28 Undervalued Stocks

Though the market is slightly overvalued, our analysts are finding pockets of opportunity.

/s3.amazonaws.com/arc-authors/morningstar/35408bfa-dc38-4ae5-81e8-b11e52d70005.jpg)

Despite tepid performance during the first six months of the year, the Morningstar Global Markets Index was up more than 4% for the year to date through September, thanks largely to a decent third-quarter showing. Our equity coverage universe of about 1,500 stocks ended the quarter slightly overvalued, trading at a 4.5% premium to fair value on a capitalization-weighted basis.

On a sector level, communications services looks cheap, trading at a 13% discount, notes Morningstar director of North American equity research Dan Rohr in his quarterly wrap. Meanwhile, technology and healthcare now rank among the priciest sectors, trading at 8.0% and 6.4% premiums, respectively.

Here are our analysts' takes on the themes dominating their sectors and the best opportunities they see today.

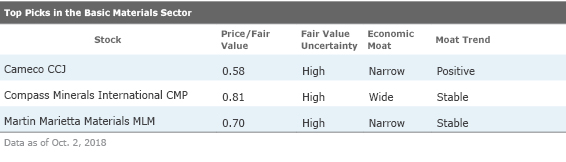

Basic Materials Basic materials stocks, as a group, remains pricey. We're especially bearish on most metals and mining companies, where a structural change in demand growth from China will have a negative impact. We forecast gold prices to hug $1,200 per ounce by the end of 2018, and rise to $1,300 per ounce by 2020.

Meanwhile, solid global demand for potash should support prices in 2018, and we've boosted our 2019 potash price forecast to $300 per metric ton, up from $270 per metric ton this year. And while construction softened meaningfully last quarter and lumber and panel prices stumbled, our long-term outlook for housing remains comparatively bullish.

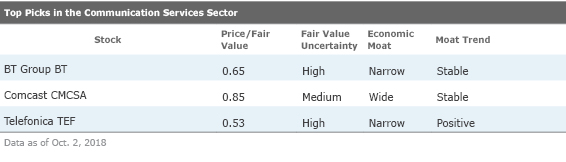

Communication Services With a market-cap-weighted price/fair value of 0.87, the sector trades at the widest discount to fair value. Global telecom stocks have struggled for many reasons. For instance, rising rates in the U.S. have likely dinged the valuations of these higher-yielding stocks; the industry isn't delivering meaningful growth, either.

In the U.S., the proposed merger of

Consumer Cyclical

The consumer cyclical sector is trading at a 5% premium to our fair value estimate, thanks to healthy consumer sentiment, low unemployment, and stable asset market valuations. Disruption from e-commerce giant

Travel and leisure companies continue to increase their take of consumer dollars: As consumers migrate to experiences over things, cruising and lodging companies stand to benefit. Other consumer product companies willing to invest in convenience, ease of use, and experience continue to nab market-share gains.

Consumer Defensive

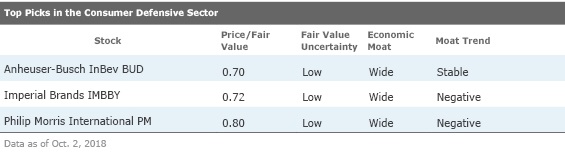

The sector is trading at just a 2% discount to our fair value estimates on a market-cap-weighted basis, versus a 5% discount three months ago. M&A activity has been robust, as leading players try to compensate for sluggish organic growth.

Consumer product manufacturers are working to increase e-commerce penetration. While e-commerce sales are just a fraction of revenue today, we expect online consumer product sales to account for a mid- to high-single-digit percentage of the market over the next five years.

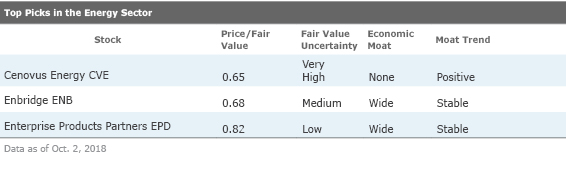

Energy Crude oil fundamentals continue to look healthy. However, we continue to think that the market is underestimating the capacity of the shale industry to eventually push oil markets back into oversupply. Our midcycle forecast for WTI is still $55/bbl.

Despite our bearish outlook for long-term oil prices, we see pockets of opportunity in the sector, which is trading at an average price to fair value estimate of 0.99. Those industries less dependent on the price of oil are more attractive to us than those with higher oil price betas.

