Protecting a Client's Portfolio From Drawdowns

The road ahead could be rocky, but investors still must accept some risk in order to meet their goals.

This is the first in a series of four articles collected from Morningstar Investment Management's 2022 outlook, highlighting the most important issues facing investors in the coming year. Matt Wacher is the group's CIO for Asia-Pacific.

Investing is all about taking risk. To achieve our investment objectives and enable investors to meet their goals, we need to assess the investment environment and take what we deem to be appropriate risks. Sometimes the opportunity set will be rich, and we will be able to build robust portfolios that should comfortably meet an investor's investment objectives. Other times, that's not the case. Our analysis hints that the path ahead could be a little rocky at times, but we must accept some risk to achieve goals.

Risk Is the Price You Pay for Good Returns

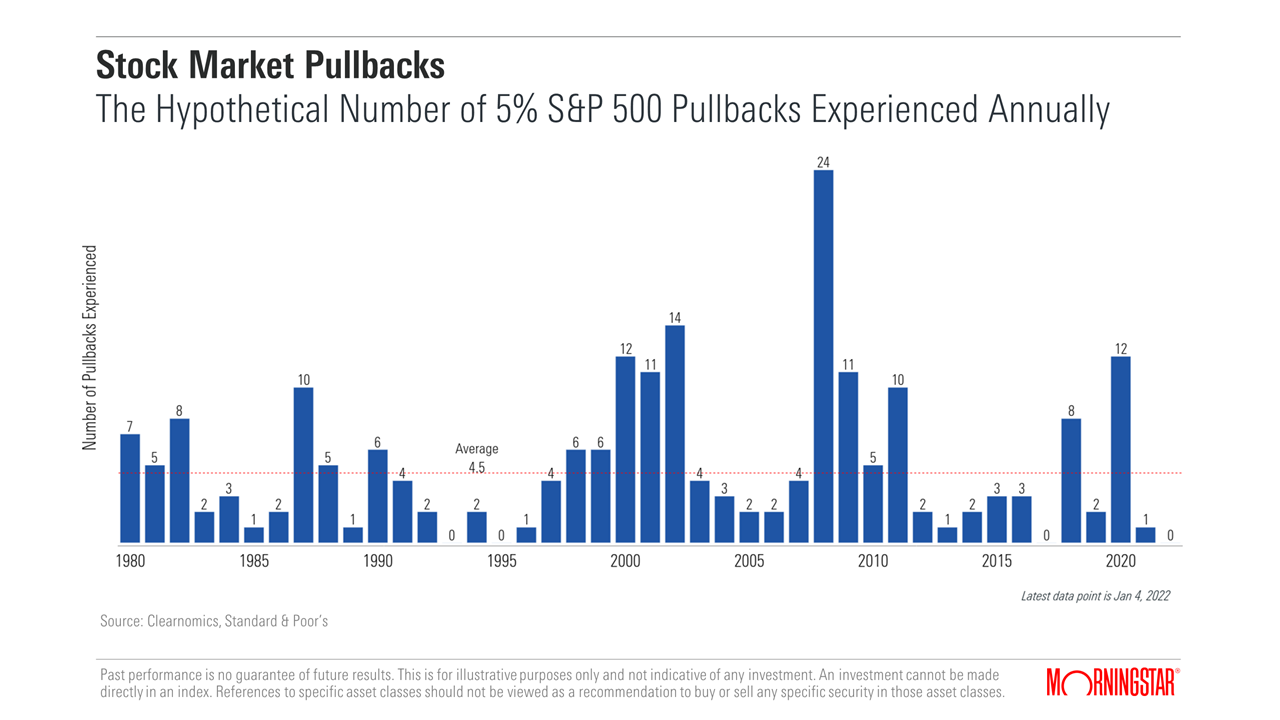

Calling drawdowns good or bad is somewhat flippant. Of course, no drawdown is good for an investor. This is especially the case for investors with shorter time horizons.

In fact, risk aversion can be a rational response, as people often fail to appreciate the danger of negative compounding. The common message is that compounding is a beautiful thing; however, it is more powerful on the downside than the upside. Consider various scenarios. If the market were to sell off by 20% tomorrow, you need to make 25% to get back to square. If it falls by 50%, you need to earn 100%. Avoiding losses matters because losing less means you require less to bounce back.

That said, failing to take calculated risks is a risk itself. Or, said simply: We must ensure that we take enough risk to meet our objectives. This side of the coin is just as important, as goal attainment is the key reason most people invest. This is also the main focus of our investment approach: We need to ensure we are being rewarded for the risks we take.

