There's More to Sustainability Than Meets the Eye

There is no one-size-fits-all in sustainable investing.

/s3.amazonaws.com/arc-authors/morningstar/0fa19b38-60f6-4a0f-9e06-9869d9c57d52.jpg)

A version of this article previously appeared in the June 2022 issue of

. Click here to download a complimentary copy.

Sustainable investing has exploded in popularity, with the number of sustainable funds in the United States doubling and assets quadrupling over the past three years. Asset managers have launched funds across a spectrum of sustainability aims, from cheap index strategies with basic exclusions to impact funds intended to generate positive and measurable environmental, social, and governance impact.

This wide array of strategies has created confusion for investors and regulators in determining what counts as ESG and where investments fall on the sustainable continuum. Claims of greenwashing—a term coined in the 1980s by environmentalist Jay Westerveld in an essay criticizing the “save the towel” movement in hotels that ultimately just benefited hotels—are commonplace as organizations balance competing in a burgeoning industry with trying to define what counts as ESG.

Two schools of thought have emerged about handling companies with negative ESG practices: divestment or active ownership. Divestment is the most prominent tool used by ESG funds. It runs the gamut from index funds with basic exclusions to impact funds. Active ownership instead leverages a fund’s ownership of a company to advance causes through engagement and proxy-voting activities.

Directing capital away from negative ESG companies in the secondary market may cause the company to rethink its strategy under certain circumstances. However, investors’ ability to directly effect change is forfeited the second they divest. For many investors, the best option is to hang on to their shares and vote.

Most investors, however, surrender their votes to fund managers, as is often the case for active funds, or a group within the broader asset manager that specializes in corporate engagement and proxy voting, which is most common for index funds. This introduces a new vector in choosing funds: Who are you entrusting with your vote?

One Step Forward, One Step Back

Active ownership by asset managers can take different forms. Some of the best examples of investment stewardship came from asset managers that led the movement in ESG exchange-traded funds and generated power from their substantial assets under management.

BlackRock’s Larry Fink publishes an annual letter to the CEOs of BlackRock’s portfolio companies that serves to highlight issues facing the long-term health of corporations. Fink wields BlackRock’s $10 trillion AUM to drive action. In his 2020 letter, Fink raised the alarm on climate change, stating that climate risk is investment risk and BlackRock has a fiduciary duty to place sustainability at the center of their investment approach. As a result, Fink has become one of the faces of the shift to sustainable investing.

In 2021, activist hedge fund Engine No. 1 shocked the corporate world by parlaying a $50 million stake in ExxonMobil XOM into three seats on the energy giant’s board, against the recommendation of Exxon’s own executives. Although its 0.2% stake hardly moved the needle for the vote, it won the hearts of sustainability-focused shareholders by pledging to push Exxon toward renewable energy. BlackRock voted its 6.7% stake in support for the three candidates, while Vanguard (8.7%) and State Street (5.7%) supported two of the confirmed candidates. Engine No. 1 Transform 500 ETF VOTE was launched shortly after the victory.

On International Women’s Day in 2017, State Street introduced Fearless Girl, a powerful statue of a defiant girl positioned in front of the Charging Bull statue in New York. While this coincided with the launch of SPDR SSGA Gender Diversity ETF SHE, it also spurred conversation about gender equality in corporations. According to State Street’s website, the number of companies they identified without a woman on their board of directors fell from 1,548 companies when it launched its Fearless Girl campaign in 2017 to 600 companies as of February 2022.

Each of these examples reflects the power of active ownership to build awareness and enact change. However, as is often the case with sustainable investing, individuals interpret these campaigns differently. And each campaign has come under scrutiny since its launch.

Fear over a few asset managers—or even one man, in the case of Fink—directing substantial corporate ownership has market observers questioning the consolidation of power among BlackRock and other heavyweight asset managers, like Vanguard, State Street, and Fidelity. And Engine No. 1’s opportunity to “Reenergize Exxon” has fallen short of expectations. Early reports on Engine No. 1’s voting in the 2022 proxy season have it siding more often with Big Oil management than driving change. For State Street, the firm paid $5 million to settle claims by the U.S. Department of Labor that it had discriminated against female and Black employees through unfair pay practices just a few months after Fearless Girl went up.

