How Can Fund Providers Protect the Future for Worker-Investors?

Stewardship is an opportunity for fund providers to connect with sustainability-minded investors, and many large asset managers are using proxy votes to press for better governance of environmental and social risks.

Leo Strine, former Chief Justice of the Delaware Supreme Court, describes "worker-investors" as the "99 per cent of Americans [who] owe most of their wealth to their jobs" and who "… do not benefit when some companies offload the costs of their activities, such as pollution and carbon emissions, on to everyone else."[1]

Healthy capital markets need vigilant investors. Vigilance is exercised through selecting good investments and rejecting bad ones. It’s also exercised through active ownership, the ability of shareholders to influence corporate governance at investee companies.

Heightened investor anxiety about issues like climate change is driving a global investor stewardship movement--the gathering pace at which investors are organizing into coalitions, undertaking engagements with companies, and supporting shareholder resolutions that address how companies are governing environmental and social risks.

Mutual funds and exchange-traded funds collectively own a sizable stake in the global equity market. As investment fiduciaries, the asset managers that offer those funds are under growing pressure from investors, clients, peers, and regulators to use their voting power and other stewardship strategies to advance sustainable business practices at investee companies.

They are also being called on to be stewards of the financial system itself. Consider the new wording in the introduction to the U.K.'s revised, and globally influential, stewardship code:

“… asset owners and asset managers play an important role as guardians of market integrity and in working to minimise systemic risks as well as being stewards of the investments in their portfolios.”

Much of this pressure is coming from the world’s largest asset owners--the big pension funds, who are growing increasingly assertive in calling on asset managers to offer investment approaches that align with their values and their long-term investing goals.

In this context, proxy voting, which gives investors considerable influence over corporate governance, is becoming increasingly important to asset managers.

An encouraging set of findings has emerged from the proxy votes of large asset managers in 2019, based on Morningstar’s fund proxy vote data.