Tomorrow vs. Yesterday

In the past decade, it has been a relatively simple task to invest in a very risk-focused way and still achieve healthy returns above the inflation rate.[1] Even in the extreme market event of March 2020, we were afforded the opportunity to buy assets at prices that could deliver exceptional long-term returns, enabling us to be confident that we could deliver on our promises to investors.

However, the opportunity set has clearly narrowed. Equity markets have become more expensive on almost every measure, with some parts of the market moving to what we'd consider quite extreme levels. The same can be said for traditionally defensive assets, with bonds trading at levels that could lead to significant capital losses, especially with economic growth remaining a tailwind and inflation at levels not seen for many years.

Faced with these risks, the key is to assess a portfolio relative to the corresponding goals and risk tolerance of the investor, while also acknowledging the investing environment that we operate in. Regarding the investment environment, we foresee a wide range of potential outcomes, expecting the next year (and decade) to look quite different from the last.

This is both an opportunity and a threat: It presents an opportunity for us to add value for investors by navigating the series of setbacks ahead, but it'll require a different approach from that taken over the past decade. We are heading into a time when broad market exposure (passive investing) could easily fall short of historical averages and may fail to meet absolute return objectives, making it difficult for investors to achieve their goals. In this sense, we don't expect an easy ride for the average investor.

Defending in a Low-Interest-Rate Environment

Perhaps the biggest dilemma for risk-sensitive investors resides in traditional fixed income. Holdings in defensive assets such as bonds offer poor return prospects, in our analysis, creating a true challenge for risk management.

We don't paint with a broad brush here and are still selectively investing in pockets of the bond market for their defensive characteristics and/or return potential. However, many fixed-income markets are expensive (especially so in corporate high-yield bonds, where we carry an underweight position). This is quite different from the past 30 years, where bonds have played the dual role of return generator and diversifier in portfolios. We are therefore balancing what is left of bonds' defensive characteristics against low absolute yields while also looking for more defensive characteristics from the growth holdings in our portfolios.

