Experts Forecast Stock and Bond Returns: 2023 Edition

Thanks to higher yields and lower equity valuations, return assumptions are the highest they’ve been in years.

/s3.amazonaws.com/arc-authors/morningstar/66112c3a-1edc-4f2a-ad8e-317f22d64dd3.jpg)

This past year was a dispiriting one for investors, with stocks and bonds declining simultaneously along with the increase in interest rates.

Yet, even as investor balances are depressed, their portfolio prospects are likely better than they were a year ago, a fact that my latest roundup of capital markets assumptions illustrates vividly. Thanks to higher fixed-income yields and lower equity valuations, almost all of the firms in our survey have increased their expectations for stock and bond returns for the next decade. Every firm in our survey expects non-U.S. stocks to outperform U.S. stocks in the decade ahead.

Sane investors might pooh-pooh market-return forecasts of any kind, pointing to forecasters’ poor track records of predicting the market’s direction on a short-term basis. But long-term return projections can be useful and are arguably even mission-critical in a financial planning context. Without some expectation of what market returns might be, it’s difficult to know how much to save, whether a retirement nest egg is adequate, or if an in-retirement spending rate is too high. Long-term historical returns might fill that role, but at various points in time, such as early 2000 or early 2022, they might be unrealistically high.

That’s why I have been gathering firms’ capital markets assumptions annually, and occasionally even more frequently than that when the market has experienced a downdraft. As in the past, I’ve sampled return outlooks from a host of firms to identify commonalities and points of difference. Investment firms use different methodologies to arrive at their capital markets assumptions, but most employ some combination of current dividend yields, valuation, and earnings-growth expectations to guide their equity forecasts. Fixed-income return assumptions are more straightforward given the tight historical correlation between starting yields and returns over the next decade.

How to Use Them

Before you take these or any other return forecasts and run with them, it’s important to bear in mind that these return estimates are more intermediate-term than they are long-term. The firms I’ve included below all prepare capital markets forecasts for the next seven to 10 years, not the next 30. (BlackRock does provide a 30-year forecast, and Fidelity’s capital markets assumptions apply to a 20-year horizon, but they’re outliers in terms of making such far-reaching forecasts available to the public.) As such, these forecasts will have the most relevance for investors whose time horizons are in that ballpark, or for new retirees who face sequence-of-return risk in the next decade.

It’s also important to note that the parameters for these return estimates vary a bit; some of the return expectations are inflation-adjusted, while most are not. In addition, some of the experts forecast returns for the next decade, while others employ slightly shorter time horizons.

Finally, it’s worth noting that several of the capital markets assumptions included here date from the end of the third quarter of 2022, when bond yields were peaking and stock and bond prices were exceptionally beaten down. Both asset classes have recovered a decent amount since that time, so it stands to reason that many of the forecasts discussed below may have declined accordingly.