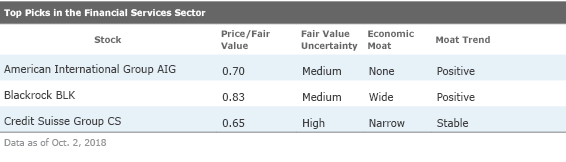

Financial Services The global financial-services sector is trading at a slight 4% discount to what we think the sector is worth. Despite an overall strong economy, increased competition among banks is slowing net interest margin growth, and credit cost uncertainty is on the rise.

The investment services industry in the United States is seeing a pickup in strategic activity; there's a general easing of financial regulations in the U.S., too. But there are signs of tightening in other regions, including China, Australia, and Europe.

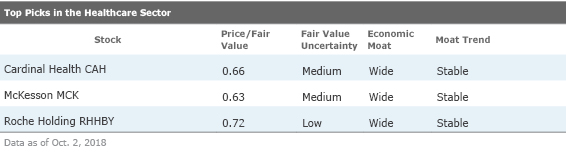

Healthcare Healthcare valuations have risen quite a bit: The sector is trading at a 7% premium to our fair value estimate, up from a 2% discount to fair value as of the end of the second quarter. Drug pricing concerns appear to be easing, and innovative new drug launches and rich drug pipelines support a steady growth outlook for the drug and biotech industries.

Corporate restricting and redeployment of capital are key strategic decisions within the industry, as firms divest noncore assets and use their strong cash flows for acquisitions.

Industrials The industrials sector remains slightly overvalued, at a 4% premium to our fair value estimate. Interest in industrial automation and autonomous vehicles persisted during the quarter. Compelling automation and autonomous vehicle technologies are likely to foster new company formation and M&A.

The Internet of Things is also making strides in the sector, increasing the prospects of margin expansion. As early adopters of this technology, industrials stand to disproportionately benefit.

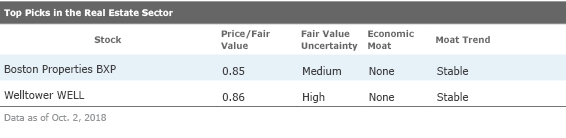

Real Estate The real estate sector is trading at market-cap-weighted price/fair value of 0.98, suggesting it's slightly undervalued. Underlying performance in the sector remains healthy overall. Real estate investment trusts have been focused on repositioning and strengthening their portfolios, deleveraging, and capital recycling.

Construction of new properties continues, though supply may have peaked in some markets and sectors. Rising construction costs may lead to slowing supply growth over the next several years. And lingering concerns about increasing bond yields associated with future rate hikes remains.

Technology

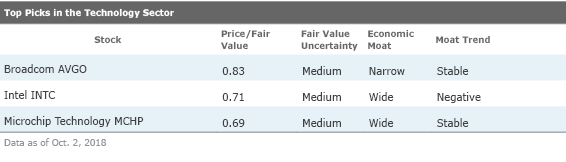

The technology sector is overvalued by 7.5%. Enterprise cloud computing is the most important story in the sector. The shift has ramifications for dozens of stocks we cover. Software-as-a-service vendors are enjoying significant growth while legacy IT vendors face ongoing headwinds. The companies that have been adept at transitioning to the new model--including

M&A activity remains a key theme in the sector, with deals continuing among semiconductors and software companies, in particular. However, the U.S.-China trade war continues to add an element of uncertainty to the sector.

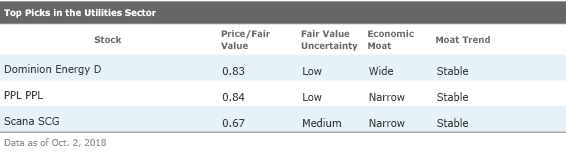

Utilities On a global basis, the sector is trading in line with our fair values estimates. Higher-quality names, however, are trading at 15% to 20% premiums. As long as energy prices remain stable, we expect 5% to 7% annual earnings and dividend growth across the sector during the next few years.

Most of the utilities we cover continue to invest heavily in infrastructure, ranging from renewable energy to local energy distribution. M&A has slowed in 2018 after a heated 2015-17 period, as the worldwide pool of midsize utilities that would be good targets shrinks. And hurricanes, wildfires and the Boston-area pipeline explosion illustrate the unplanned operational risks inherent in this sector.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/RNODFET5RVBMBKRZTQFUBVXUEU.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LJHOT24AYJCHBNGUQ67KUYGHEE.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/35408bfa-dc38-4ae5-81e8-b11e52d70005.jpg)