The Goal Must Still Be to Avoid Permanent Loss of Capital

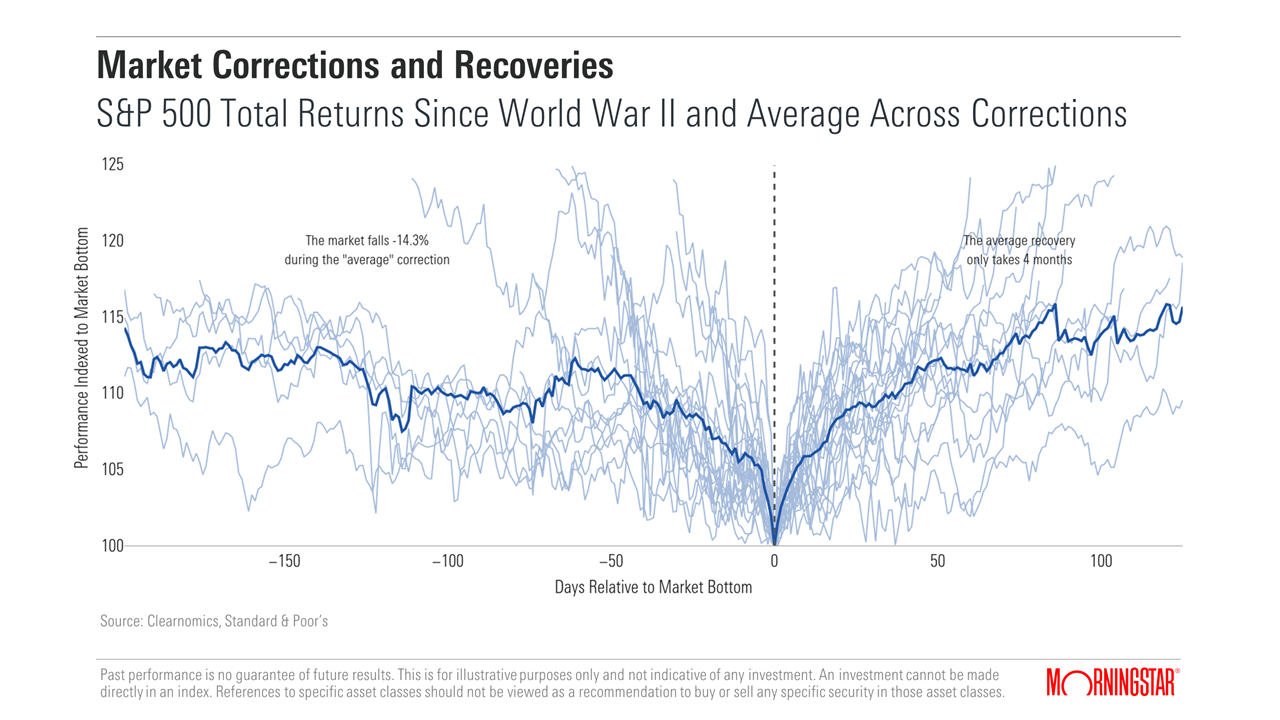

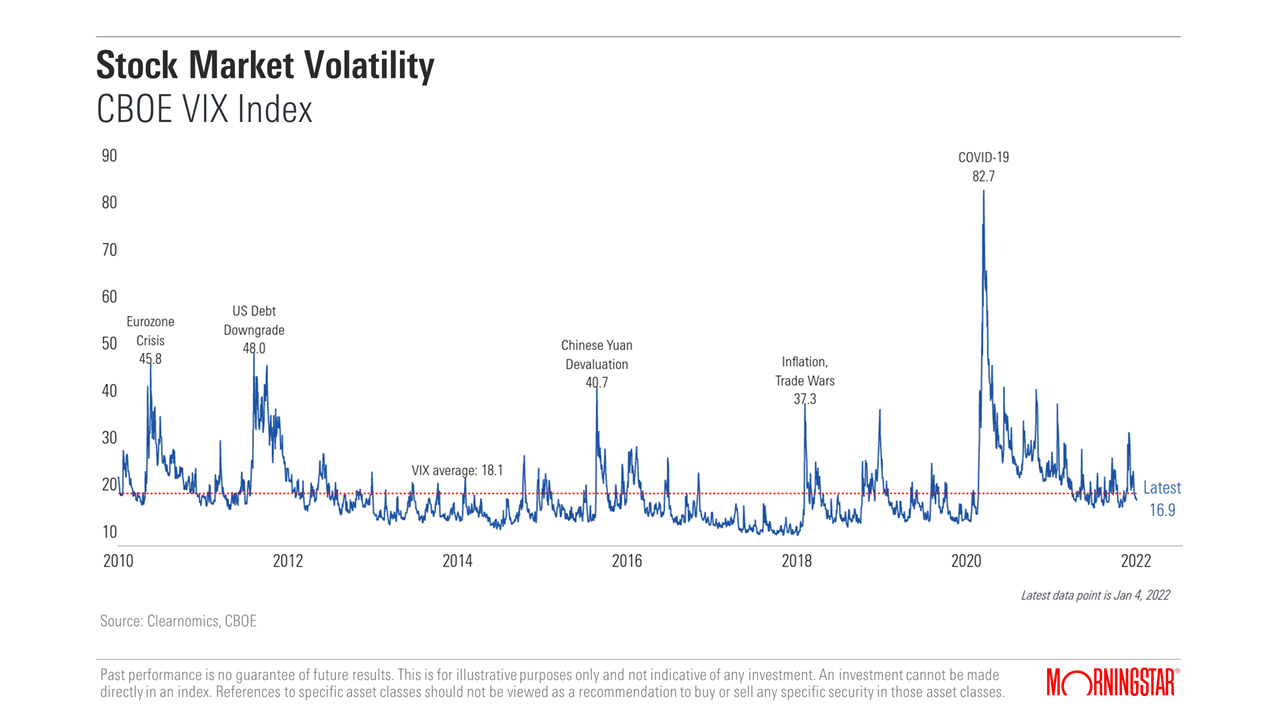

Importantly, not all drawdowns are equal. Volatility provides investment opportunities--the ability to get in assets with significant upside. As investing great Bill Miller says, "volatility is the price you pay for returns," and accepting volatility will be necessary for most investors. The way we approach risk is to consider the potential for two types of drawdowns: 1) valuation-induced drawdowns, and 2) volatility-induced drawdowns. We embrace volatility, within reason, but want to avoid valuation-induced sell-offs.