Digging Deeper on Stewardship

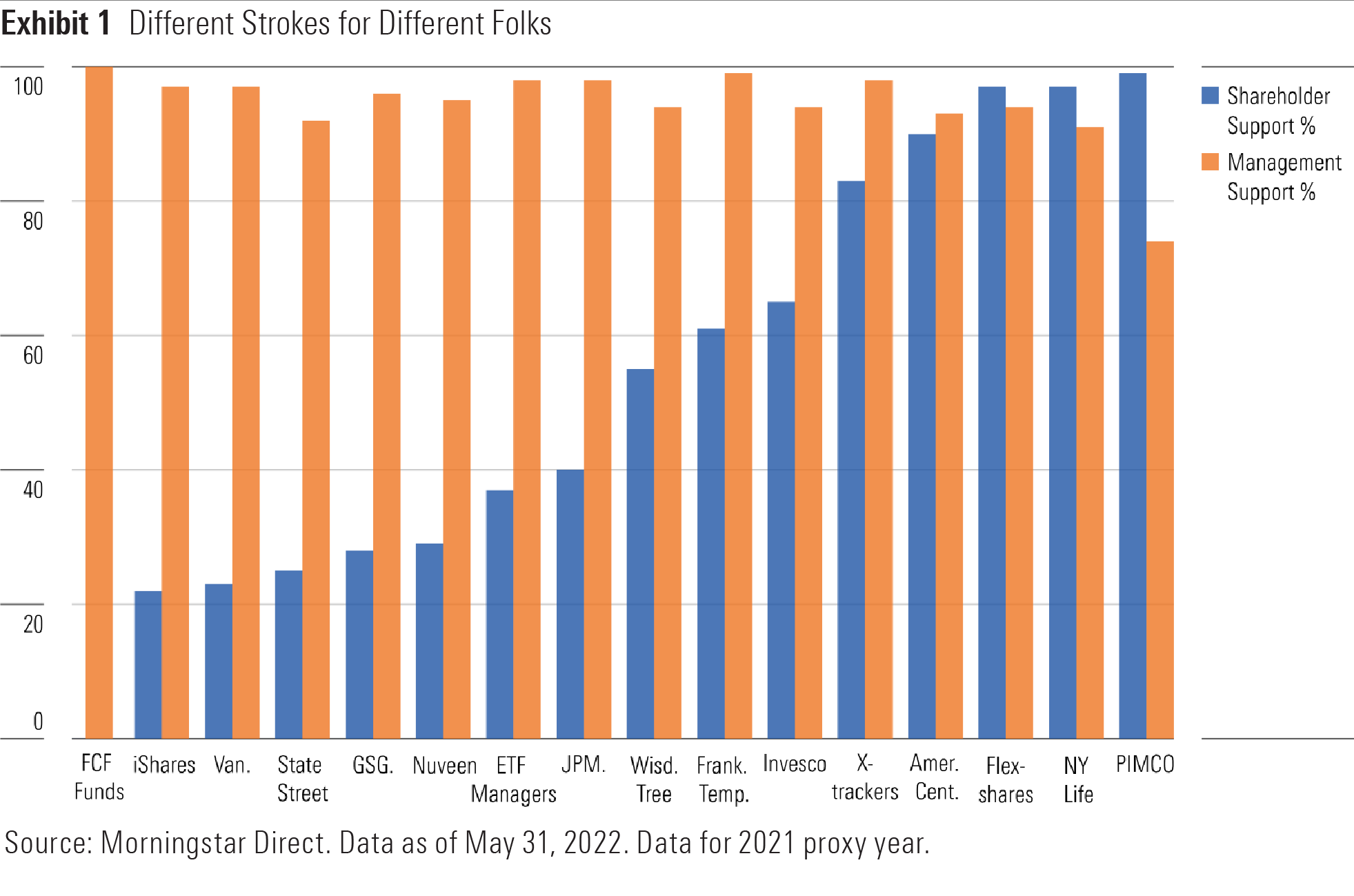

These examples illustrate the power potential of an activist campaign, but counterarguments raise questions about their true intentions and lasting impact. To better evaluate asset managers’ active ownership, I reviewed proxy vote data from 2021 for 83 sustainable ETFs from 31 issuers to look for patterns of support for shareholder and manager resolutions. I aggregated votes by asset manager and included only firms with a minimum sample size of 100 votes on shareholder proposals.

