Weighting Bonds by Market Value Isn't as Bad as Some Make It Out to Be

Doing so doesn’t wittingly expose investors to excessive risks.

/s3.amazonaws.com/arc-authors/morningstar/78665e5a-2da4-4dff-bdfd-3d8248d5ae4d.jpg)

A version of this article previously appeared in the April 2022 issue of Morningstar ETFInvestor. Click here to download a complimentary copy.

Investors have long looked to bonds to control risk in their portfolios. Most bonds are less volatile than stocks and commodities, and their correlations with both asset classes are incredibly low. The same holds for broad bond-market index funds, such as Vanguard Total Bond Market ETF BND, which carries a Morningstar Analyst Rating of Gold.

One of the criticisms foisted upon bond indexes, and funds that track them, pertains to how they weight bonds. Weights are typically assigned based on bonds’ market value. Market-value-weighted bond indexes assign the biggest weights to the largest bonds trading at the highest prices. So, the bonds from the institutions that have issued the most debt take up the largest positions in popular benchmarks like the Bloomberg U.S. Aggregate Bond Index (the index underpinning BND). At first blush, this seems foolish. Presumably, allocating your assets according to how much debt a company has placed with creditors adds credit risk. Credit risk is positively correlated with stock risk. So this would all seem to run against the grain of what a bond portfolio is supposed to do, which is tamp down risk and provide stability.

There’s no arguing against this premise. By definition, market-value-weighted bond indexes place the greatest emphasis on the institutions with the most debt. But the amount a borrower owes its creditors says nothing about its creditworthiness or its capacity to repay debt.

Broad market-value-weighted bond indexes have their flaws, but they don’t wittingly expose investors to excessive risks that could compromise performance. Furthermore, many of the alternatives to a broad market-value-weighted bond index exchange-traded fund have failed to deliver better long-term performance.

Pros

In the context of a broad-market bond index like the Aggregate Index, market-value weighting doesn’t necessarily increase risk—it may actually help control it. Bond prices incorporate the market’s collective view of each borrower’s creditworthiness. If a borrower’s credit rating declines, its bond prices should fall, and market-value weighting would assign a proportionally smaller weight to what is arguably a riskier bond. The opposite occurs when a borrower’s credit rating improves and its bond prices increase.

