After Earnings and a Big Rally, Is Microsoft Stock a Buy, a Sell, or Fairly Valued?

With better-than-expected results, here’s what we think of Microsoft stock.

Microsoft MSFT released its fiscal second-quarter earnings report on Jan. 30. With Microsoft’s stock up 57% in the past year, here’s Morningstar’s take on the company’s earnings report and outlook.

Key Morningstar Metrics for Microsoft

- Fair Value Estimate: $420.00

- Morningstar Rating: 3 stars

- Morningstar Economic Moat Rating: Wide

- Morningstar Uncertainty Rating: Medium

What We Thought of Microsoft’s Fiscal Q2 Earnings

Microsoft continues to impress with its solid second-quarter results, including upside on both the top and bottom lines. We find the firm’s outlook encouraging, especially for Azure. Though management will not admit as much, we continue to see indicators that the demand environment has improved at least modestly.

Artificial intelligence stole the show again this quarter. Azure is strong, especially thanks to AI. Large deals are also good, as Microsoft Office E5 upsells very well. Commercial bookings are in a good position. Overall, profitability is strong despite headwinds from the Activision acquisition.

We raised our near/mid-term estimates based on continued strong results from both a revenue growth and margin perspective. We also see AI as a bigger boost to both than what we initially modeled. Beyond that, results are consistent with our belief that Azure is a leader in the public cloud, and Microsoft’s near-monopoly positions with Windows and Office support our wide moat rating.