Exhibit 1 shows the wide dispersion of how asset managers vote on shareholder resolutions, spanning 0 to 99% votes of support. Appearing on either end of the spectrum raises a red flag on the firms’ due-diligence processes. Familiar names—BlackRock’s iShares, State Street, and Vanguard—appeared clustered near the lowest levels of support for shareholder resolutions; iShares and Vanguard were also near the highest supporters of management resolutions. This calls into question the degree of change these firms truly seek.

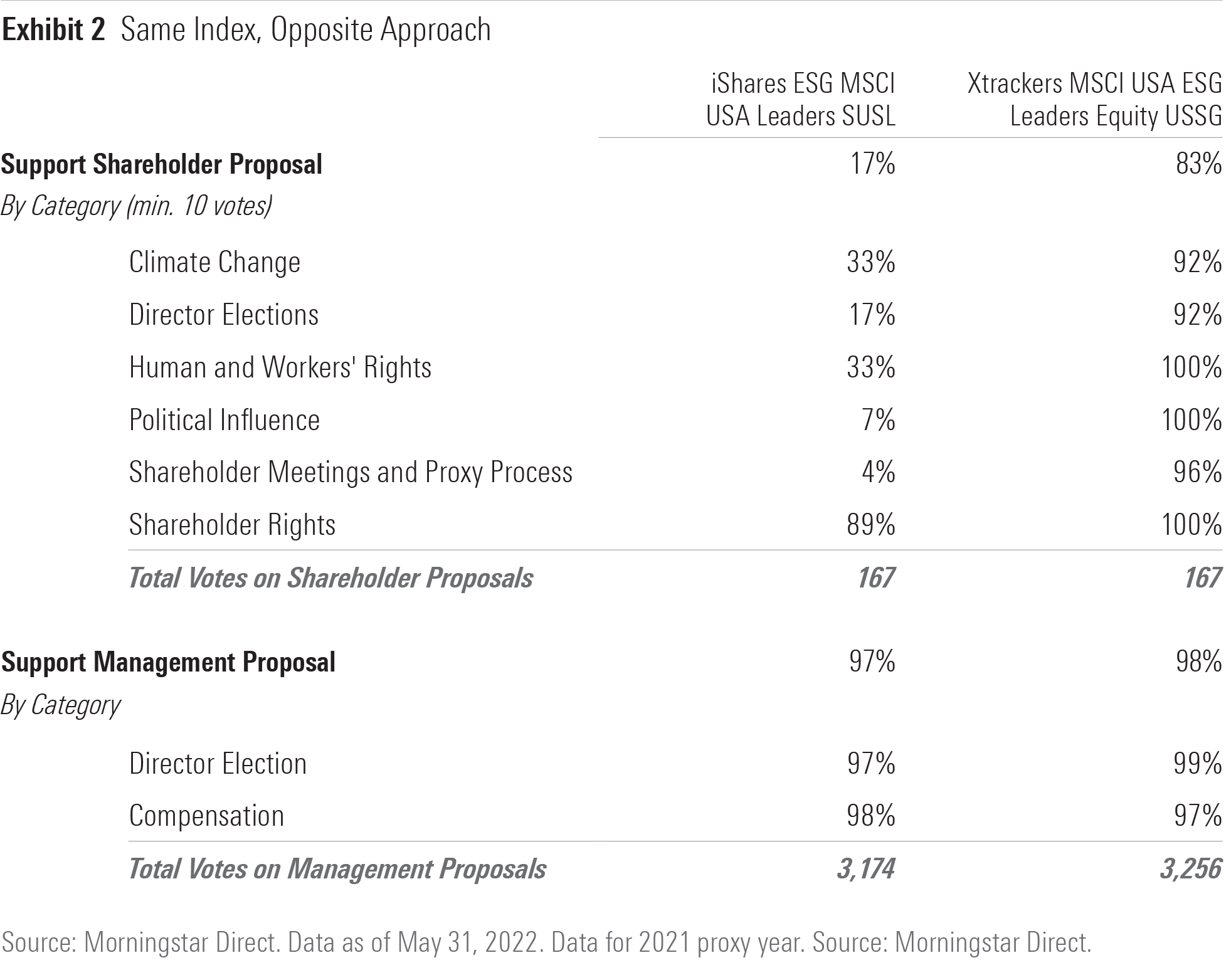

These votes aggregate across different portfolio companies and are not a pure apples-to-apples comparison. For a more direct comparison of voting records, I found a pair of ESG funds from different asset managers that track the same index. Each fund holds substantially the same portfolio. Exhibit 2 details the 2021 proxy year voting records of funds tracking the MSCI USA ESG Leaders Index.

There are challenges for investors in selecting a particular index and fund that fits their preferences and goals. The chasm between the Xtrackers fund and the iShares fund in their support of shareholder resolutions shows that voting records and active ownership should factor into investors’ selection process. Comparing another pair of funds tracking the same index, this time between Xtrackers and State Street—Xtrackers S&P 500 ESG ETF SNPE and SPDR S&P 500 ESG ETF EFIV—yielded similar results. Investors looking for more impact from their votes may be better off holding the Xtrackers funds, all else equal.

But proxy voting isn’t the only consideration. Just as we saw counterarguments to the campaigns by BlackRock, State Street, and Engine No. 1, Xtrackers’ European parent company, DWS, recently took a hit to its reputation on sustainability. DWS’ offices were raided in May 2022, and its CEO resigned amid allegations of greenwashing.

Active Ownership Is in the Eye of the Beholder

There is no one-size-fits-all in sustainable investing. Investor goals and preferences should dictate their investment choices. Active ownership provides another way for investors to maximize their sustainability objectives. The examples covered here demonstrate the complexity in evaluating asset managers’ stewardship and the need to continuously monitor their actions and approach to active ownership.

