Where Are the Bargains in Tech in 2022?

We remain bullish on the key secular trends in technology but think the sector overall is a little pricey.

/s3.amazonaws.com/arc-authors/morningstar/5c8852db-04a9-4ec5-8527-9107fff80c09.jpg)

The technology sector was a strong market outperformer at the beginning of the COVID-19 pandemic and outperformed the broader market through most of 2021. Tech was an outperformer once again in the fourth quarter, but we suspect that strong performance among mega-cap Tech stocks is masking underperformance from smaller Tech stocks. Regardless, we remain bullish on the key secular tailwinds within Technology, such as cloud computing, 5G, and the "Internet of Things." Tech valuations are slightly rich, in our view, but software is an area that has pulled back and we now view the sector as fairly valued. We still see some attractive margins of safety for investors in large-cap software but also some of the high-flying remote software stocks that ripped higher in 2020 but have fallen out of favor more recently.

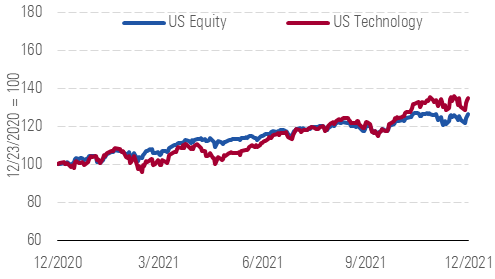

As of Dec. 23, the Morningstar U.S. Technology Index was up 34.7% on a trailing twelve-month basis, outperforming the U.S. equity market, which is up 26.4% on a TTM basis (Exhibit 12a). Over the past three months, Tech outperformed the broader market, up 15.9% as compared to the U.S. equity market up 8.6%.

The Gap Between Tech and the Broader Market Widened in Q4

Source: Morningstar analysts

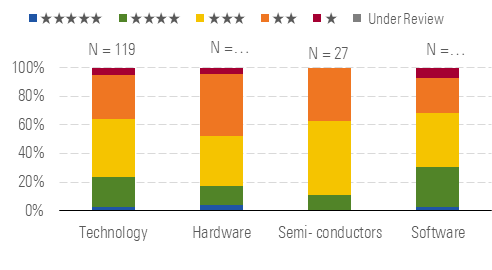

As of Dec. 23, the median U.S. technology stock was 9% overvalued, pulling back as it was 14% overvalued a quarter ago. Hardware remains the least attractive sub-sector to us as it is overvalued by 16%. Semiconductors are overvalued by 10%, up from being 7% overvalued a quarter ago. Software is now only 4% overvalued, versus 13% overvalued a quarter ago (Exhibit 12b).

We See More Buying Opportunities in Software Than a Quarter Ago

Source: Morningstar analysts

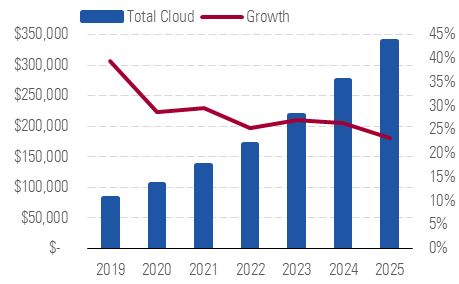

In software, IT departments have been focused on digital transformation for several years, first from the secular shift to cloud computing and software as a service, or SaaS, followed by the coronavirus pandemic and the critical rush to implement remote working tools. We foresee enterprises using software to modernize all types of business processes, in turn leading to software industry growth at a low-double-digit CAGR. (Exhibit 12c).

The Cloud Opportunity Is the Most Obvious Secular Theme in Software

source: Morningstar analysts

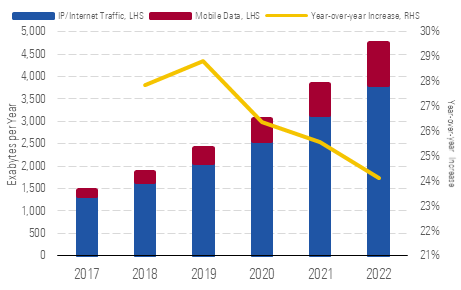

Additionally, the explosion of data should not be slowing down. This bodes well for cloud computing firms like

The Explosion of Data Should Not Be Slowing Down

Source: Morningstar analysts

Top Picks

VMware

VMW

Star Rating: ★★★★

Economic Moat Rating: Narrow

Fair Value Estimate: $175

Fair Value Uncertainty: High

We believe that VMware has developed an enviable position by becoming the commonality between clouds, including the hyperscale cloud providers, and on-premises environments. The integration of container management within its tried-and-true virtualization platform can give enterprises one solution for application and infrastructure teams, and we expect increased cross- and up-selling to come from VMware's robust security portfolio. The firm's migration toward subscription and SaaS-based offerings is well underway and we expect VMware to benefit from customers attempting digital transformations.

CRM

Star Rating: ★★★★

Economic Moat Rating: Wide

Fair Value Estimate: $320

Fair Value Uncertainty: Medium

We believe Salesforce.com represents one of best long-term growth stories in large cap software. In our view, Salesforce will benefit further from natural cross-selling among its clouds, upselling more robust features within product lines, pricing actions, international growth, and continued acquisitions such as the recent Tableau and Slack deals. Salesforce is widely considered a leader in each of its served markets, which is attractive on its own, but the tight integration among the solutions and the natural fit they have with one another makes for a powerful value proposition, in our opinion.

ST

Star Rating: ★★★★

Economic Moat Rating: Narrow

Fair Value Estimate: $75

Fair Value Uncertainty: High

Narrow-moat Sensata Technologies should continue to be a long-term beneficiary of greater content in electrified, autonomous, and connected vehicles. In the near term, the company has performed well in recent quarters, and we expect content growth to lead to outperformance over the automotive and heavy vehicle markets even amid ongoing supply constraints in 2021. Sensata's sensors enable electrification and emissions reduction in new vehicles, and we think an accelerating proliferation of electric vehicles and global emissions regulations will be long-term secular tailwinds for the firm.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/RNODFET5RVBMBKRZTQFUBVXUEU.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LJHOT24AYJCHBNGUQ67KUYGHEE.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/5c8852db-04a9-4ec5-8527-9107fff80c09.jpg)