BlackRock

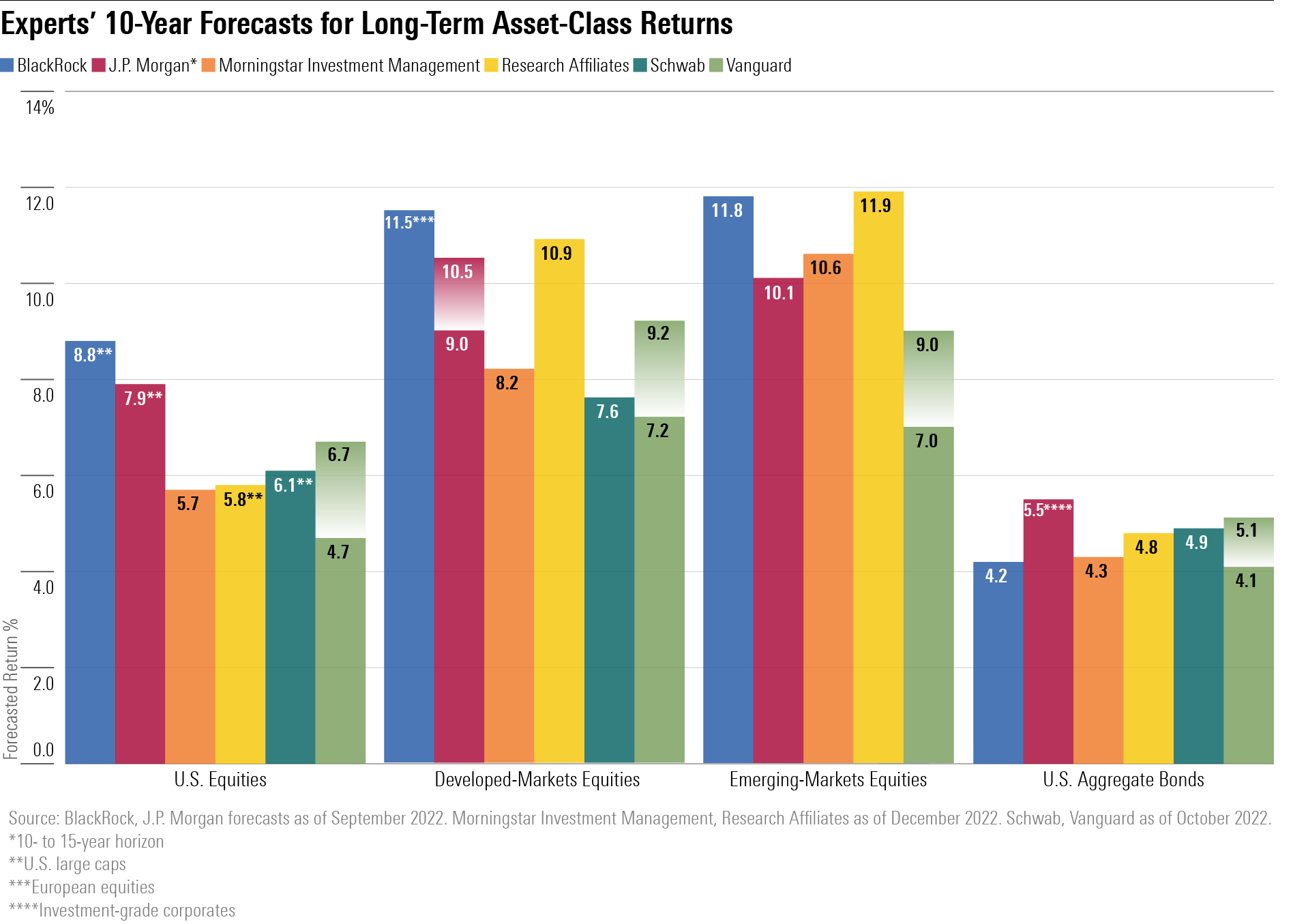

Highlights: 8.8% 10-year expected nominal return from U.S. large-cap equities; 11.5% from European equities; 11.8% from emerging-markets large-cap equities; 4.2% for U.S. aggregate bonds (September 2022). All return assumptions are nominal (non-inflation-adjusted).

BlackRock’s asset-class return expectations in September 2022 were notably higher than was the case the year prior. For example, the firm was expecting a 7% 10-year return for U.S. large caps in September 2021 but a nearly 9% return as of September 2022. Reflecting the prospect of higher interest rates, the firm’s expectation for U.S. aggregate bond returns was also much higher—a 4.2% expected 10-year return as of September 2022 versus less than 2% in 2021.

Like every firm in our survey, BlackRock continues to be even more sanguine in its outlook for international stocks, assuming nominal 10-year returns of nearly 12% for emerging-markets and European equities over the next decade. (The return assumption for Chinese equities was particularly high—nearly 15%.) BlackRock’s return assumptions for private equity were also quite high, at 11%, but that’s substantially lower than its 19% 10-year private equity return assumption in September 2021.

Fidelity

Fidelity’s capital markets assumptions employ a 20-year horizon (2022-42) and therefore can’t be stacked up neatly against the 10-year returns from other firms in our survey. In addition, the firm states its capital markets assumptions in real (inflation-adjusted) terms; its base-case inflation rate over the 20-year horizon is 2.5%. Finally, the firm’s assumptions are based on data as of April 2022, so they don’t factor in the equity price declines and higher bond yields that came to pass later last year.

The firm is forecasting a 3.0% real return for U.S. equities over the next 20 years, less than half their 6.6% average return from 2001-21. Fidelity cites elevated equity valuations (again, as of April 2022) and reduced earnings potential as constraints on U.S. equity gains. On the fixed-income side, the firm was forecasting 1.9% 20-year real returns for the Bloomberg U.S. Aggregate Bond Index as of April 2022. Like all of the firms in our survey, Fidelity’s research accords a higher return assumption for non-U.S. equities for the next two decades: 3.3% real returns for developed non-U.S. equities and 5.1% for emerging-markets stocks.

Grantham Mayo Van Otterloo

Highlights: Negative 0.7% real (inflation-adjusted) returns for U.S. large caps over the next seven years; 0.6% real returns for U.S. bonds; 5.6% real returns for emerging-markets equities; 4.1% real returns for emerging-markets debt (Dec. 31, 2022).

GMO’s asset-return expectations have historically been the most pessimistic in our roundup, and despite improving valuations and higher fixed-income yields, the firm’s year-end 2022 forecast for the next seven years was no exception. That said, the firm’s expectations took a positive turn during the year. GMO expects U.S. large caps to deliver a real (inflation-adjusted) loss of 0.7% over the next seven years, a big increase from the nearly 7% real loss the firm was forecasting a year ago. And the firm’s seven-year expected return from U.S. bonds popped into positive territory as of year-end 2022, in contrast with the 4% real loss the firm anticipated at the end of 2021.

In keeping with previous forecasts, the firm still expects emerging markets to shine. Its seven-year real return forecast for the broad category of emerging-markets equities is 5.6%, and it’s 9.8% for the subset of emerging-markets value stocks.

J.P. Morgan

Highlights: 7.9% nominal returns for U.S. large-cap equities over a 10- to 15-year horizon; 4.0% nominal returns for 10-year Treasury bonds and 5.5% nominal returns for U.S. investment-grade corporate bonds over a 10- to 15-year holding period (Sept. 30, 2022).

