federal Reserve no longer responds by hiking interest rates while simultaneously permitting banks to fail. Also, Congress no longer stifles global trade by enacting steep tariffs. The only lesson to be drawn from the class of 1929 is the inapplicability of ancient history to the current era.

The Later Years

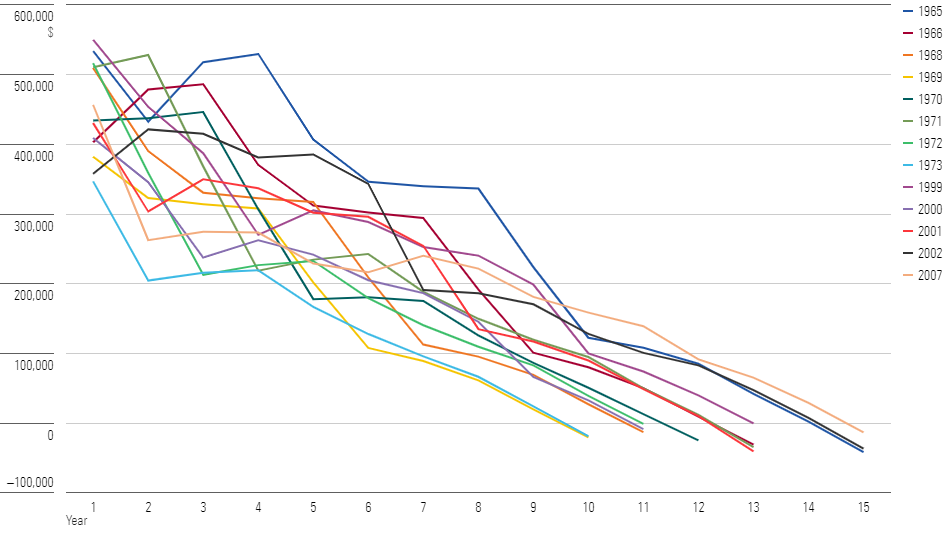

It’s true that when the Great Depression ended, a 100% stock portfolio almost always survived for at least 10 years. But on a baker’s dozen occasions since 1965, retirees adopting Ramsey’s strategy would have fared not much better, exhausting their investment pools before year 15 concluded.

Future Flops

As four of those implosions happened in this millennium, most recently in 2007, the Great Depression’s experience remains relevant. Today’s economy is different from 1929′s, and so are the federal government’s policies, but the potential for stock market disaster remains. Such is the nature of risky investments; if equities did not hold such dangers, they would not boast the high potential returns that an 8% spending rate requires.

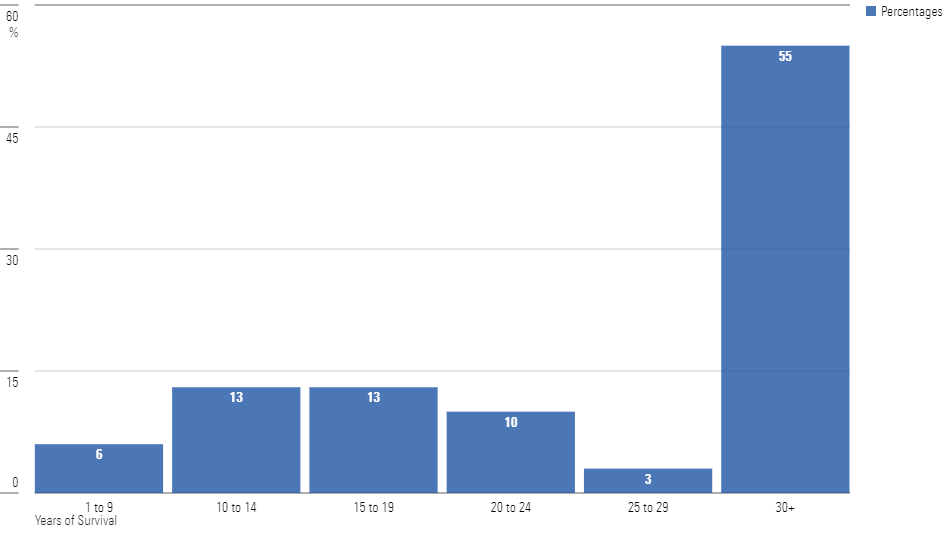

Here is another look. The data contains 68 completed 30-year horizons. The next chart shows the portfolio-survival percentages for those episodes.

The Track Record

The Little Girl With the Curl

Let’s start with the good news. With the 55% of occasions in which the portfolios survived through Year 30, retirees faced few worries when the period ended. In real terms, 80% of those portfolios were worth more after year 30 than when the investor retired. Their accounts had paid them handsomely for three decades yet were still flying high. Almost certainly, they would outlive their owners.

Unfortunately, the opposite precept also applies. As with the little girl with the curl, when the portfolios were good, they were very good. And when they were bad, they were horrid. Most of the portfolios that went bust before year 30 did so long before that date arrived. In 22 of the 68 incidences, representing 32% of the test cases, the portfolios failed to reach year 20. One could perhaps excuse those outcomes had they at least approached the 30-year mark. But they did not.

