The Inflation Hedges Haven't Hedged

When inflation arrived, they slept.

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

The Imperfect Storm

On May 12, 2021, inflation struck the United States. That morning, the Bureau of Labor Statistics announced that the nation's core inflation rate--derived by stripping out food and energy costs from the Consumer Price Index--had risen by 0.9% in April, the largest such increase in 39 years. Although core inflation has since declined, the rate remains well above its previous level.

The surge was unanticipated. When 37 economists were surveyed in November 2020, their prediction for the 2021 core inflation rate was 1.8%. In addition to providing the median estimate, the forecasters were also asked whether 2021 core inflation would exceed 4%. They estimated that possibility as zero. Not less than one chance in 100. Not less than one chance in 1,000. Not even one chance in 10,000. Zero. (The actual amount was 5.9%.)

The conditions were ideal for inflation hedges, not only because prices surged, but also because they did so suddenly. Investment hedges don’t necessarily protect against widely predicted troubles, as those events may already be reflected in the securities’ prices. But they should certainly defend against surprises. A hedge that doesn’t shield against abrupt shocks is a failed hedge.

Four Candidates

And this, unfortunately, is largely what investors have owned: failed hedges.

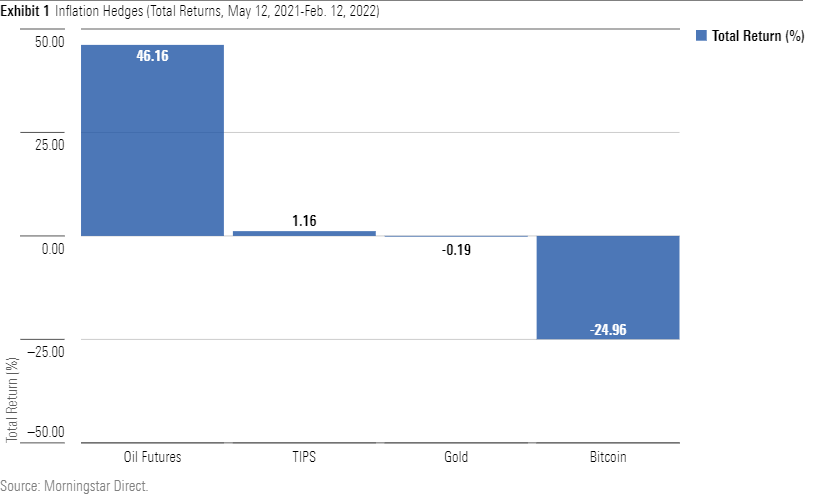

- Gold. The traditional inflation hedge, of course, is gold, a commodity with more than 5,000 years of price history. Since the Bureau of Labor Statistics released its announcement, gold bullion has dogpaddled. Nobody looking at a gold price chart would be able to tell when inflation resurfaced.

- Treasury-Inflation Protected Securities. Along with gold, TIPS are the most logical inflation hedge. After all, they were created by the U.S. government for exactly that purpose. As with gold, TIPS have gone nowhere. From May 12 until now, they have gained barely more than 1%. So far this year, relates Morningstar's Tom Lauricella, their performance has been worse yet, with TIPS chalking up losses.

- Cryptocurrencies. Cryptocurrencies are commonly regarded as electronic inflation hedges. That makes sense. Historically, gold has appreciated when fiat currencies have stumbled. So, why would the modern equivalents of gold behave differently? But behave differently they have. Unlike gold, cryptocurrencies haven't broken even since the Bureau's announcement. They have lost money, badly. (Bitcoin's main rivals of Ethereum and Binance Coin have performed somewhat better, but they have also been in the red since mid-May.)

- Energy. Energy long ago lost its investment allure. Not only has oil badly trailed other assets since its 1980 peak, it also hasn't protected well against stock-market declines. Crude oil fell during the 2000-02 technology-stock downturn, lost two thirds of its value through the 2008 global financial crisis, and briefly turned negative amidst the pandemic. Recently, though, oil prices have surged, making energy the sole winner among the four potential inflation hedges.

Assessing the Results

The following chart depicts the returns since the week of the Bureau’s announcement for the largest investable version of each of the inflation hedges: 1) SPDR Gold Shares GLD, 2) Vanguard Inflation-Protected Securities VIPSX, 3) Grayscale Bitcoin Trust GBTC, and 4) United States Oil Fund LP USO.

An unimpressive showing. Among the group, only energy has flourished, and it’s doubtful given the lack of investor interest whether it even belongs on a list of inflation hedges. For example, United States Oil has attracted only $2.6 billion in shareholder monies, as opposed to $27 billion for Grayscale Bitcoin Trust, $41 billion for Vanguard’s TIPS fund, and $60 billion for SPDR Gold Shares. Oil prices respond almost entirely to industrial demand rather than to investors’ inflation expectations.