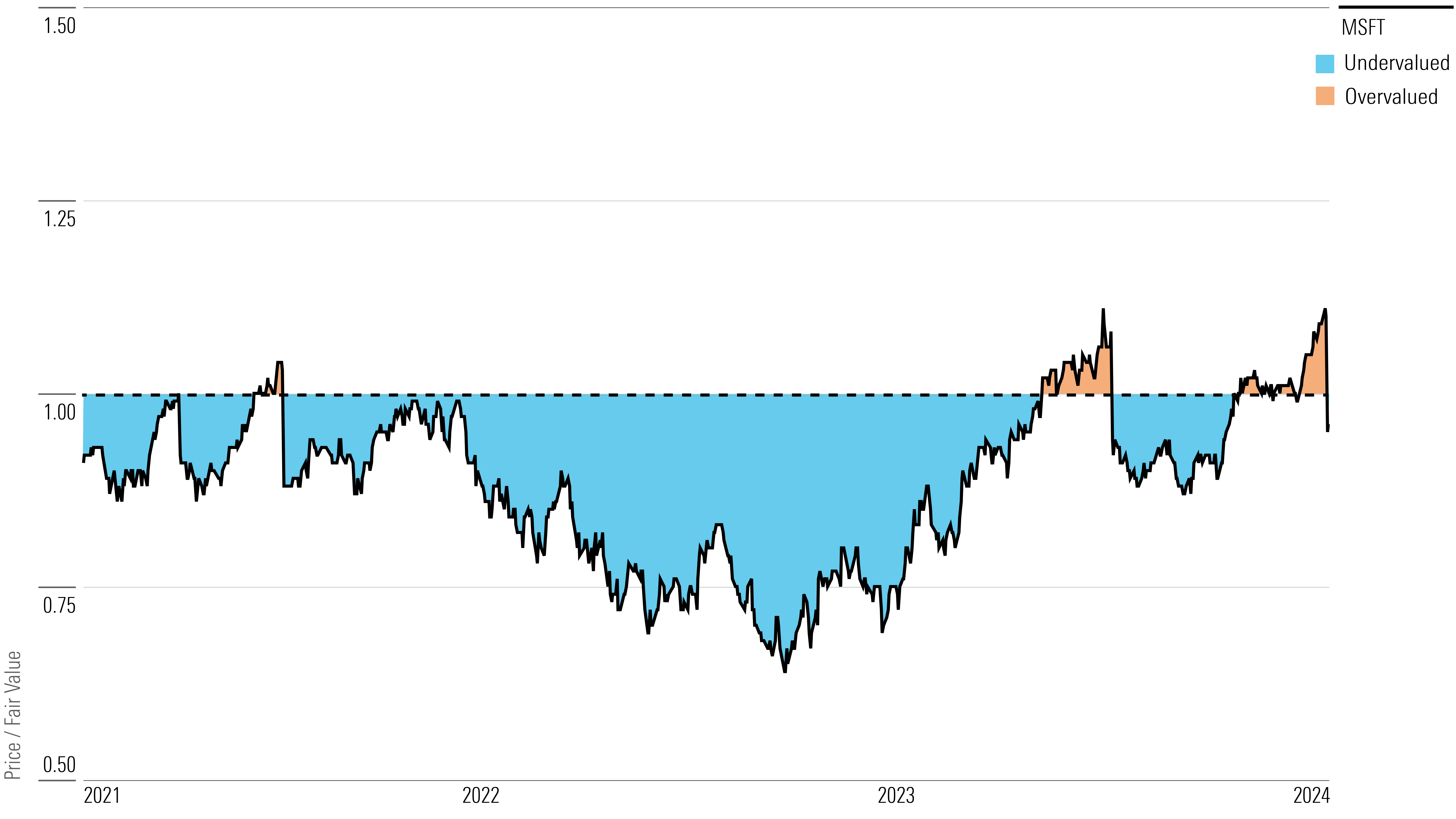

However, shares have run sharply over the last year, so the stock is fairly valued. We think enterprise users are still cautious about the macroeconomic outlook and are not currently willing to aggressively invest in IT programs/projects.

Microsoft Stock Price

Fair Value Estimate for Microsoft Stock

With its 3-star rating, we believe Microsoft’s stock is fairly valued compared with our long-term fair value estimate of $420 per share, which implies a fiscal 2024 enterprise value/sales multiple of 12 times, adjusted P/E multiple of 36 times, and a 1% free cash flow yield.

We model a five-year compound annual growth rate for revenue of approximately 13% inclusive of the Activision acquisition. We envision stronger revenue growth ahead, as Microsoft’s prior decade was bogged down by the downturn in 2008, the complete evaporation of mobile handset revenue from the disposal of the Nokia handset business, and the transition to the subscription model (which initially saw slower revenue growth). However, we believe macro and currency factors will pressure revenue in the near term.

We think revenue growth will be driven by Azure, Office 365, Dynamics 365, LinkedIn, and emerging AI adoption, and that Azure in particular will be the most critical revenue driver over the next 10 years as hybrid environments (where Microsoft excels) drive mass cloud adoption. We also anticipate that the combination of Azure, DBMS, Dynamics 365, and Office 365 will drive above-market growth as CIOs continue to consolidate vendors. We foresee More Personal Computing growing modestly above GDP over the next 10 years.

Read more about Microsoft’s fair value estimate.

Microsoft Historical Price/Fair Value Ratio

Economic Moat Rating

We assign Microsoft overall a wide moat arising from switching costs, network effects, and cost advantages. We believe the firm is a leader across a variety of key technology areas, which should result in economic returns well over its cost of capital for years to come.

We think Microsoft’s different segments and products benefit from different moat sources. The Productivity and Business Processes segment includes Office, Dynamics, and LinkedIn. We assign it a wide moat based on high switching costs and network effects. In our view, high switching costs and cost advantages drive a wide moat for Azure, which is clearly the growth engine for the Intelligent Cloud segment and one of the critical products the “new” Microsoft will be built around.

Read more about Microsoft’s moat rating.

Risk and Uncertainty

Microsoft faces risks that vary among its products and segments. High market share in the client-server architecture over the last 30 years means significant high-margin revenue is at risk, particularly in OS, Office, and Server. Microsoft has thus far been successful in growing revenues in a constantly evolving technology landscape, and it’s enjoying success in both moving existing workloads to the cloud for current customers and attracting new clients directly to Azure. However, the company must continue to drive revenue growth for cloud-based products faster than revenue declines for on-premises products.

Microsoft is acquisitive, and while many small acquisitions are completed that fly under the radar, the company has had several high-profile flops, including Nokia and aQuantive. The LinkedIn acquisition was expensive but served a purpose, and we think it’s working out well. It is not clear how much Microsoft bought in the Permira-led Informatica LBO, and it may have been an important strategic investment, but Informatica was certainly not a growth catalyst. GitHub was expensive but strategic and seems to be shaping up as a success, while the ZeniMax deal should boost the company’s first-party video game publishing efforts. While Nuance was not hard to digest, the $69 billion Activision deal was completed in October 2023 and will likely be a bit more involved.

Read more about Microsoft’s risk and uncertainty.

MSFT Bulls Say

- Public cloud is widely considered the future of enterprise computing, and Azure is a leading service that benefits the evolution to first to hybrid environments and ultimately to public cloud environments.

- Microsoft 365 continues to benefit from upselling into higher-priced stock-keeping units, as customers are willing to pay for better security and Teams Phone. This should continue over the next several years.

- Microsoft has monopoly-like positions in various areas (OS, Office) that serve as cash cows to help drive Azure growth.

MSFT Bears Say

- Momentum is slowing in the ongoing shift to subscriptions, particularly in Office, which is generally considered a mature product.

- Microsoft lacks a meaningful mobile presence.

- Microsoft is not the top player in its key sources of growth, notably Azure and Dynamics.

This article was compiled by Quinn Rennell.

The author or authors own shares in one or more securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/RNODFET5RVBMBKRZTQFUBVXUEU.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LJHOT24AYJCHBNGUQ67KUYGHEE.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)