5 Things About Sustainable Investing in the First Half of 2018

Fink's letter, Parkland, Labor Department guidance on retirement plans, new funds, and record flows.

/s3.amazonaws.com/arc-authors/morningstar/42c1ea94-d6c0-4bf1-a767-7f56026627df.jpg)

Larry Fink's annual letter to CEOs. The first big thing about sustainable investing came along in January, when the head of BlackRock--the world's largest asset manager--urged CEOs to think long term, benefit all their stakeholders, and make a positive contribution to society. In so doing, Fink was not urging them to make less money. Just the opposite, he was urging them to position their businesses for long-term profitability by keeping their focus on a bigger picture that includes the role of the corporation in society. Companies focused on minimizing negative environmental and social impacts and accentuating positive ones will be rewarded by increasingly aware customers, will protect their brand, and will attract top talent, enabling them to better navigate the transition to an increasingly low-carbon and digital economy.

The letter generated a lot of attention, but to me it was a one-sided debate. Who's for short-termism? Who's for ignoring stakeholders at a time when global capitalism clearly needs to be made to work for more people? Who's for not taking issues like climate change, diversity, and data privacy into account in corporate and investment decision-making?

A few investors tried to counter by using Milton Friedman's nearly half-century-old exhortation that profit maximization is what business is about, not social purpose, by which they assume any corporate spending for social purpose is value-destroying because it has nothing to do with the business itself.

But Fink's argument transcends that one. Social purpose is an investment in long-term profitability. I don't know of a single corporate CEO who spoke out against Fink's letter. Sustainable investing gives them the space they need for bigger-picture thinking.

Parkland. Whether or not a fund invests in gun manufacturers or gun retailers can lead to some confusion about whether that is part of sustainable investing, but the Parkland tragedy in February sparked a lot of investor interest in understanding what kinds of objectionable companies are in portfolios--particularly those of passive funds. Although many sustainable-investing funds still use negative screening and many exclude guns, the focus today is on using environmental, social, and governance criteria to determine what companies are best positioned to adapt to a changing world. It isn't inherently about automatic exclusions.

Nonetheless, many fund investors were disappointed to find out that their index funds contained gunmakers or retailers that sold guns, and that there was little they could do about it. That prompted BlackRock, for one, to engage with those companies, which likely played a role as several retailers agreed to limit or end their sales of guns--although direct public pressure and concerns about reputation may have been bigger influences. BlackRock also announced that gun retailers would be excluded from all of its ESG funds (nearly all of which are iShares exchange-traded funds) and launched iShares MSCI USA Small-Cap ESG Optimized ETF ESML, which also excludes gunmakers and gun retailers--it is the only broad-market passive small-cap fund in the United States that does so.

After Parkland, more investors and advisors were confronted with the fact that inexpensive passive portfolios contain some uncomfortable holdings, opening the way for more to consider investing in sustainable funds, and that asset managers running passive portfolios nonetheless need to actively engage with companies they own. That is one way to address investor concerns while at the same time driving shareholder value in companies they'll own over the long-run.

The Department of Labor's Field Assistance Bulletin. Retirement plan participants overwhelmingly want sustainable investment options, especially millennials. A Morgan Stanley survey last year found that 90% of millennials want a sustainable investing option as part of their 401(k) plans. A 2015 Department of Labor Interpretive Bulletin made it clear to plan fiduciaries that they can add sustainable investing options to retirement plans. The "all things equal" test, in essence, says that a fund added to a retirement plan that offers the extra benefit of social or environmental impact must be judged on its financial merits relative to conventional strategies. In other words, a large-cap growth sustainable "impact" fund must have a risk/return profile that's competitive with large-cap growth funds overall. However, the guidance also said that if a fund is using ESG criteria as part of the investment process to enhance financial returns, without claiming any broader impact, then it should be considered using the same criteria as with any fund.

In April 2018, the Labor Department issued a Field Assistance Bulletin to help fiduciaries interpret the Interpretive Bulletin. Coming from a new administration that seems not exactly aligned with sustainable investing, it's not surprising that the new bulletin muddied the waters a bit. The focus was on qualified default investment alternatives, or QDIAs. These are the investments that plan participants are defaulted into when they don't choose a plan option for themselves. Most QDIAs these days are target-date funds, and for good reason they are attracting the bulk of flows into 401(k) plans.

Can sustainable target-date funds be designated as QDIAs? The Field Assistance Bulletin tried to distinguish between ESG-themed funds and those that may be using ESG criteria as part of their investment process to deliver superior risk-adjusted returns. The former, which I would call "impact" funds, are those that aim to deliver some type of measurable societal or environmental "impact return" alongside their financial return. They are not, however, trying to do so at the expense of their investment returns.

Well, according to the April bulletin, impact funds might not be appropriate QDIAs if some plan participants might disagree with their impact aims:

The decision to favor the fiduciary's own policy preferences in selecting an ESG-themed investment option for a 401(k)-type plan without regard to possibly different or competing views of plan participants and beneficiaries would raise questions about the fiduciary's compliance with ERISA's duty of loyalty.

But what if the choice is made by taking into account a broad cross-section of employee views? What if 90% want a sustainable fund? Would that answer any questions about duty of loyalty?