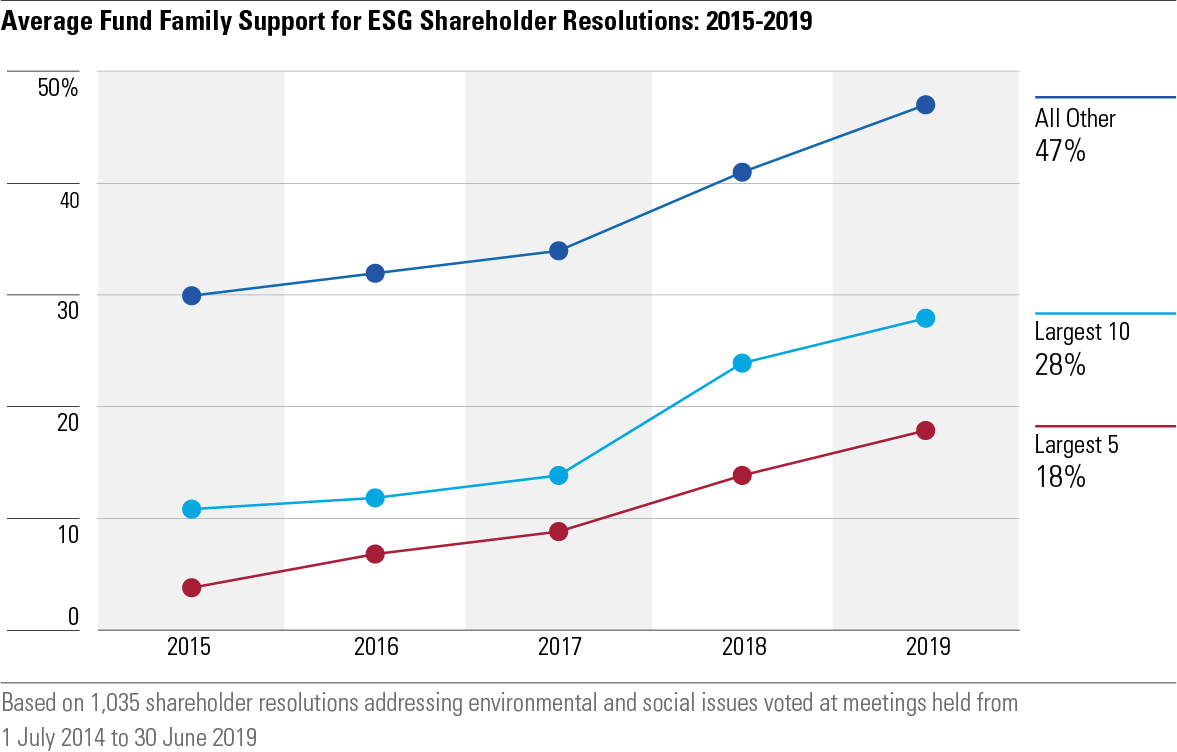

Across 55 large fund families with more than $17 trillion in assets, shareholder-proposed sustainability resolutions were supported 44% of the time, up from 26% in 2015 and increasing by 7 percentage points in each of the last two proxy seasons.

In 2019, 177 resolutions were put on company ballots by shareholders asking boards to address risks like climate change, environmental stewardship, pay equity, diversity, reputational and liability risks from products linked to social harms, political influence, animal welfare, cybersecurity, and online content governance.

More than 1,000 of these sorts of ballot initiatives have been voted over the past five years. And more than half a million votes on these initiatives were cast by funds belonging to one of the 55 large fund families included in this analysis.

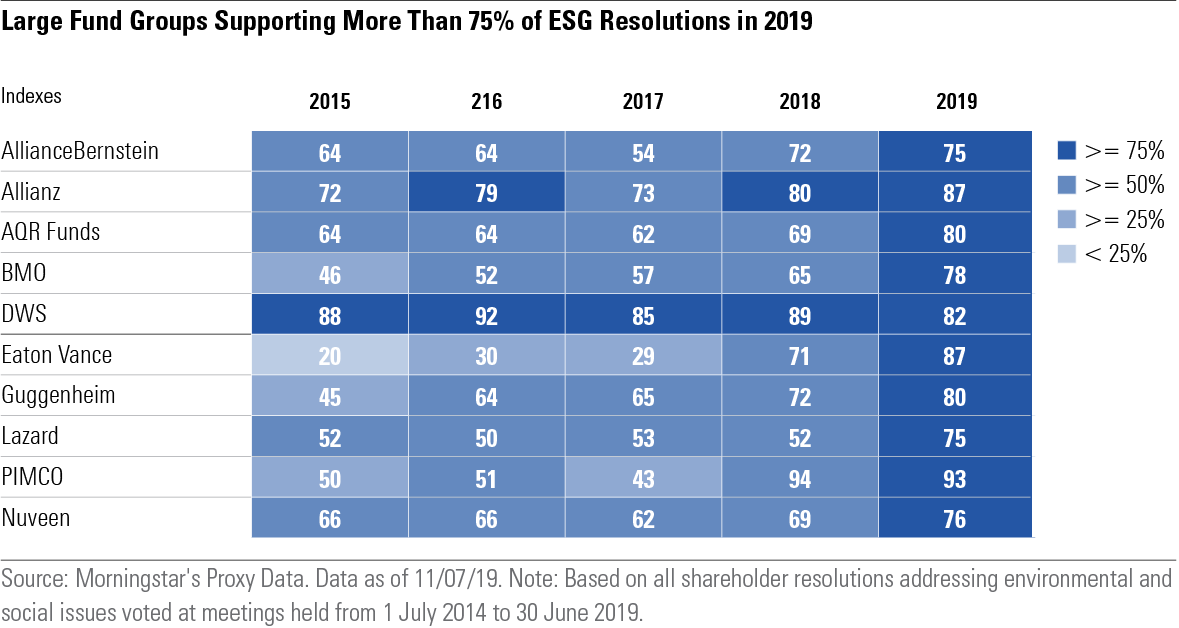

Ten of these 55 large fund groups voted ‘for’ at least 75% of sustainability resolutions in 2019.

In addition, 14 fund groups expanded their support for ESG-related shareholder resolutions in 2019 by more than 20 percentage points over their respective previous four-year averages, most notably, American Century; Eaton Vance; and Fidelity’s index funds, managed by Geode.

Unfortunately, the largest of the fund providers did not keep pace with their smaller peers and this has important implications for how much can be achieved through the proxy process.

