It’s Been Rough for Stocks, but the Outlook Is Still OK

The changing outlook for the Fed continues to spark volatility.

/s3.amazonaws.com/arc-authors/morningstar/ed529c14-e87a-417f-a91c-4cee045d88b4.jpg)

It’s been an especially rough start to the year for the stock market, but as painful as the hit has been to portfolios, that doesn’t mean the outlook is equally as dire.

It’s natural for investors to see a day like Monday’s sell-off--when broad market indexes were down more than 3% before bouncing--as a sign of worse to come. And financial markets often are forward-looking, with prices rising and falling based on expectations for what is to come.

Yet, in this case, it may be more of an overdue reset by an overvalued stock market when it comes to the outlook for interest rates and Federal Reserve policy. Economists expect the economy to continue growing at a healthy pace this year, and that by historical standards, interest rates are expected to remain low for some time, supporting that economic growth.

“While the markets have been brutalized the past few trading sessions, the outlook is not as dire as the market action implies,” says David Sekera, Morningstar’s chief U.S. market strategist

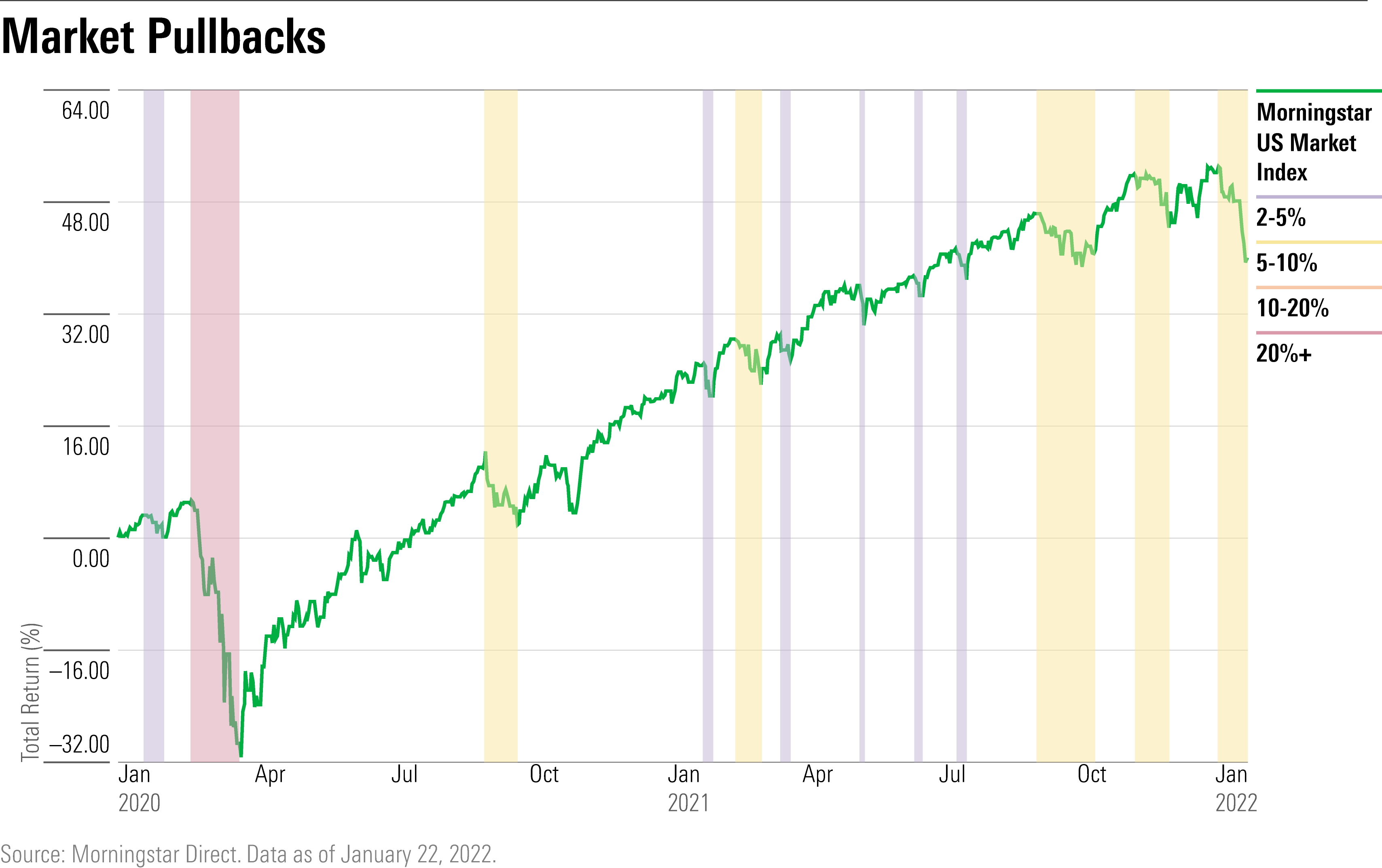

And it has been brutal. The Morningstar U.S. Market index has lost 8% so far in 2022 and at its worst levels Monday was down more than 10% from the most recent peak on Jan. 3--a decline known in market lingo as a “correction.”

Raheel Siddiqui, portfolio and quantitative strategist in Neuberger Berman’s global equity research department, says Monday’s steep declines weren’t driven by fundamental news, but rather a confluence of “technical” factors, such as selling by trend-following futures traders, stock options traders, and ripples from leveraged exchange-traded funds. That coupled with a lack of “buy-the-dip” support from individual investors helped create a void for the market to fall into to start the week. At the same time, there was an overhang of big, institutional investors heavily weighted in the very largest--and often most expensive--stocks who finally started cutting back on those positions.

“A lot of the selling was technical in nature … but obviously the trigger was the Fed,” Siddiqui says.

