Experts Forecast Stock and Bond Returns: 2024 Edition

Bond outlooks improve, but stocks’ prospects drop on the heels of 2023′s rally.

/s3.amazonaws.com/arc-authors/morningstar/66112c3a-1edc-4f2a-ad8e-317f22d64dd3.jpg)

/s3.amazonaws.com/arc-authors/morningstar/96c6c90b-a081-4567-8cc7-ba1a8af090d1.jpg)

Better things lie ahead for bonds, but the prospects for stocks, especially U.S. equities, are less rosy.

Those were the recurring themes among the capital markets assumptions provided by major investment firms as 2023 wound down.

In contrast with the major firms’ capital markets assumptions released toward the end of 2022, when declining equity prices and higher interest rates buoyed the prospects for both stocks and bonds, the 2023 equity market rally diminished most firms’ return assumptions for U.S. stocks. Meanwhile, last year’s continued interest-rate hikes have contributed to higher forward-looking return prospects for bonds and cash. And firms’ outlooks for non-U.S. stocks, a persistent bright spot in my annual compendium, continued to be more robust than their expectations for companies domiciled stateside, thanks largely to foreign stocks’ valuation advantage.

How to Use the Forecasts

Although it’s reasonable to be skeptical about predicting the market’s direction, especially over the short term, the fact is that you need to have some type of return expectation in mind when you’re creating a financial plan. If you can’t plug in a long-term return assumption, it’s tough to figure out how much to save and what sort of withdrawal rate to use once you retire. Long-term historical returns are one option. But at certain points in time—like 2000 or early 2022—they might lead to overly rosy planning assumptions, which in turn might lead you to save too little or overspend in retirement.

To draw some conclusions about what sorts of return assumptions might be reasonable for planning, I have been amalgamating investment firms’ capital markets assumptions at least once a year. Firms use different methodologies to arrive at their capital markets assumptions, but most employ some combination of current dividend yields, valuation, and earnings-growth expectations to guide their equity forecasts. Fixed-income return assumptions are more straightforward given the tight historical correlation between starting yields and returns over the next decade. That explains why you see more uniformity among firms’ fixed-income return expectations, with variations driven largely by time-period differences.

Before you take these or any other return forecasts and run with them, it’s important to bear in mind that these return estimates are more intermediate-term than they are long-term. The firms I’ve included below all prepare capital markets forecasts for the next seven to 10 years, not the next 30. (BlackRock and Vanguard do provide 30-year forecasts as well as 10-year, and Fidelity’s capital markets assumptions apply to a 20-year horizon. But they’re outliers in terms of making such far-reaching forecasts available to the public.) As such, these forecasts will have the most relevance for investors whose time horizons are in that ballpark, or for new retirees who face sequence-of-return risk in the next decade.

It’s also important to note that the parameters for these return estimates vary a bit; some of the return expectations are inflation-adjusted, while others are not.