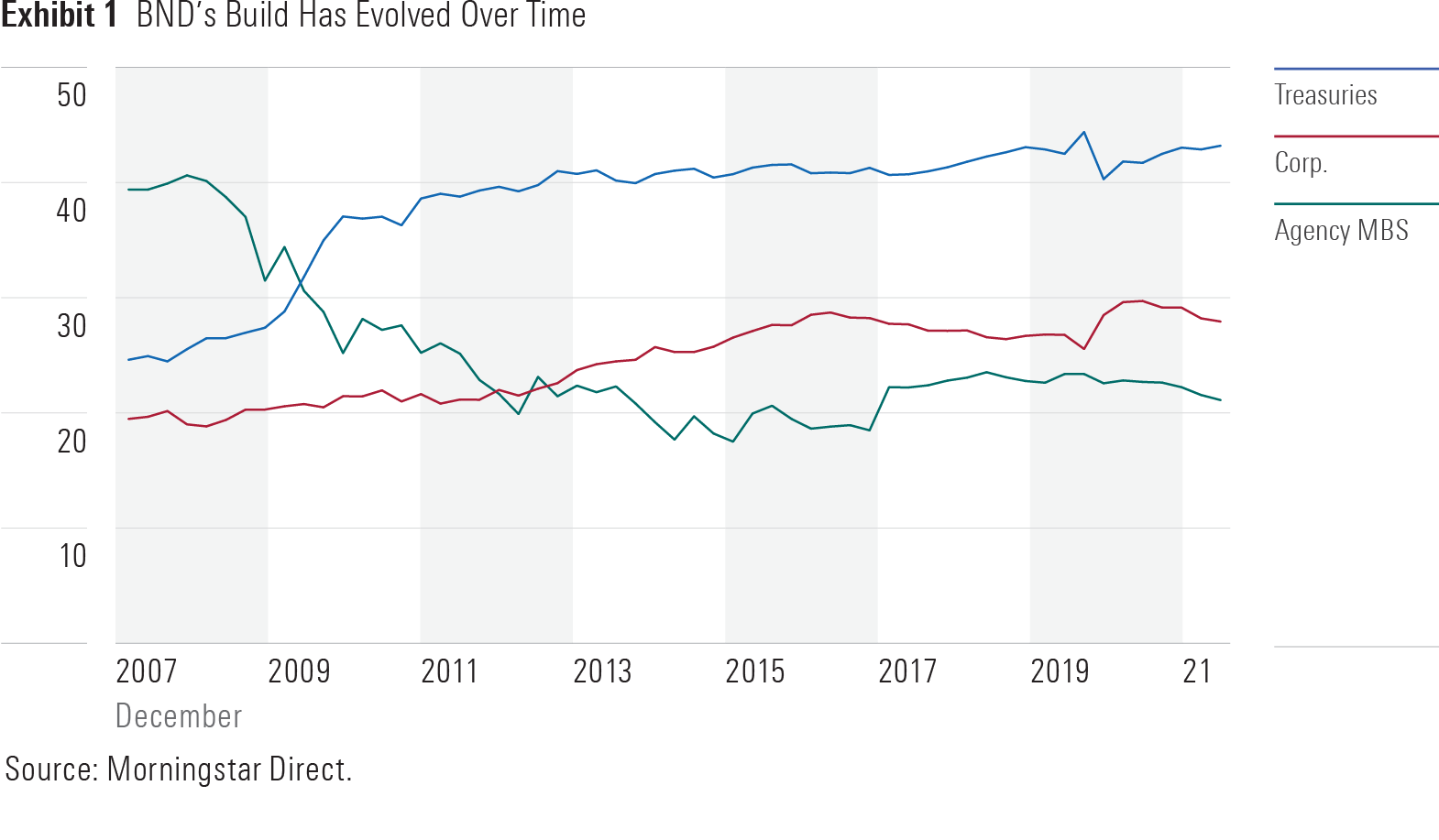

It isn’t difficult to find evidence of this at work in the bond market. Going back to 2009, mortgage-backed securities were the largest segment of the Aggregate Index, representing about 40% of that broad benchmark. But their weight started declining when the housing crisis plunged the global economy into a recession.

Many mortgage bonds declined in value between 2007 and 2009, while fewer were issued in the ensuing years as the global economy slowly came back to life. From 2009 through 2014, BND’s allocation to MBS was cut in half. Ultrasafe U.S. Treasury bonds, with their near-zero default risk, filled most of the void.

Fast forward to February 2022, and Treasuries remain the largest bonds with the biggest weights in BND. Exhibit 1 shows that their position has grown so much that they now represent almost half of BND’s portfolio. U.S. Treasuries are among the safest financial assets on the planet. Assigning such a heavy allocation to them should only help BND function as a risk-reducing agent in a diversified portfolio.

Cons

The advantage of that risk control mechanism has its limits because a trade-off exists between risk and reward. Bond prices rise as their perceived safety increases, but this pushes their yields lower. While market-value weighting tends to place the greatest weight on the safest bonds, it also emphasizes those with the lowest yields and the lowest expected returns.

The fallout of the global financial crisis further illustrates this point. The Federal Reserve tried to stimulate economic growth by cutting short-term interest rates to nearly zero. Other governments around the world followed suit. Some went a step further, with central banks in Europe and Japan introducing negative short-term rates.

The result was lower yields across the yield curve in most markets. Yields on foreign bonds inched lower than their U.S. counterparts. Like BND, ETFs tracking broad market-value-weighted foreign bond indexes shifted toward the lowest-yielding and safest sovereign bonds in their markets, and the effects are still visible today. As of February 2022, The Bloomberg Global Aggregate ex USD Float-Adjusted Index (tracked by Silver-rated Vanguard Total International Bond ETF BNDX) had roughly 80% of its portfolio in government or government-related bonds from major foreign markets like Europe and Japan. Its yield to maturity was about 40 basis points lower than BND’s.

Yields aside, market-value-weighted portfolios have another less-desirable trait. Their composition is shaped by the issuing activity of the U.S. government and major corporations, whose bonds make up the bulk of investment-grade indexes like the Aggregate Index.