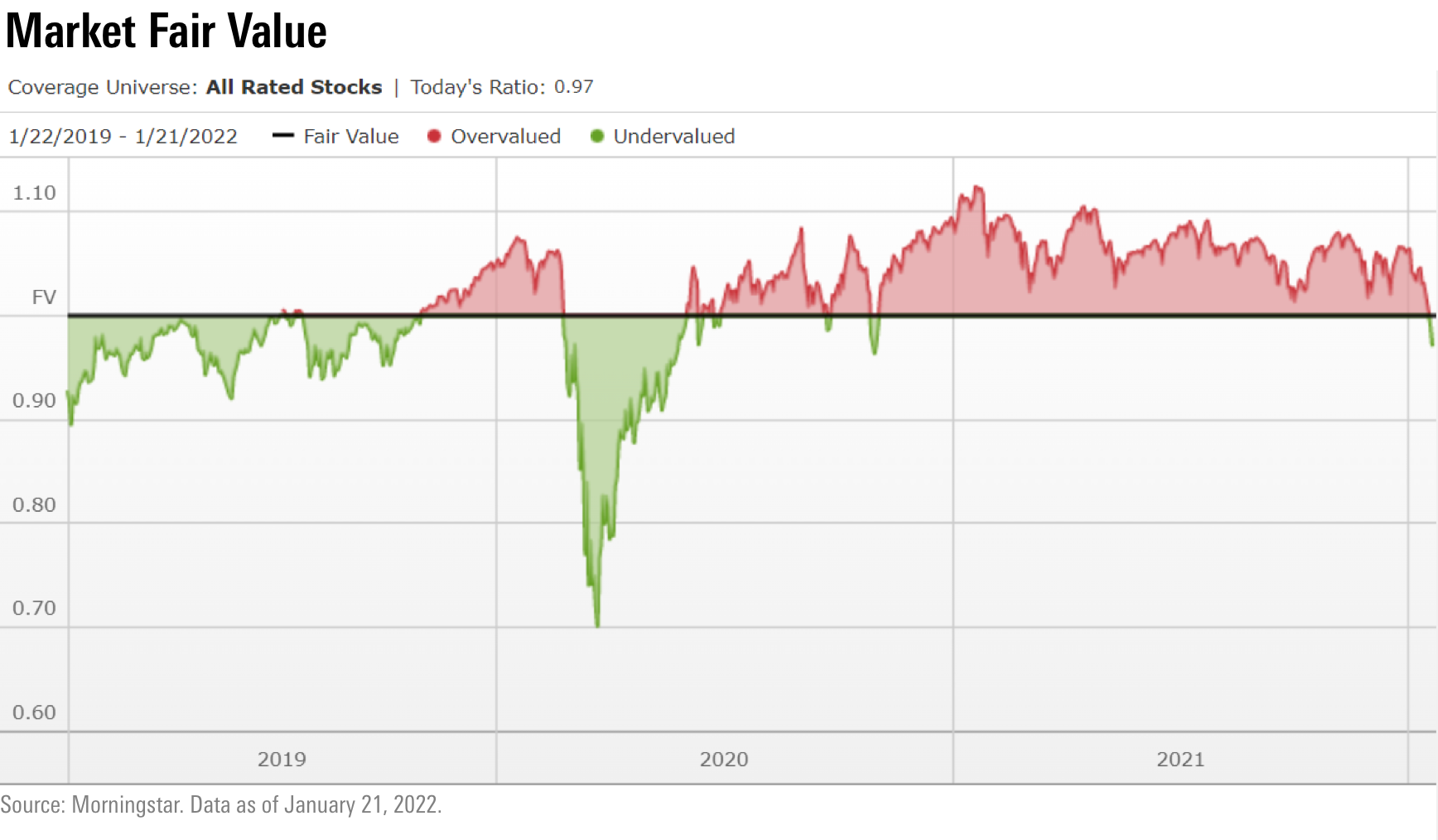

Another challenge for the stock market has been valuations. Based on the universe of stocks covered by Morningstar's analysts, U.S. stocks came into 2022 roughly 5% overvalued.

When it comes to the Fed, another the issue is the Fed’s hard pivot in terms of its support for the economy. The central bank is making a quick switch from a pedal-to-the-metal approach, to keeping the economy rolling during the worst of the coronavirus pandemic recession, to hitting the brakes in response to the flareup in inflation. This Tuesday and Wednesday Fed officials are meeting to decide the next steps for monetary policy.

While a change in posture by the Fed been in the cards for months, the pace at which the outlook for the Fed is evolving has forced investors to adjust their expectations rapidly as well.

As recently as Thanksgiving, the Fed was expected to start raising interest rates in mid-2022 and boost the federal-funds rate just two, maybe three times this year. Now the Fed is expected to lift off its rate increases in March with a total of four increases expected this year.

Not only that, the Fed is expected to start reversing the bond-buying program--known as quantitative easing--that it used to pump money into the economy during the pandemic. That looming switch from quantitative easing to the opposite--known as quantitative tightening--is what some speculate has particularly roiled the market.

Barry Knapp, direct of research at Ironsides Macroeconomics, says the market’s action in January reflects a relatively new dynamic for stocks that began to show up in the wake of the global financial crisis when the Fed first employed QE.