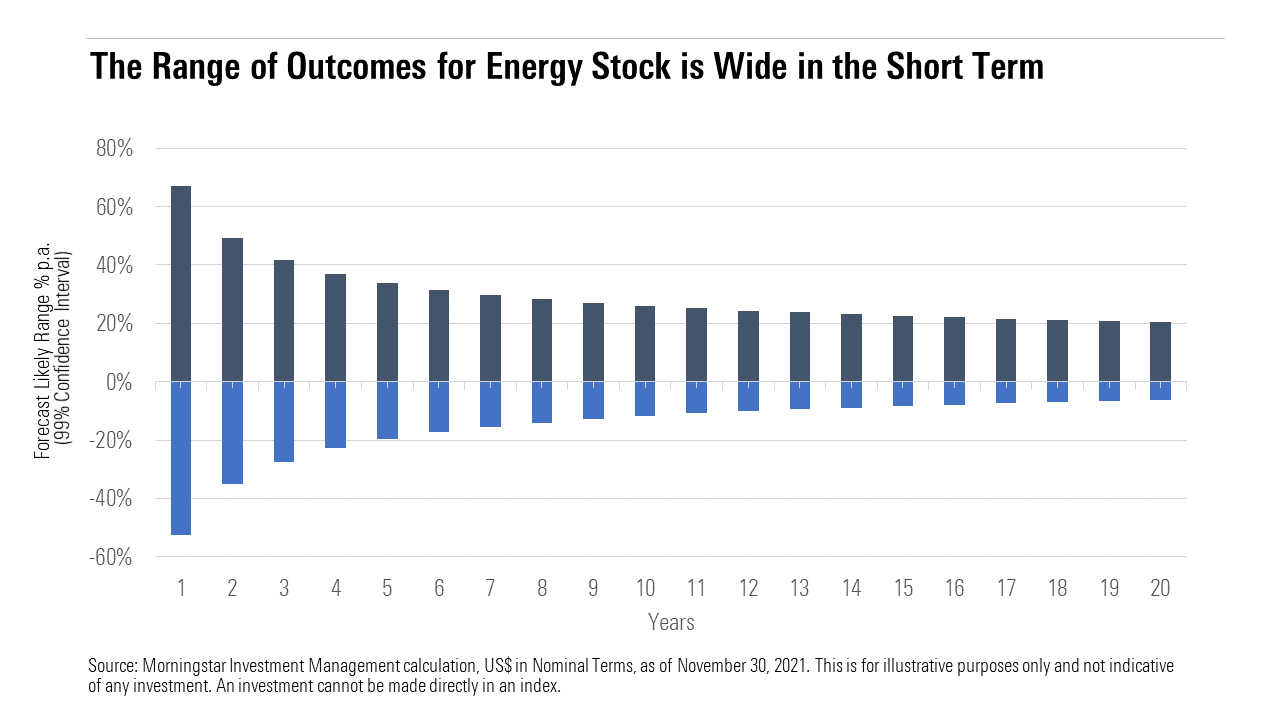

When you look at the exposure in our multi-asset portfolios, this difference between volatility and valuation becomes evident. We have a decent tolerance for holding assets with economically sensitive cash flows, even if these assets tend to have higher core volatility. Our exposure to energy stocks is a good example. They present reasonably high core volatility, but that can usually be recouped with time. See the chart below for the volatility of the global energy sector, where the range of outcomes really starts to skew to the upside over long time frames--this is a "good" volatility trade-off, in our view.

Valuation-based drawdowns (paying too much for an asset) can be more enduring and may not be fully recouped, even over the long term. Equities that go bankrupt or bonds that default are extreme examples. Our process seeks to avoid drawdowns that can permanently impair capital.

So, how can an investor both protect and earn? We believe the best pathway is to identify the assets with the greatest risk/reward profiles and size them appropriately to manage total portfolio risk. Today, the most attractive holdings are concentrated in cyclical areas of the market, despite their higher volatility, so we employ portfolio construction techniques to offset or temper the cyclical risk, including defensive sector exposures.

