Tactical-Allocation Funds: Even Worse Than Expected

They were never going to be good ... but this bad?

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

Fool Me Once Tactical-allocation funds--investments that readily adjust their asset mixes in response to current market conditions--are a sucker's play.

Such funds garner assets after a stock market crash, preying on investors' desires to win the previous war. That war fails to arrive; tactical-allocation funds lag the rising markets; their shareholders become disillusioned and exit the funds. A few years later, that next stock market crash does arrive. The tactical-allocation funds then become paper tigers, showing strong relative performance but offering little benefit to investors given their small size.

I watched that process occur in the late '80s and early '90s, after the October 1987 collapse, so I was under no illusion when tactical-allocation funds returned to popularity in 2009. Give the portfolio managers their freedom, check. Untie them from the tyranny of benchmarks, check. Let active managers truly be active, check. All the appropriate boxes were ticked. The category was poised to fail.

Foolish Consistency

And fail the category has, most spectacularly. Earlier this month, in

, guest author Luke Delorme

the category’s trailing five-year returns. The results were breathtakingly bad. Among the 57 tactical-allocation funds, "not a single one of them outperformed the simple, low-cost, passive fund" of

Shrinking the analysis to three years makes no difference to the result; every tactical-allocation fund trailed. Increasing the analysis to a decade, ditto. The same holds true for 15 years. You name the time period, tactical-allocation funds missed the boat. True, Delorme did find that two of the funds were better than Vanguard’s passive offering if measured on risk/return (rather than return alone) over the 10-year period. But none were better over three years, or five years, or 15 years.

Another View Two questions arise. One: Is the problem unique to tactical-allocation funds? Perhaps other flavors of allocation funds have been similarly poor, in which case the criticism should be expanded. Two: Is the comparison to Vanguard Balanced Index fair? That fund may be rather different in construction than the typical tactical-allocation fund.

The answer to the first question: Yes, the problem is unique.

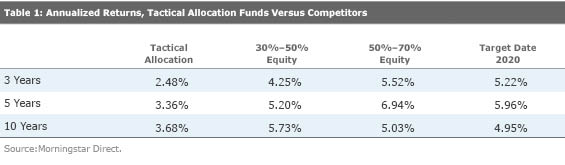

To be sure, Vanguard Balanced has been a resounding success by any standard of allocation fund. Within the allocation--50% to 70% equity Morningstar Category (an awkward label, but certainly descriptive), the Vanguard fund has easily beaten the group averages. What’s more, while Vanguard Balanced does trail several of its own category’s funds over all time periods--typical of passive offerings, which tend to be reliably good rather than number-one winners--it has trounced all funds in the target-date 2020 category. As with the tactical-allocation group, all target-date 2020 funds have lagged Vanguard Balanced over the three-, five-, 10-, and 15-year periods.

So, why pick only on tactical-allocation funds? Because they get punked on another measure: category-average returns. Yes, target-date 2020 and tactical-allocation funds both flopped when chasing Vanguard Balanced. But that joint failure does not make the two categories equal. The target-date group has many decent funds and none that are awful. For example, the target-date 2020 fund with the lowest five-year return registers 2.8%. Nineteen--19!--tactical-allocation funds fall short of that mark, including six funds that placed in the red.

In other words, there are no truly good tactical-allocation funds, but there are plenty that are terrible.

The chart below shows the total-return averages for tactical-allocation funds and target-date 2020 funds, as well as the performance gap between the two categories. For context, the chart also contains the figures for the aforementioned group of allocation--50% to 70% equity funds and the more conservative allocation--30% to 50% equity funds. Across the board, it’s a whipping.

Possible Defenses

Which brings us to the second question: Is it reasonable to compare tactical-allocation funds to Vanguard Balanced--or to these other categories? Or is the comparison somehow rigged?

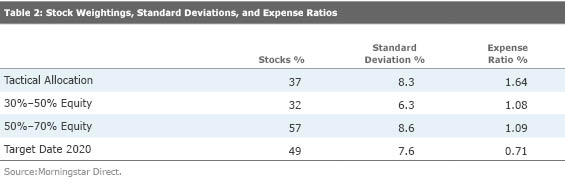

Initially, that concern looks to be valid. Vanguard Balanced consistently holds 60% of its assets in stocks, while the average tactical-allocation fund is currently at 37%. Of course, the category that owns more equities will look better when stocks rally! Any dummy knows that.

Unfortunately, as shown in the chart below, the tactical-allocation category’s troubles run deeper than merely holding a conservative asset mix. The allocation--30% to 50% equity Morningstar Category invests even less in stocks than do tactical-allocation funds but has significantly higher returns. It also is considerably less volatile, as illustrated by an average annualized standard deviation of 6.3% (calculated over the trailing five years), as opposed to 8.3% for tactical-allocation funds.

There’s also the problem that, despite its much-higher stock weighting, Vanguard Balanced also posted a lower standard deviation than did the average tactical-allocation fund. That’s not very reassuring, given that the group’s primary appeal is risk reduction and that its primary defense is that it is positioned too conservatively to participate fully in a stock bull market.

Besides, how can tactical-allocation funds credibly dispute the comparison to other versions of allocation funds? They assert the ability to anticipate the future. They seek to know when to own more stocks, when to own less. There should be no such thing as an unreasonable comparison--or an unfavorable market--for tactical-allocation funds. They are highly paid for their claims. Their average expense ratio is 50% higher than those of the two strategic-allocation categories and more than double the target-date average.

Tactical-allocation funds embody the worst of active fund management. They come to the marketplace during times of weakness, promise what they cannot deliver, and charge a small fortune. Even when their expenses are added back to their results so that they are judged on gross returns--returns that no investor can ever achieve--they trail all feasible competitors. There is no measure by which tactical-allocation funds can be defended. They are indefensible.

John Rekenthaler has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar's investment research department. John is quick to point out that while Morningstar typically agrees with the views of the Rekenthaler Report, his views are his own.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

/d10o6nnig0wrdw.cloudfront.net/04-25-2024/t_d30270f760794625a1e74b94c0d352af_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/DOXM5RLEKJHX5B6OIEWSUMX6X4.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZKOY2ZAHLJVJJMCLXHIVFME56M.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)