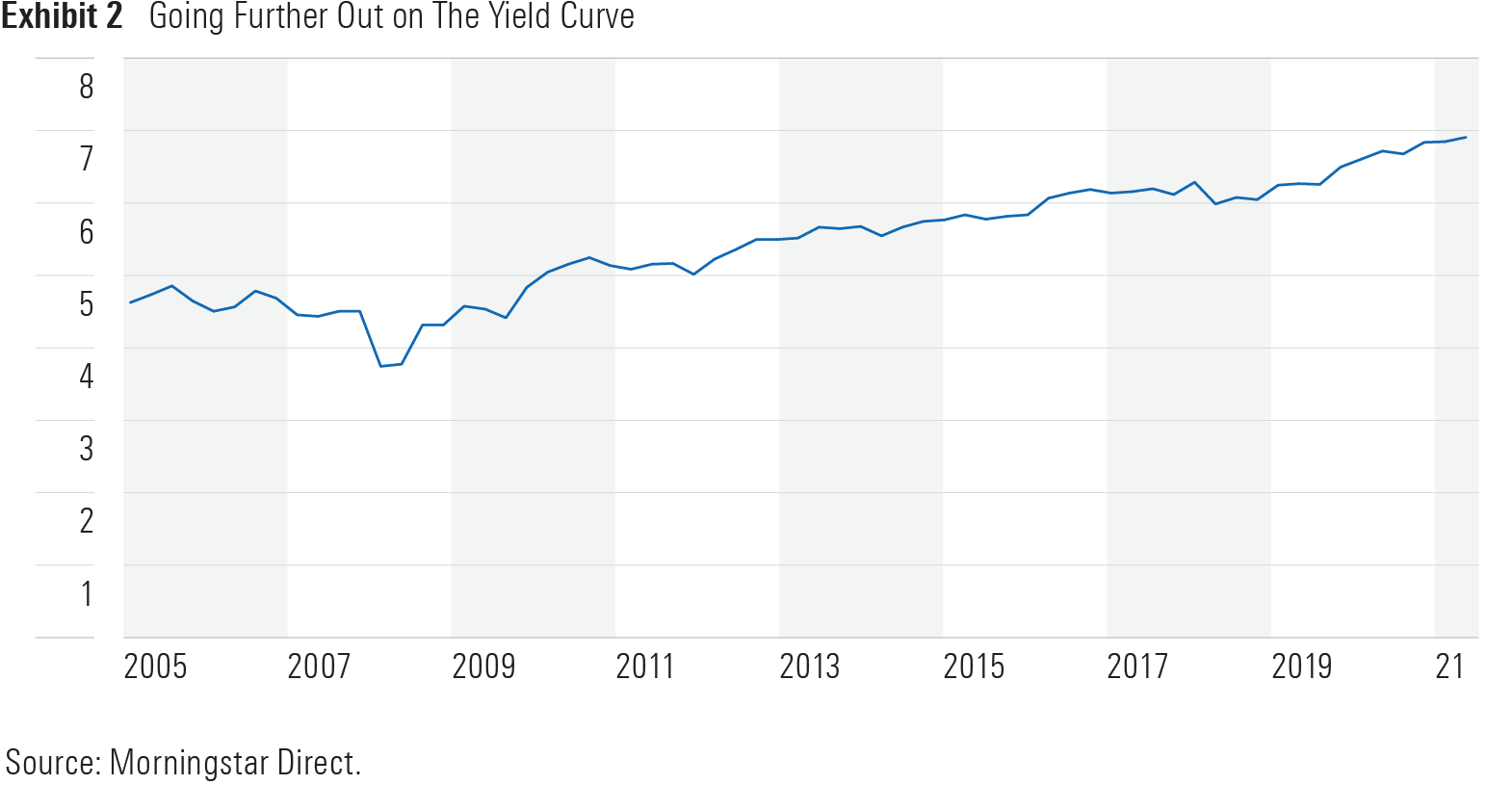

Starting around 2010, the U.S. Treasury and many U.S. corporations started to shift toward bonds with longer maturities. BND’s average maturity increased over the subsequent 12 years. Prior to 2008, BND’s average effective maturity (the average amount of time until the bonds in its portfolio matured) was fairly steady at around 7.0-7.5 years. That extended to almost 9.0 years by the end of 2021.

Longer maturities are important because they have an impact on bond durations, or the sensitivity of bond prices to interest-rate changes. All else equal, increasing a bond’s maturity will increase its duration, meaning its price will decline by a larger amount when interest rates increase and rise more when interest rates fall. Exhibit 2 shows that longer maturities have translated into longer durations for BND.

The Alternatives Aren’t Much Better

Other indexed approaches attempt to offer higher yields with comparable risk. For example, Neutral-rated WisdomTree Yield Enhanced U.S. Aggregate Bond ETF AGGY tracks the Bloomberg U.S. Aggregate Enhanced Yield Index—a benchmark that tries to provide a higher yield than the Aggregate Index. It uses an optimizer to assign bigger weights to bonds with higher yields while honoring constraints that keep the portfolio’s risk profile close to its parent index's.

