8 Stocks to Avoid

These stocks are all extremely overvalued by our standards--and carry a good deal of uncertainty, too.

/s3.amazonaws.com/arc-authors/morningstar/35408bfa-dc38-4ae5-81e8-b11e52d70005.jpg)

Death and taxes are two of the few certainties in life. In investing, too, there are few certainties. Of course, we can improve our chances of investing success by, say, favoring low-cost, broadly diversified funds. Or by purchasing stocks of companies with solid competitive advantages.

One thing would seem to be for certain, though: Investing in stocks with unpredictable cash flows when they're trading at nosebleed valuations is a recipe for failure. These are stocks to avoid.

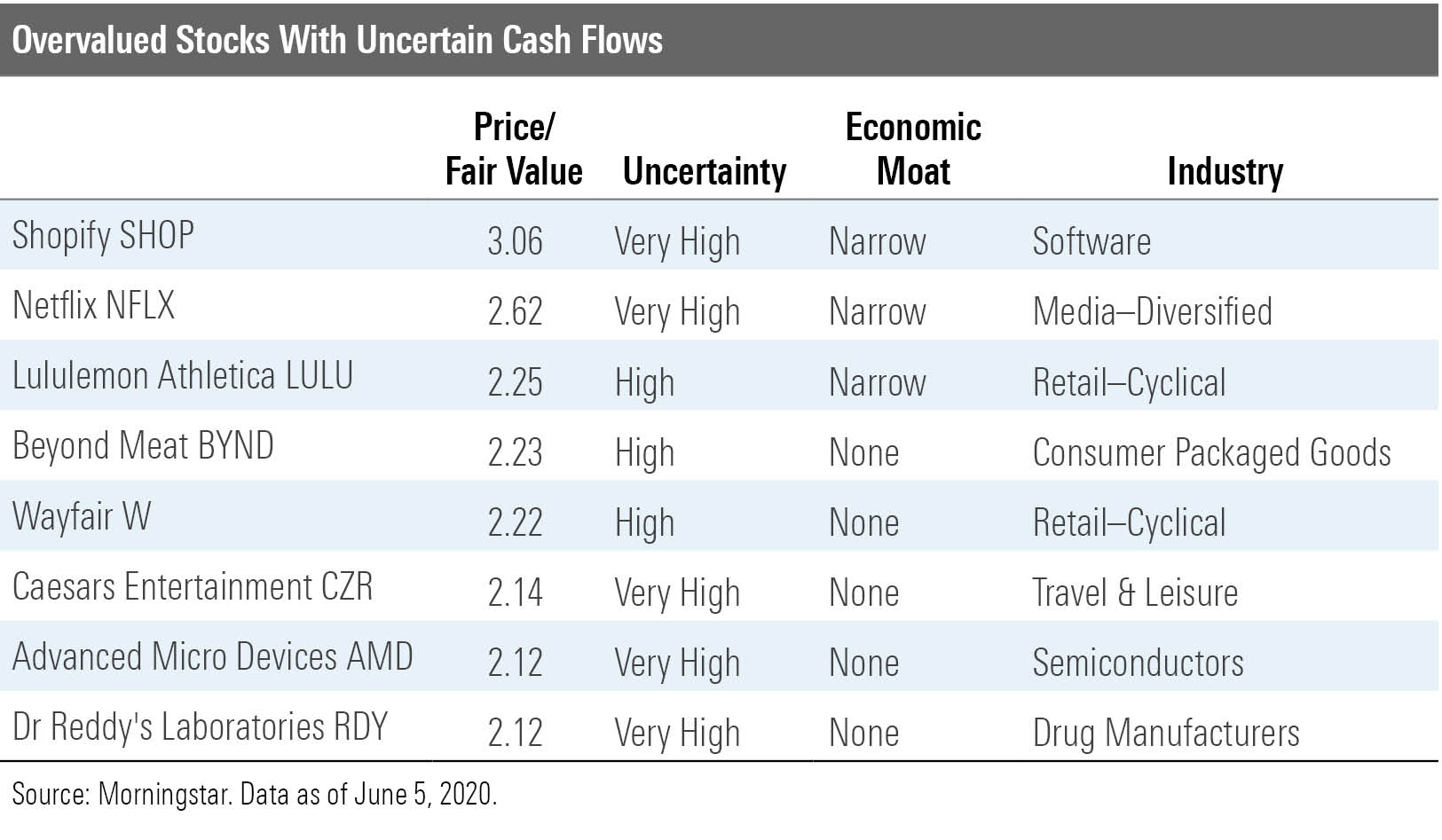

For today's screen, we're isolating stocks with high or very high fair value uncertainty ratings that are trading at least double our fair value estimates.

