After Earnings, Is Boeing Stock a Buy, a Sell, or Fairly Valued?

With the recent 737 MAX incident slowing the company from getting back on track, here’s what we think of Boeing stock.

/s3.amazonaws.com/arc-authors/morningstar/4c0ebe77-db24-4647-aac9-f4c13027ec2f.jpg)

Boeing BA released its fourth-quarter earnings report on Jan. 31. Here’s Morningstar’s take on Boeing’s earnings and stock.

Key Morningstar Metrics for Boeing

- Fair Value Estimate: $219.00

- Morningstar Rating: 3 stars

- Morningstar Economic Moat Rating: Wide

- Morningstar Uncertainty Rating: High

What We Thought of Boeing’s Q4 Earnings

- Boeing’s results were quite good. The company delivered 107 737 jets and 24 787s, and it booked more revenue and profit than we expected. These results support the thesis that Boeing was on its way to finally getting a grip on some of its production problems and promised a return to “stability” for its production rate and finances by 2025-26.

- However, that story will unfold a bit differently because of the door blowing off a 737 MAX 9 flight on Jan. 5. We estimate that because the company has had to reexamine its manufacturing processes and prove to the FAA that it can build safe planes, the plan to ramp up 737 production will take about 18 months longer than previously expected. As a result, we lowered our fair value estimate from $232 to $219 on Jan. 31.

- In the long term, we believe Boeing can and will sort through its production process and eventually regain people’s confidence that its products are airworthy. We also still see a lot of demand for narrow-body jets over the next 20 years. So we think the overall thesis is still valid, and that a shallower ramp-up in 737 production could (perhaps ironically) be healthy for Boeing in a handful of ways.

- Before the Alaska Air incident, our forecast for the rate at which Boeing could ramp up 737s was lower than the company’s stated goal and more conservative than most other estimates. Our 2025 forecast for 737 deliveries is still likely below what most others are expecting. As we learn more, depending on how long it takes for the manufacturing process to get sorted out, there could be upside to those forecasts. Boeing also has hundreds of planes in inventory that are getting reworked after the latest defects were identified. When they are finished and delivered, these planes can add quite a lot to the firm’s cash flows in 2024 and 2025, even if they are still capped at building 38 new planes per month for the time being.

- The question for investors is what margin of safety they’d want, and what signals other investors are likely to look for as the “all clear” from Boeing. It could be a while before we get that signal, and we maintain a High Uncertainty Rating for the firm.