One of these constraints is a tracking-error requirement that turns out to be both a blessing and a curse. It gives AGGY the freedom to be overweight in higher-yielding bonds without straying too far from the parent universe. The portfolio usually has a modest tilt toward bonds with longer maturities and those with a little more credit risk. As of Dec. 31, 2021, its yield to maturity was about 40 basis points higher than BND’s. The portfolio had roughly 13% more of its assets in BBB rated bonds, while its average effective duration was about nine months longer.

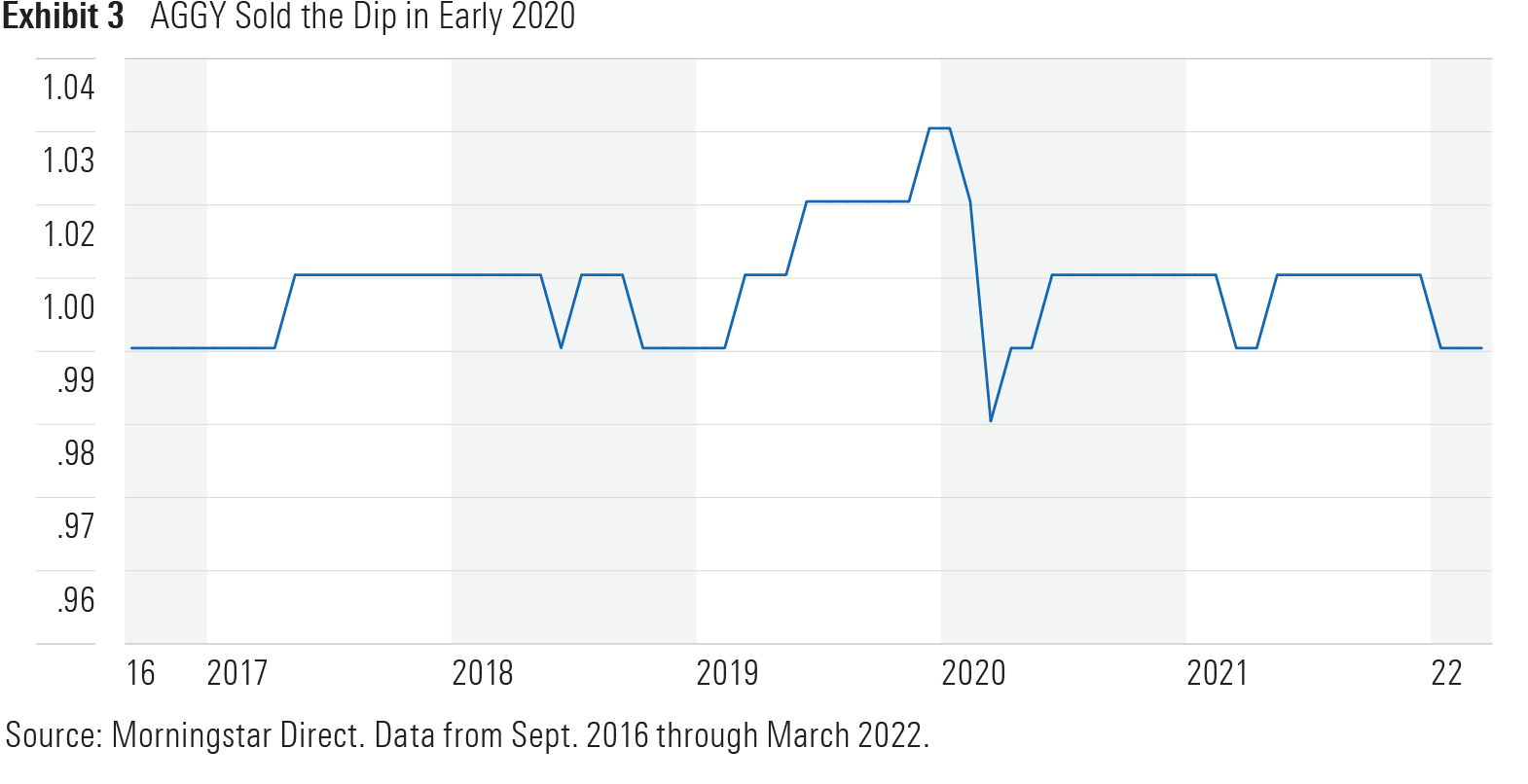

However, that tracking error requirement has undermined AGGY’s performance. During the coronavirus-driven selloff in early 2020, poor performance from the lower-credit-quality bonds that it had overweighted pushed its tracking error outside of its prescribed limits. At its March 2020 rebalance, the optimizer tried to bring tracking error back inside its threshold. It sold some of its fare that had recently gotten pummeled for safer, more-stable bonds that had held up better.