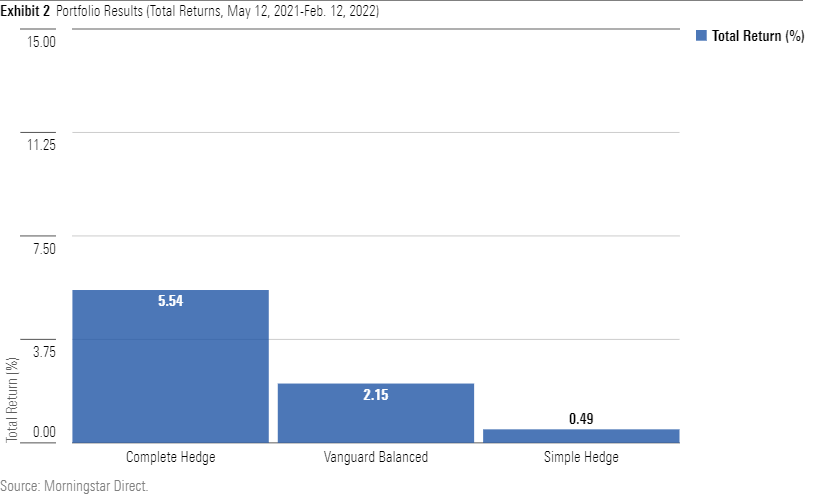

The next chart compares the returns for two blends of the inflation hedges against that of a conventional unhedged fund, Vanguard Balanced Index VBAIX. The Simple Hedge consists solely of gold and TIPS, while the Complete Hedge contains all four investments. The hedges are equally weighted and have not been rebalanced. (No need to overcomplicate an exercise conducted on the virtual back of an envelope.)

The Complete Hedge fared reasonably well. However, this hedge benefits massively from hindsight, because entering spring 2021 even investors who were deeply concerned about inflation were unlikely to have owned energy. The Simple Hedge is therefore a more realistic estimate of how inflation-wary securities performed. The answer, it turned out, was “much like securities that made no explicit attempt to safeguard against inflation.”

What’s Going on Here?

The problem doesn’t lie with the assets. Cryptocurrencies may prove to be illusory, and while oil prices advanced during this inflationary bout, they might well sink during the next one should industrial demand be slack. But the Simple Hedge should have thrived. Gold’s inflation-fighting powers have been amply demonstrated over many centuries. And TIPS were explicitly designed to combat rising inflation.

The reason for the uninspiring performance of the inflation hedges thus lies elsewhere, outside the investments themselves. One possible explanation is that current inflation is a mirage. Not to say, of course, that the Bureau of Labor Statistics cooked the numbers (government bodies are not in the habit of spoiling their own reports), but instead that the increase is only temporary. When the global supply chain becomes unstuck, inflation will diminish.

Another interpretation is that although inflation’s arrival caught market forecasters unawares, it did not surprise investors. They did not know when inflation would surface, any more than did the forecasters, but they knew that sooner or later, the bad news would arrive. Consequently, they had already bid up the prices of inflation hedges. Thus, when inflation did appear, gold and TIPS failed to react, because their values already anticipated the event.

The evidence supports both answers. The bond market has treated, and continues to treat, today's inflation as a mirage. The yield on 30-year Treasuries has declined since May 12, 2021. (Yes, it has.) The public may regard inflation as a headache, but not bond investors. They see no need to hedge against inflation that will not persist. Also, it appears that inflation hedges have been aggressively valued. From 2018 through summer 2020, gold prices rose by more than 50%, while the real yield on TIPS shrunk to negative 1% from 1%.

The upshot: Inflation hedges disappointed because the financial markets aren’t (yet) convinced that inflation is here to stay, and because the insurance they provide was costly. With hedges, as with other securities, the investment features alone don’t determine returns. The cost of admission also matters.

The other lesson from this episode, at least from me, is the importance of diversifying inflation hedges. This time, oil came out of nowhere to at least partially salvage inflation-hedging strategies. Next time, another asset might come to the rescue. Better to own a Complete Hedge than a simple one.

John Rekenthaler (john.rekenthaler@morningstar.com) has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar's investment research department. John is quick to point out that while Morningstar typically agrees with the views of the Rekenthaler Report, his views are his own.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HKIFRWSPJZGZRNDNXEELOFFMVM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/N7VBPGEKIZDBPEAHLKIWYNRLBE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/JIZ7XPQ4FK7TGXNX42XRYN4GZM.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)