Boeing Stock Price

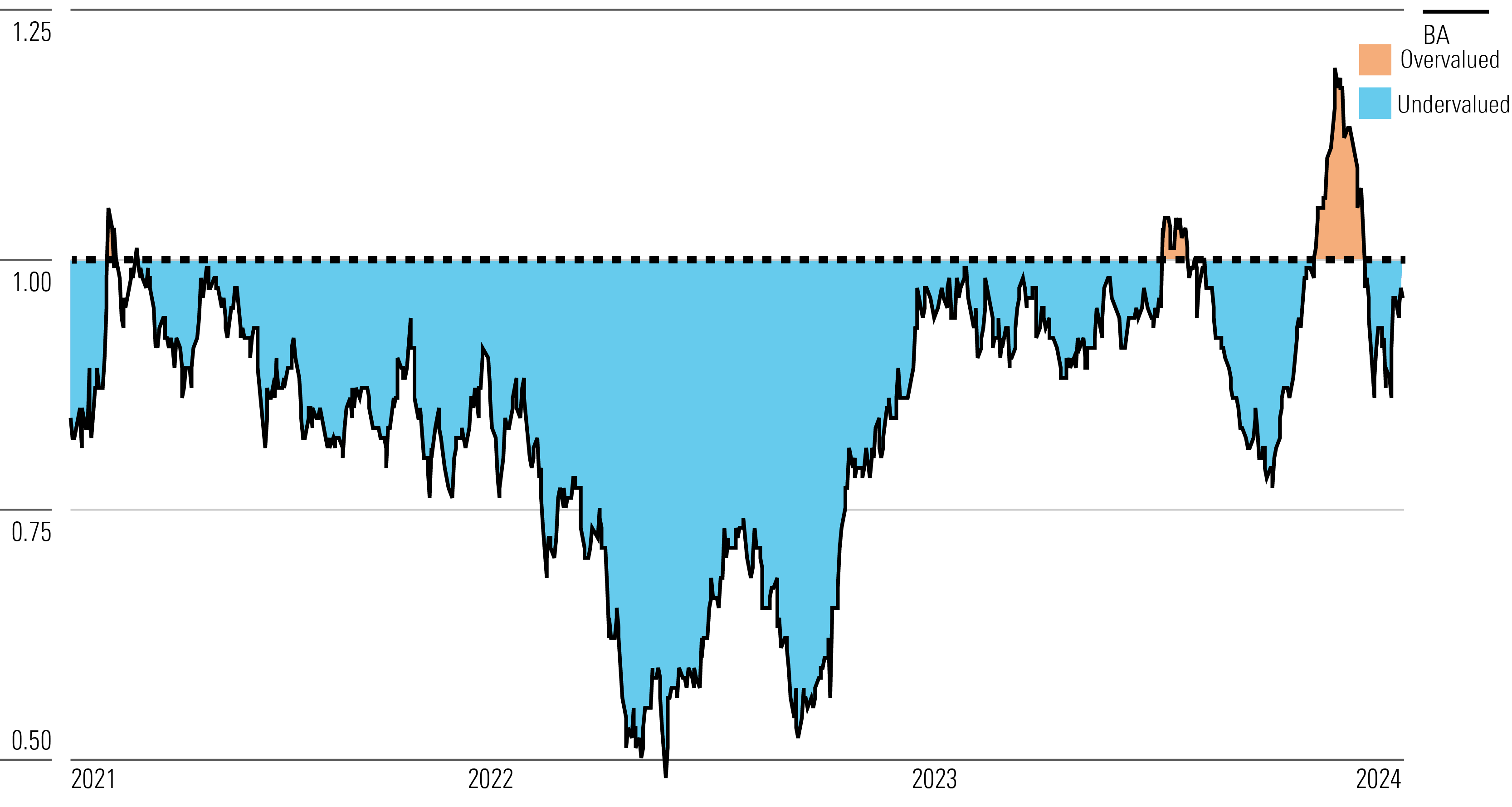

Fair Value Estimate for Boeing

With its 3-star rating, we believe Boeing’s stock is fairly valued compared with our long-term fair value estimate of $219 per share, which represents an equity value 29 times our 2025 EBITDA free cash flow and 1.3 times our 2025 sales estimates. We think the enormous special charges and fleet groundings are mostly behind Boeing, and we forecast one or two more years of hard slogging as it clears up the manufacturing and supply chain issues that hamper its production pacing. Our valuation includes healthy long-term global demand for Boeing’s products and the successful scaling up of deliveries and eventually margins on its bread-and-butter 737 and 787 models in 2026-27.

The COVID-19 crisis shocked the aviation industry and essentially halved global revenue passenger kilometers in 2020. Beyond the pandemic and lingering manufacturing headaches, we assume a replacement cycle among most airlines will take place, and that the vast majority of fleet growth will be from narrow-body aircraft as an emerging-market middle class demands more short-haul and point-to-point medium-haul travel.

We anticipate that it will take until mid-2025 for Boeing to stabilize its manufacturing processes and certify that its planes are consistently built to their specified design and safety standards. In the longer term, we expect that a mix shift toward the high-margin 737 MAX and eventual returns to learning-curve-based cost efficiencies should help the company improve margins. We expect the firm to return to 2018 levels of 737 MAX production by 2026. We anticipate the firm will be able to deliver 68 737 MAX a month in 2031 versus about 48 per month in 2018. We expect that volume increases in the high-margin 737 MAX will bring Boeing Commercial’s operating margin to the mid-teens.

Overall, we expect the firm’s operating margin to improve to about 13% at midcycle versus 12% in 2018. These forecasts include aggressive research and development spending on the development of a brand-new airframe design within our forecast period, though it won’t fly until the 2030s. We expect the services business will be able to regain profitability faster than Boeing as a whole because aftermarket revenue increases directly with flights.

Read more about Boeing’s fair value estimate.