“Lower valuations and higher yields mean that markets today offer the best potential long-term returns since 2010,” wrote the co-authors of J.P. Morgan’s 2023 Long-Term Capital Markets Assumptions report. Indeed, J.P. Morgan’s 2023 capital markets assumptions for the major asset classes are significantly higher than was the case a year ago. The firm’s 10- to 15-year forecast for U.S. large-cap equities is nearly double the forecast in 2022—7.9% versus 4.1%. J.P. Morgan ascribes the difference to lower valuations. The outlook for developed-markets equities was higher still: 10.5% for European equities, 10.4% for Japanese equities, and 9.1% for U.K. equities. The firm’s return expectation for emerging-markets equities was equally optimistic—10.1% versus 6.9% in the 2022.

On the fixed-income side, the firm has nudged up return expectations thanks largely to higher yields on offer today: It’s expecting a 5.5% nominal return from U.S. investment-grade corporates, substantially better than its 2.8% return forecast in 2022. J.P. Morgan’s return expectation for U.S. high-yield bonds is higher, too—6.8% versus 3.9% last year. The firm is also enthusiastic about the prospects for emerging-markets debt, forecasting a return of 7.1% versus 5.2% in 2022.

Morningstar Investment Management

Highlights: 5.7% 10-year nominal returns for U.S. stocks; 4.3% 10-year nominal returns for U.S. aggregate bonds (Dec. 31, 2022; data forthcoming in the Morningstar Markets Observer).

As usual, the Morningstar Investment Management team’s forecast for U.S. equities leans toward the pessimistic side of our collected forecasts, especially for equities. However, it’s substantially better than was the case in 2022: a 5.7% nominal 10-year return assumption for U.S. large caps for the next decade, versus 2.6% at this time last year. MIM’s outlook for non-U.S. stocks is a bit sunnier: an 8.2% return (nominally) for developed-markets equities and 10.6% for emerging-markets equities.

Like most of the forecasts, MIM’s return expectations for bonds have jumped up to reflect higher yields. It assumes a 4.3% 10-year nominal return for U.S. aggregate bonds and 6.2% for U.S. high yield. A year ago, the 10-year projected return for both asset classes was less than 2%.

Research Affiliates

Highlights: 5.8% nominal (2.3% real) returns for U.S. large caps during the next 10 years; 4.8% nominal (1.2% real) returns for aggregate U.S. bonds (Dec. 31, 2022; valuation-dependent model).

Research Affiliates’ return expectations for the major asset classes have increased substantially over the past year. It was forecasting a small negative real return for U.S. stocks and bonds a year ago, whereas those return projections are now comfortably in the black and look even better on a nominal basis. In keeping with past forecasts, the firm is more sanguine still in its outlook for non-U.S. stocks. It’s forecasting a 10.9% nominal return (7.3% real) for developed-markets equities over the next decade and an 11.9% nominal gain (8.3% real) for emerging-markets stocks.

Schwab

Highlights: 6.1% nominal returns for U.S. large caps during the next 10 years; 4.9% nominal returns for U.S. aggregate bonds (Oct. 31, 2022).

Schwab is a new addition in this year’s compilation of capital markets assumptions, though it has been compiling these return projections for several years. In 2023′s forecast, the firm’s 10-year annualized return expectation for U.S. stocks is 6.1%, and 7.6% for international large-cap equities. Schwab’s researchers note that those figures are roughly in line with the 2022 return projections: While valuations are indeed more attractive, they believe that company-level and macroeconomic headwinds could put a damper on gains.

In line with the outlook from other investment providers, the firm is forecasting a 4.9% gain for U.S. aggregate bonds, versus 2.3% a year ago. (All figures are nominal.) Schwab notes, however, that its 10-year return expectations are well below each asset class’ returns from 1970 through October 2022.

Vanguard

Highlights: Nominal median U.S. equity market return of 4.7%-6.7% during the next decade; 7.2%-9.2% median expected returns for non-U.S. equities; 4.1%-5.1% median expected return for U.S. fixed income (Oct. 31, 2022).

Vanguard’s recently published return expectations were substantially higher at the end of October 2022 than was the case a year prior. On the equity side, the firm’s researchers note that its 10-year global equity return assumption is now 2.25 percentage points higher than in late 2021, whereas its bond-return expectations are roughly 2.5 percentage points higher than was the case a year earlier. The firm produces its return expectations in a range rather than providing a precise estimate for each asset class.

As at other firms, the headline continues to be that Vanguard expects better performance from non-U.S. equities than U.S. equities over the next decade. Vanguard is also expecting smaller stocks to outperform large, but no longer believes that value stocks to have an edge over growth. “Within the U.S. market, value stocks are fairly valued relative to growth, and small-capitalization stocks are attractive despite our expectations for weaker near-term growth,” the firm’s researchers wrote.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/6ZMXY4RCRNEADPDWYQVTTWALWM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/URSWZ2VN4JCXXALUUYEFYMOBIE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/CGEMAKSOGVCKBCSH32YM7X5FWI.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/66112c3a-1edc-4f2a-ad8e-317f22d64dd3.jpg)