The Key to Success

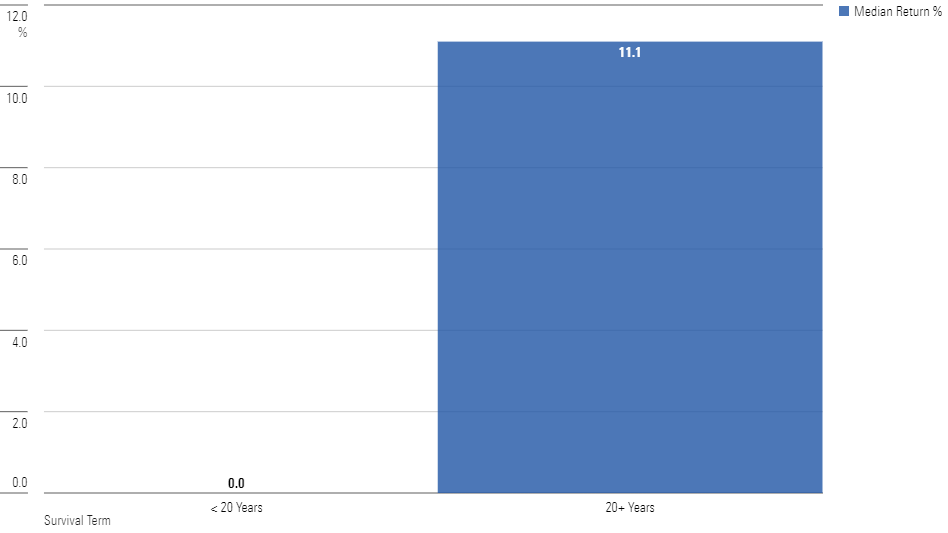

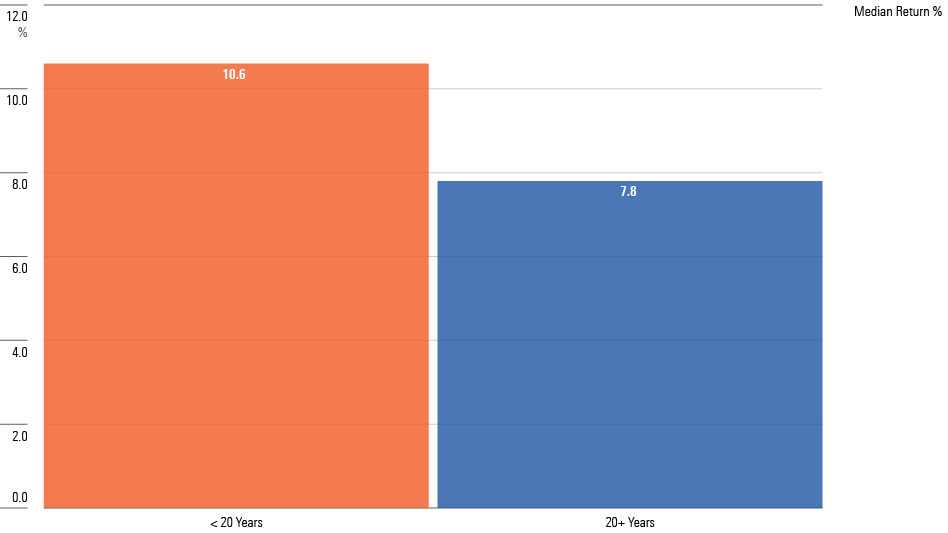

The biggest reason the portfolios cratered was slow starts. There is no hard-and-fast rule about how profitable investments must be to sustain an 8% real withdrawal rate. But they have to earn something! No retirement portfolio that suffered an overall real loss during its first five years survived for 20 years. In contrast, most of the winning portfolios enjoyed handsome early returns.

Below are the median annualized real returns during the initial five years of the retirement period for 1) the portfolios that did not live for 20 years and 2) those that did. The numbers amply support my claim.

The First 5 Years

In contrast, here is the same calculation, only this time measuring the annualized real performance of years 16-20. As demonstrated, later performances are largely beside the point. The early results are what really matter.

Years 16 to 20

Conclusion

History shows that portfolios adopting Ramsey’s strategy survive for 30 years slightly over half the time, and for 20 years on two thirds of occasions. Such odds may suit those who retire at advanced ages, say in their mid-70s, or who have severe health issues. As I wrote, short time horizons cure investment ills.

The wager is unlikely to suit those with longer expected life spans, however. The question then becomes, can the strategy be a useful starting point? That is, might retirees be well served by adopting a bold initial withdrawal rate—although probably not as high as 8%—and then adjusting in response to market circumstances?

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/G3DCA6SF2FAR5PKHPEXOIB6CWQ.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/6ZMXY4RCRNEADPDWYQVTTWALWM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)