Five of the 10 largest fund families supported fewer than 12% of sustainability resolutions voted in 2019. These are Vanguard, BlackRock, American Funds, T. Rowe, and Dimensional Funds. Given the volume of votes they control, their opposition to ESG shareholder initiatives significantly lowers overall support, despite the trend of increasing asset manager votes in favor of these resolutions.

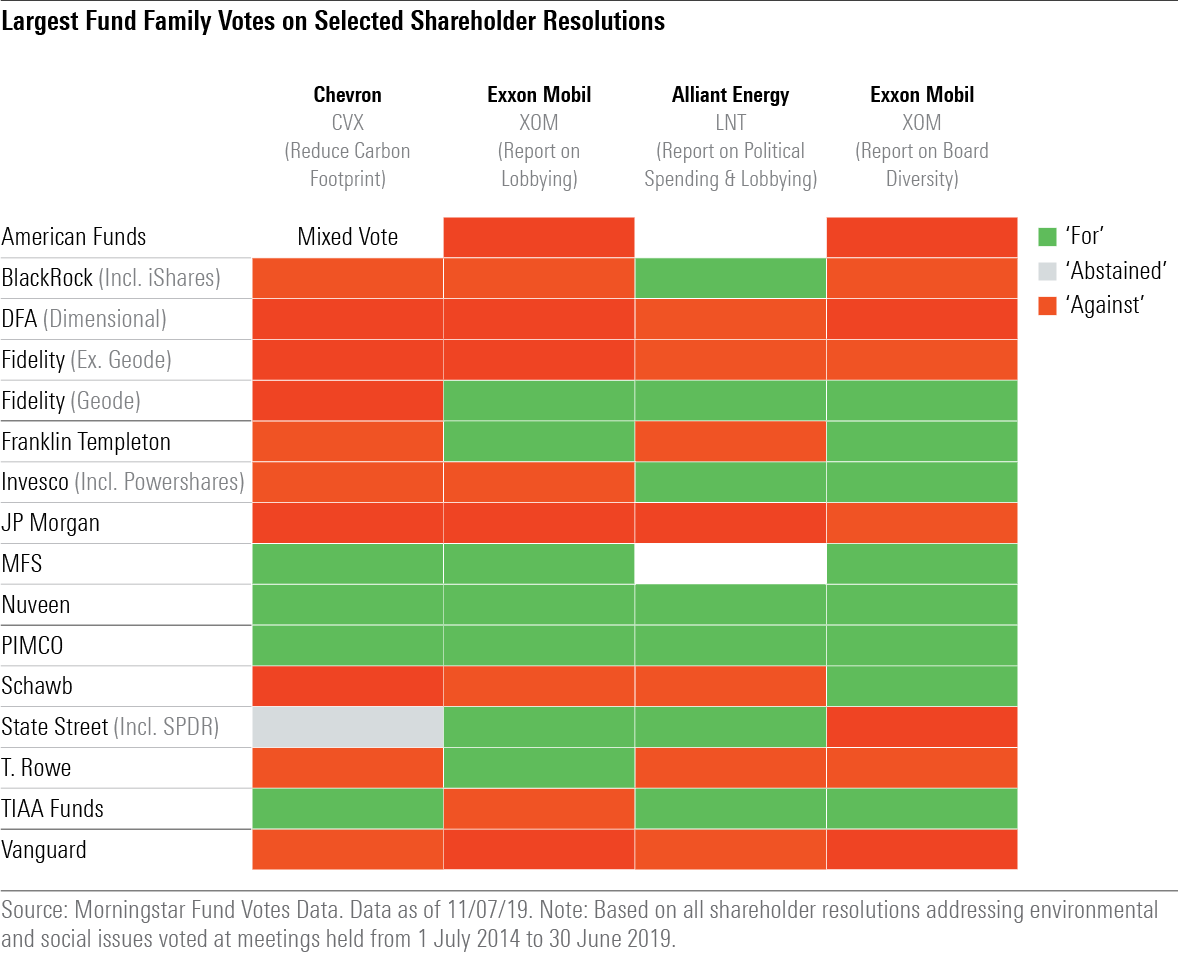

For example, a resolution voted at Chevron CVX asked the company to disclose plans to reduce its carbon footprint in line with the Paris Climate Agreement. The ballot initiative earned 33% support from shareholders. Had Chevron’s largest three institutional holders--BlackRock, Vanguard, and State Street--supported the measure, it would have passed with majority support.