Boeing Historical Price/Fair Value Ratio

Economic Moat Rating

We think Boeing merits a wide moat, as it benefits from durable intangible assets and switching costs. In commercial aircraft manufacturing, we believe the technical complexity of manufacturing and the extensive regulatory barriers to entering the market constitute wide-moat-caliber intangible assets. Both Boeing and Airbus benefit from these barriers, and it means they operate in a duopoly in the global large-frame jet aircraft market. We expect virtually all global revenue associated with air travel growth will continue to flow through their top lines. What’s more, we estimate that demand from airlines for their products will remain high enough for long enough that both firms can generate economic profits for decades. Although Boeing has taken some competitive hits, the market is large enough and so difficult to break into that it supports two wide-moat aircraft manufacturers.

We believe Boeing’s defense business is more vulnerable to operational risk than peers due to its higher exposure to fixed-price contracts, but we think the firm is turning a corner operationally. It benefits from intangible assets stemming from the technical complexity of its products, switching costs from the time and effort the military faces to switch suppliers, and a lack of viable alternative suppliers. We think Boeing Global Services has intangible assets from proprietary access to aftermarket part designs, as the Federal Aviation Administration and other regulators require that spare parts be identical to the original design. The segment also benefits from switching costs stemming from a lack of alternative suppliers for such parts.

Further, we see the lack of alternative aircraft suppliers, the criticality of their products to customers, and very long product cycles as presenting powerful switching costs. These three factors usually reinforce each other to allow for long-term economic profits to persist at both Boeing and Airbus. At present, Boeing has a superior product in the wide-body or long-haul category, while Airbus is enjoying the advantage with variants of its narrow-body A320 and A321 lines.

Read more about Boeing’s moat rating.

Risk and Uncertainty

We believe Boeing’s biggest uncertainties come from macro risks that limit demand and operational risks that constrain supply, both of which have hurt the company over the last three years. We think the firm deserves a High Uncertainty Rating, but note it is still working through much higher supply risks than Airbus as it revives 737 MAX and 787 production and deliveries.

On the demand side, the pandemic dramatically reduced air travel and aircraft deliveries. Trade group IATA reported that passenger demand declined by nearly two-thirds in 2020. While travel has returned to pre-pandemic levels in many markets, its recovery is still patchy and may face renewed disruption. China is a major aviation market, and notwithstanding the recertification of the 737 MAX in the country and resumed deliveries of new planes in due course, we suspect it may be easier (if not simply more expedient) for local airlines to substitute future marginal orders of 737s for Comac C919s while maintaining or growing their share of orders for Airbus narrow-bodies.

On the supply side, Boeing’s execution of the extraordinarily complex manufacturing process of its commercial jets poses a risk to the company’s results, as numerous errors and lapses in quality emerged between 2020 and 2024. A second major risk in the aftermath of the 737 MAX grounding and production rework on the 787 lies in global supply chain disruptions that also affect Boeing’s engine and subsystem suppliers. These suppliers may just not be able to ramp up production at Boeing’s desired pace, which would constrain or delay the firm’s ability to get its assembly up to the volume where it makes money on every plane it delivers, versus having to continue to record extraordinary charges for idle assembly capacity.

Read more about Boeing’s risk and uncertainty.

BA Bulls Say

- Boeing has a large backlog that covers several years of production for the most popular aircraft, which gives us confidence in aggregate demand for aerospace products.

- Boeing is well-positioned to benefit from emerging-market growth in revenue passenger kilometers and a robust developed-market replacement cycle over the next two decades.

- We expect that commercial airframe manufacturing will remain a duopoly for most of the world for the foreseeable future. We think customers will not have any meaningful options other than continuing to rely on incumbent aircraft suppliers.

BA Bears Say

- Boeing’s reputation for engineering prowess may have taken a permanent hit since repeated manufacturing flaws in 737 MAX jets have hampered its assembly pace and disrupted airlines’ and passengers’ schedules.

- In the long term, changed consumer behavior, especially among business travelers, could be unfavorable for aviation.

- As recent history has proved, aircraft development is notoriously susceptible to development delays, hiccups, and cost overruns.

This article was compiled by Freeman Brou.

The author or authors own shares in one or more securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ECVXZPYGAJEWHOXQMUK6RKDJOM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/KOTZFI3SBBGOVJJVPI7NWAPW4E.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/4c0ebe77-db24-4647-aac9-f4c13027ec2f.jpg)