The net result was that AGGY sold low and bought high. Exhibit 3 shows the relative performance of AGGY versus BND. An upward-sloping line indicates AGGY outperformed BND, while a downward-sloping line means the opposite. AGGY lost 3.1 percentage points more than BND in March 2020. But its move toward safer bonds at the end of the month—after they had appreciated in price—left it poorly positioned to benefit from the rebound. Two years later, it has not fully regained the ground it lost to BND after emerging from this episode.

Discretionary active managers have also had a difficult time trying to outperform ETFs like BND. Morningstar has recently reshuffled its intermediate core bond category. Most funds that have historically attempted to boost their performance by holding higher-yielding bonds were split off into the intermediate core-plus bond category. Those remaining mimic the contours of the category benchmark, the Aggregate Index, and the funds that track it, like BND. These funds’ long-term success rate versus their indexed peers has not been great. Morningstar’s year-end 2021 U.S. Active/Passive Barometer showed that just 17% of discretionary active funds in the intermediate core bond category survived and outperformed their average index fund counterpart over the 15 years through December 2021.[1] Over the same period, The Admiral share class of BND was slightly less risky than the average of its category peers. It turned in a slightly lower standard deviation and a shallower average drawdown.

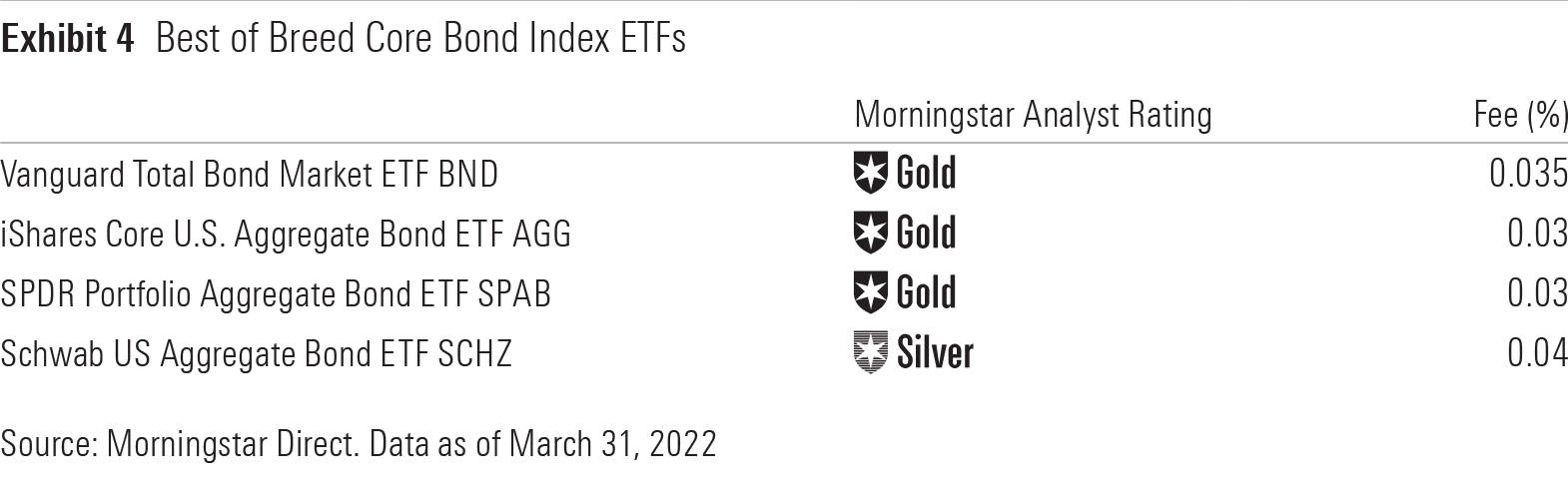

Broad market-value-weighted bond indexes are far from perfect. They tend to focus on the lowest-yielding bonds, and their sensitivity to interest rates has increased over the past 13 years. But they have clearly delivered for investors. ETFs like BND, and similar low-cost ETFs highlighted in Exhibit 4, have proved difficult to beat over the long run. Their big stakes in ultrasafe Treasuries mean they should continue to serve as ballast when markets get choppy.

[1] Johnson, B., & Boyadzhiev, D. 2022. "Morningstar's U.S. Active/Passive Barometer." Morningstar. https://www.morningstar.com/lp/active-passive-barometer.

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Morningstar, Inc. does not market, sell, or make any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/G3DCA6SF2FAR5PKHPEXOIB6CWQ.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/6ZMXY4RCRNEADPDWYQVTTWALWM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/78665e5a-2da4-4dff-bdfd-3d8248d5ae4d.jpg)