I turned to Lindsey Stewart, director of investment stewardship research at Morningstar, for advice on how investors can find asset managers that align with their goals. He responded that “asset managers tend to publish updated proxy voting policies and engagement priorities at least once a year, ahead of proxy season. These policies often give useful insights to investors on what each asset manager expects of investee companies on major environmental and social issues like climate change and diversity, equity, and inclusion, or on other issues of increasing prominence like nature and biodiversity, human rights and labor rights, or corporate political activity.”

Monitoring of asset managers’ active ownership practices has proved just as critical as finding the right fit when selecting a fund. This can often be achieved thanks to increased disclosures around asset managers’ active ownership activities. “It has become common for managers to compile detailed stewardship reports—at least annually, sometimes more frequently—outlining how their voting and engagement activities stack up against policies they’ve previously set out. They’re a really useful tool for investors to hold asset managers to account for their performance in these areas,” Stewart added.

The future of active ownership seems bright given the structural changes and focus it has received in recent years. In looking to the future, Stewart shared a vision of companies adopting better ESG-related disclosures that would increase their accountability as well as asset managers’. “This would enable a much higher level of rigor and accountability in active ownership practice and reporting that can only be of benefit to investors,” said Stewart. Better ESG and active ownership information would go a long way in maximizing investors’ success in sustainable investing.

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Morningstar, Inc. does not market, sell, or make any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/CFV2L6HSW5DHTFGCNEH2GCH42U.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/7JIRPH5AMVETLBZDLUSERZ2FRA.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/YWKBIVULT5DGJEIGAJGBA6H5ZA.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/0fa19b38-60f6-4a0f-9e06-9869d9c57d52.jpg)