As firms start to develop sustainable target-date funds, which is happening with at least three major asset managers that I know of (only Natixis has one now, and it's only two years old), they will likely keep the focus on integrating ESG criteria within the investment process to generate financial return rather than try to offer measurable ancillary societal or environmental impacts. Under such conditions, as long as these funds can compete on the performance front, they can be QDIA candidates. The Field Assistance Bulletin didn't change the overall guidance from 2015, but it was written in a discouraging tone that may make already risk-averse retirement-plan fiduciaries less apt to consider sustainable investment options.

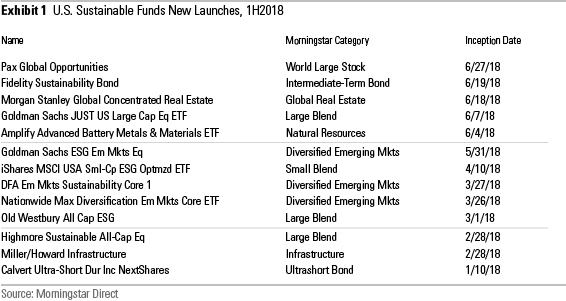

New Fund Launches and Repurposed Funds. The sustainable funds universe in the U.S. continued to expand in the first half of 2018. A total of 13 new funds launched (eight open-end and five ETFs) and 28 existing funds added ESG or impact criteria to their investment processes, as described in their prospectuses. According to my count, there are now 285 sustainable open-end funds and ETFs available to U.S. investors. To make my list, a fund must make clear in its prospectus that it uses sustainability or ESG criteria and/or seeks to deliver measurable impact alongside financial returns.

During the quarter, Fidelity launched a bond index fund, Fidelity Sustainability Bond FNASX, which can be combined with its sustainable U.S.- and international-equity funds to complete a basic stock-bond portfolio. Goldman Sachs got into the act, launching an emerging-markets fund and an ETF based on sustainability research from Paul Tudor Jones' JUST Capital. Just prior to quarter-end, Vanguard announced that it would launch two ESG ETFs in the third quarter.

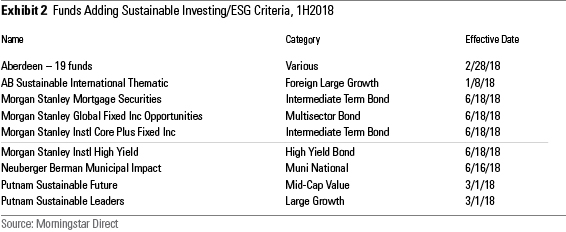

Asset managers have begun adding sustainability criteria to the prospectuses of existing funds and, in some cases, referring to it in the funds' names, the latter an indicator of a more significant commitment. In 2017, 17 existing funds added ESG to their prospectuses. The trend continued in the first half of 2018 with another 27 funds adding ESG criteria. Aberdeen Funds account for most of this year's retoolings, but it's significant because the firm has decided to add ESG criteria to all its funds. Morgan Stanley appears to be doing the same thing, adding ESG criteria to four bond funds after doing so for 10 of its international-equity funds last year.

In some cases, existing funds are getting complete ESG facelifts. Putnam turned Putnam Multi-Cap Growth into Putnam Sustainable Leaders PNOPX and Putnam Multi-Cap Value became Putnam Sustainable Future PMVAX. In June, Neuberger Berman turned a New York muni fund into Neuberger Berman Municipal Impact NMIIX.

Repurposing funds as sustainable allows asset managers to leverage existing assets to build their sustainable-funds business, thereby avoiding having to create funds from scratch and the sometimes long wait to reach scale. Many large asset managers have an inventory of actively managed equity funds with large but seasoned asset bases that cannot attract new assets at the rate they are losing assets from routine withdrawals made by longtime investors. For that reason and because more asset-managers are coming to terms with how they want to incorporate ESG into their particular processes, I expect this trend to continue.

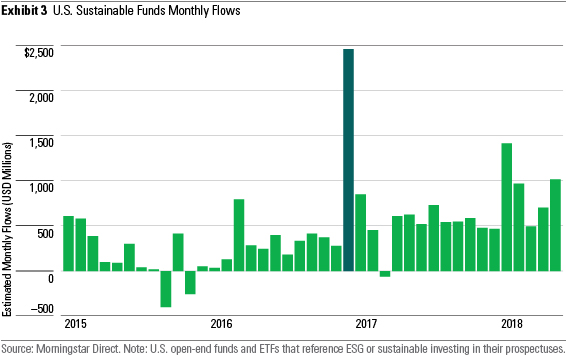

Continued Strong Flows. For the first five months of 2018, sustainable funds averaged $924 million per month in net flows. That is nearly twice last year's monthly average of $532 million. And it is far more than sustainable funds were getting in the period before the 2016 election. From 2015 through November 2016, sustainable funds had already begun their growth spurt, but their average monthly net flows were $236 million. In December 2016, sustainable funds garnered a record single-month net flow of $2.5 billion. Since that time, sustainable funds have averaged $647 million in net flows per month and, as noted, well more than that so far this year.

Jon Hale has been researching the fund industry since 1995. He is Morningstar’s director of ESG research for the Americas and a member of Morningstar's investment research department. While Morningstar typically agrees with the views Jon expresses on ESG matters, they represent his own views.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/RFJBWBYYTARXBNOTU6VL4VSE4Q.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/WYB37DY4NVDTVNZTSBDENH3GMI.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/JPJHXR5CGSNR4LKQF5ZKLCCVYQ.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/42c1ea94-d6c0-4bf1-a767-7f56026627df.jpg)