Before we share the results, let's step back and review what the uncertainty rating is. The uncertainty rating represents the predictability of the company's future cash flows--and, therefore, the level of certainty we have in our fair value estimate of that company. We value a company based on a detailed projection of its future cash flows, and discount those flows back to today's dollars using a proprietary cash flow model. The uncertainty rating captures a range of likely potential intrinsic values for a company based on the characteristics of the business underlying the stock, including such things as operating and financial leverage, sales sensitivity to the economy, product concentration, and other factors. If the range of potential intrinsic values is narrow, the company earns a low uncertainty rating. If the range is great, the company earns a high uncertainty rating.

Is it so bad to buy an overpriced stock with high uncertainty, given that we're not highly confident in our estimate of what that company's shares are really worth? Certainly, one might argue that in the case of a high-uncertainty stock, valuation could be tossed aside and one should instead focus on something else--growth prospects, for example. Given the lack of cash flow predictability, we could be underestimating the value of these names.

However, we could be overestimating their value, too.

That's why we err on the side of conservatism: We suggest that investors avoid richly priced, high-uncertainty names. If one is truly tempted to take on the uncertainty, we'd recommend doing so with only a significant margin of safety--even if that fair value is, in itself, uncertain.

Eight overpriced, high-uncertainty stocks passed our screen.

Here's a closer look at the valuations and uncertainty ratings for three of the names on the list.

Shopify SHOP The priciest name on the list--trading at 3 times our fair value estimate--Shopify has developed a one-stop platform for small to midsize merchants focusing largely on e-commerce. We think the firm has carved out a narrow Morningstar Economic Moat Rating thanks to two sources--switching costs and a network effect, notes analyst Dan Romanoff.

"We forecast robust top-line growth benefiting from e-commerce trends over the next several years but still decelerating over time," he explains.

We assign Shopify a very high fair value uncertainty rating. The small- to midsize businesses that Shopify caters to generate a higher degree of churn than larger merchants--not surprising, given the failure rate for new businesses. Moreover, we think Shopify is more vulnerable to a recession than its peers focusing on larger businesses. Lastly, Salesforce CRM and Adobe ADBE are formidable competitors to Shopify as the latter moves up-market.

"The company generally trades at high multiples relative to peers," observes Romanoff. "While the company is expected to produce revenue growth at the high end of peers and the premium may be justified, higher absolute valuation levels offer less room for missteps and therefore carry greater inherent risks."

Beyond Meat BYND A pioneer in the plant-based meat market, Beyond Meat faces an increasingly large field of competitors, including the likes of Conagra CAG, Nestle NSRGY, Hormel HRL, and Tyson TSN, among others. We don't currently assign Beyond Meat an economic moat.

"Given the rapidly changing marketplace, we think it is too early to tell if Beyond's first-mover advantage will result in a sustained market leadership position," explains analyst Rebecca Scheuneman. "Until we have better visibility on the strength and durability of its brand, we don't assign Beyond a moat."

We assign a high uncertainty rating to our $60 fair value estimate; shares were trading at about $134 as of June 5, 2020.

"The biggest uncertainty facing Beyond Meat is the difficulty in predicting the future demand of the product, which could be skewed by whether consumers continue to shift away from products with long ingredients lists and/or become increasingly focused on health benefits, as Beyond's beef products have the same amount of calories and saturated fat as 85% lean beef and 5 times more sodium," asserts Scheuneman. Moreover, the firm could struggle if it's unable to meet any uptick in demand, particularly if it secures a significant deal with McDonald's, she adds.

Advanced Micro Devices AMD The microprocessor producer has many new products in the early stages of launch, which will allow it to grab market share from competitors Intel INTC and Nvidia NVDA. Although we raised our fair value estimate to $25 from $19 several weeks ago, we think shares are significantly overvalued today, trading around $53.

"We continue to believe market expectations for AMD's share gains are too high, as we do not believe they fully incorporate the competitive responses from Intel and Nvidia," argues sector strategist Abhinav Davuluri.

Indeed, we think Advanced Micro Devices is at a considerable disadvantage in terms of scale.

"Both peers are able to heavily outspend AMD in research and development, leading to further propagation of market share dominance over AMD," explains Davuluri. "The cyclical nature of the semiconductor industry, coupled with AMD's weaker competitive positioning, makes AMD an inherently risky investment despite recent product launches that are on a more level playing field."

We peg a very high uncertainty rating on the firm.

"Any misstep could lead to the possibility that AMD will be unable to meet its debt obligations," concludes Davuluri.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/RNODFET5RVBMBKRZTQFUBVXUEU.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LJHOT24AYJCHBNGUQ67KUYGHEE.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/35408bfa-dc38-4ae5-81e8-b11e52d70005.jpg)