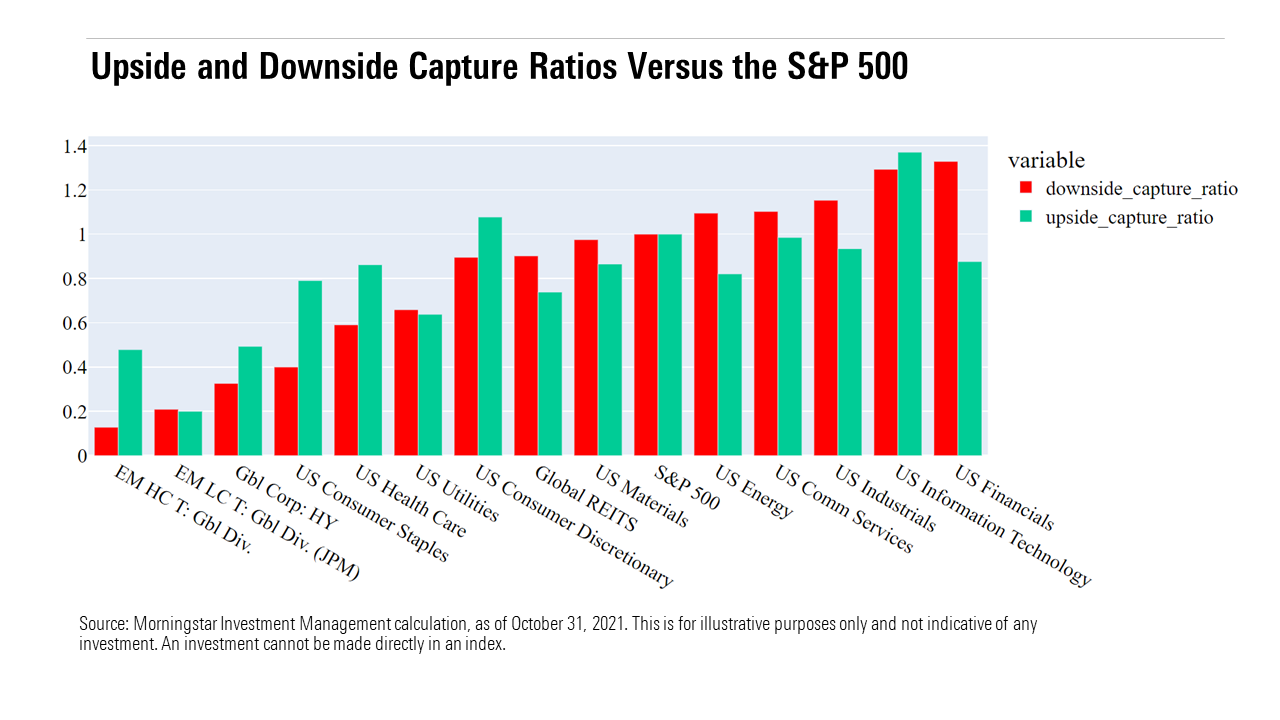

Our analysis has shown some of the most attractive assets include emerging-markets debt, consumer staples stocks, and healthcare. These are all attractive as replacements for growth assets in an array of different environments that we might face, especially where the opportunity set is diminished and the potential for a risk event is elevated. Our recent analysis shows that each of the asset classes named above has inviting downside- and upside-capture ratios against the S&P 500, presenting a particularly attractive asymmetry between the two in the significant market scenarios we have run.[2]

Somewhat counterintuitively, it is therefore likely that average "through-the-cycle" portfolio growth exposure ought to be higher than past decade--to the point where it may make sense to gain exposure to more volatile assets to achieve investment objectives. This is a good example of using smart diversification techniques, smoothing the ride via carefully selected growth holdings instead of relying on expensive traditional defensive exposures. Still, there is a potential for more volatility in portfolio returns and temporary drawdowns are there.

Currency exposure is another available tool that may be highly underrated by many investors. For example, the U.S. dollar and the Japanese yen tend to behave as so-called "safe-haven" currencies in periods of broad market stress. By allocating smartly across the currency universe, we can lean on the protective characteristics of the dollar and the yen where it makes sense to do so and have recently boosted this exposure.

Key Takeaways for Risk Management

The hardest, yet most effective, approach when protecting against loss is to distinguish between volatility-induced setbacks and valuation-induced losses. Periods of volatility will come and go; they are scary at the time but rarely impact goal attainment.

As advocates of great investing, we must collectively resist impulsive actions and understand that the road won't be straight. Accepting some volatility is a prerequisite for good returns in any market, but today's market arguably requires greater care than usual. In our view, this necessitates us to target the best assets to protect and earn, with careful sizing and smart diversification.

A final thought on downside protection: We should be happy to forego some of the gains in strong upward markets, acknowledging that we won't participate in losses to the same extent as others if we maintain a risk-focused approach. Ideally, if we can limit losses by investing in a risk-focused way, we are less likely to trigger an irrational response from investors, meaning we are more likely to help them stay invested, giving them a better chance of achieving their goals over time.

[1] In our own research, using Australian data, over the past 10 years a typical 60/40 portfolio (60% in stocks and 40% in bonds) achieved a return of at least the Consumer Price Index plus 3.5% during 96% of rolling three-year periods since the start of 2010, well above the 62% of rolling three-year returns if we take the analysis back to 1970.

[2] Emerging-markets debt presents not just inversely related downside capture (positive return when the S&P is negative) but also surprisingly large upside capture. Similarly, U.S. consumer staples stocks and healthcare stocks both show low downside captures (consumer staples nearly as low as the fixed-income asset classes) while ranking among the top upside captures.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/MNPB4CP64NCNLA3MTELE3ISLRY.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/SIEYCNPDTNDRTJFNF6DJZ32HOI.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZHTKX3QAYCHPXKWRA6SEOUGCK4.png)