Lobbying transparency is now a core component of the investor agenda to push companies to plan for low-carbon policy scenarios. Climate policy delays due to heavy lobbying by fossil fuel companies and their trade associations threaten trillions of dollars in investments. Where fiduciaries oppose lobbying transparency, they could be failing their investors.

Had Vanguard and BlackRock voted their stakes in support of lobbying transparency at Exxon’s annual meeting in May 2019, the proposal, earning 37% support from shareholders, would have passed by a comfortable margin. A resolution asking Alliant Energy LNT to disclose its political campaign and lobbying spending earned 54% support, notwithstanding Vanguard, its largest institutional holder, voting its 11% stake against the resolution.

The low-carbon transition challenge for investors is also about managing the human transition. Inclusivity is an essential tool in the fight to contain climate change. Companies led by more diverse boards perform better, and having more women in corporate leadership leads to a more-inclusive corporate culture and fewer instances of corporate scandal. Recent academic research shows that countries with female political leadership pass more progressive climate policies, resulting in lower national carbon dioxide emissions.

It stands to reason that one of the most effective strategies for aligning corporate governance with the low-carbon transition challenge is to increase board diversity.

A board diversity resolution at Exxon earned 30% support. Only one of Exxon’s largest five institutional holders, Geode (Fidelity’s index fund manager), supported the measure. Had Vanguard, BlackRock, State Street, and Capital Group (managing American Funds) voted ‘for’, the measure would have passed.

For asset managers, stewardship is becoming an imperative in winning asset-management mandates with large pension funds. Influential international stewardship codes--the regulatory or industry-led principles that guide active ownership by investment fiduciaries--are giving asset owners specific strategies for incorporating stewardship into their mandates with asset managers.

In May 2019 the UK Association of Member-Nominated Trustees, which represents the financial interest of pension fund beneficiaries, requested the UK financial services regulatory authority, the Finance Conduct Authority, to investigate "opacity and lack of comparability" in voting policies and practices of asset managers, lamenting that "…too many fund managers' public policies are, in the areas studied, out of alignment with either best practice or asset owners' and societal concerns."

Worker-investors’ interests align quite well with those of large pension funds.

Therefore, stewardship is also an opportunity for fund providers to connect with sustainability-minded investors. Passive fund providers competing on price can differentiate their offerings through stewardship. Active fund providers competing with passive providers can offer informed and strategic ESG stewardship to achieve impact.

Besides voting in support of shareholder-proposed sustainability resolutions, asset managers can tailor their votes on management-proposed resolutions, such as director elections and say on pay, to align corporate governance to investors’ long-term interests.

The policy statement that guides BlackRock's proxy voting says that, "…for companies in sectors that are significantly exposed to climate-related risk, we expect the whole board to have demonstrable fluency in how climate risk affects the business and how management approaches assessing, adapting to, and mitigating that risk." Note to boards: don't leave it too late to consider climate competence as a board renewal principle.

Geode's proxy voting guidelines state: "Geode may take action against the re-election of board members if there are serious concerns over ESG practices or the board failed to act on related shareholder proposals that received approval by Geode and a majority of the votes cast in the previous year." Note to Alliant Energy: Let's hear more about your political and lobbying spending.

Large pension funds file many of the resolutions that come to vote. For instance, the diversity and lobbying resolutions voted at Exxon and Alliant, respectively, were filed by New York City’s Retirement Systems and Pension Funds.

Of the thousands of sustainability resolutions that have come to vote over the years, many have been filed by asset managers--but only by asset managers with an explicit sustainable investing mandate.

If large asset managers disagree with the specifics of most shareholder resolutions up for vote, they could file their own. One well-placed resolution filed by one of the largest three asset managers, calling on a large and reticent oil and gas company to provide a TCFD-aligned climate report, would likely be a tipping point for corporate climate risk transparency.

--------------------------------------------

[1] Leo Strine. "Workers must be at the heart of company priorities," Financial Times, 30 Sept 2019.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/RFJBWBYYTARXBNOTU6VL4VSE4Q.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/WYB37DY4NVDTVNZTSBDENH3GMI.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/JPJHXR5CGSNR4LKQF5ZKLCCVYQ.png)