Prior to 2008, stocks would typically have just one big sell-off when the Fed switched into rate-increase mode. But in the world of quantitative easing and tightening, there has been considerably more volatility around Fed policy. From 2010 through 2018, Knapp says, the market had eight Fed-policy related declines, with an average loss of 11%.

Quantitative tightening “is a much bigger deal than the Fed raising rates … and the markets have a big adjustment to that,” he says.

That said, with stocks down roughly 11% from their peak during the worst of Monday’s sell-off, “we’ve followed that pattern,” he says. “I think we’ll find a bottom here.”

It’s important for investors to realize that even with the Fed switching gears, “monetary policy has been so easy and so far from tight, the Fed starting to normalize isn’t a negative” for the economy, Knapp says.

Morningstar’s Sekera notes that Morningstar’s forecast for the U.S. economy in 2022 is still for growth to come in at a healthy 3.9% rate and 3.5% in 2023. “Both these levels of economic growth are still near the highest levels the U.S. has experienced over the past 15 years.”

In addition, “while inflation is running hot and will remain elevated for the next few months, we project it will begin to moderate in the second half of this year and continue to decline toward normalized levels in 2023,” Sekera says.

“Factoring these attributes, at current levels, we now see the market as being broadly fairly valued,” Sekera says.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/6ZMXY4RCRNEADPDWYQVTTWALWM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/URSWZ2VN4JCXXALUUYEFYMOBIE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/CGEMAKSOGVCKBCSH32YM7X5FWI.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ed529c14-e87a-417f-a91c-4cee045d88b4.jpg)