Expert Forecasts for Long-Term Asset-Class Returns

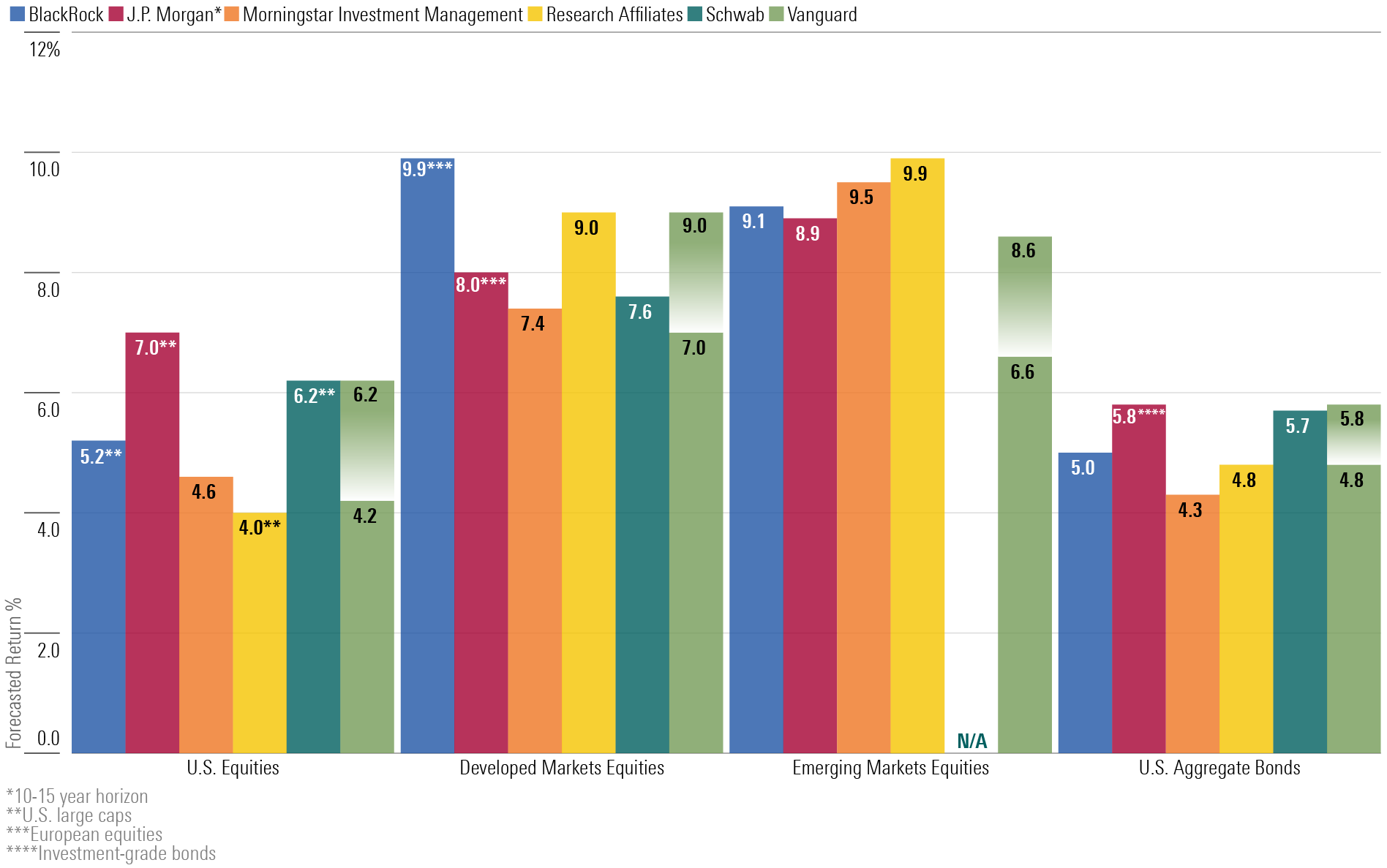

BlackRock

Highlights: 5.2% 10-year expected nominal return for U.S. large-cap equities; 9.9% for European equities; 9.1% for emerging-markets equities; 5.0% for U.S. aggregate bonds (as of September 2023). All return assumptions are nominal (non-inflation-adjusted).

BlackRock’s equity return expectations in September 2023 were quite a bit lower than they were the year prior. For example, the firm was expecting a nearly 9% 10-year return for U.S. equities in September 2022 but just over 5% a year later. The firm’s return assumptions for non-U.S. stocks have also come down since last year but are still notably higher than its U.S. equity return assumptions: nearly 10% for European equities and 9% for emerging-markets equities.

In line with 2023′s rising yields, the firm’s outlook for bond returns increased from 2022. BlackRock’s models call for a 5.0% expected 10-year return from U.S. aggregate bonds versus 4.2% in 2022 and less than 2.0% in 2021.

Fidelity

Fidelity’s capital markets assumptions employ a 20-year horizon (2023-42) and therefore can’t be stacked up neatly against the 10-year returns from other firms in our survey. In addition, the firm states its capital markets assumptions in real (inflation-adjusted) terms; its 2024 base-case inflation rate over the 20-year horizon is 2.7%. Finally, the firm’s assumptions are based on data as of April 30, 2023, so they don’t factor in stocks’ strong gains in the last eight months of 2023.

The firm is forecasting a 3.9% real return for U.S. equities over the next 20 years. That’s higher than Fidelity’s 20-year real return forecast of 3.0% for U.S. stocks last year, but substantially lower than U.S. stocks’ actual real returns of 7.3% since 2003. Fidelity cites elevated equity valuations (again, as of April 2023) as the main constraint on U.S. equity gains relative to their gains over the past 20 years. The firm expects the 20-year real returns on non-U.S. stocks to be roughly in line with U.S. (3.9%), but accords substantially higher return prospects to developing markets—a 5.4% real return over the next 20 years.

On the fixed-income side, the firm was forecasting 2.1% 20-year real returns for the Bloomberg U.S. Aggregate Bond Index as of April 2023.

Grantham Mayo Van Otterloo

Highlights: Negative 2.6% real returns for U.S. large caps over the next seven years; 1.9% real returns for U.S. bonds (as of November 2023).

As one might expect from a valuation-conscious firm after a stock market rally, GMO’s return expectations for stocks generally declined over the past year. The firm is expecting negative 2.6% real returns for U.S. large caps over the next seven years, down from its negative 0.7% real (inflation-adjusted) return forecast in 2023. Consistent with previous forecasts, the firm’s outlook for non-U.S. stocks is brighter than its expectation for U.S. names: The seven-year real return forecast for international large caps is 2.3%; 4.4% for international small-caps; 4.7% for emerging-markets equities; and a whopping 6.3% for emerging-markets value stocks.

The firm’s outlook for bonds looks better than its late-2022 number: a 1.9% real return for U.S. bonds (up from 0.6% in 2022) and a 4.4% real return forecast from emerging-markets bonds.

J.P. Morgan

Highlights: 7.0% nominal returns for U.S. large-cap equities over a 10- to 15-year horizon; 4.6% nominal returns for 10-year Treasury bonds and 5.8% nominal returns for U.S. investment-grade corporate bonds over a 10- to 15-year holding period (as of Sept. 30, 2023).

J.P. Morgan’s expectation for equities’ returns over the next 10 to 15 years declined from its September 2022 numbers: Owing to higher valuations, its forecast for U.S. large caps dropped to 7.0% from 7.9% and to 7.2% from 8.1% for U.S. small caps. The firm’s outlook for non-U.S. equities generally declined, too, though its 10- to 15-year outlook for eurozone equities was a robust 8.0%, and for emerging-markets equities it was 8.9%. More broadly, its equity return projections were higher than most of the firms in our survey.

On the fixed-income side, the firm nudged up return expectations thanks largely to the higher yields on offer today: It’s expecting a 4.6% return from 10-year Treasuries, up from 4.0% last year, and 5.8% nominal returns from U.S. investment-grade corporates, up from 5.5% in late 2022. One exception is that the firm’s expectations for high-risk bond types declined slightly. The firm’s 10- to 15-year forecast for high-yield bonds is 6.5% for 2024, down from 6.8% for 2023, and its forecast for emerging-markets sovereign bonds dropped to 6.8% from 7.1%.

Morningstar Investment Management

Highlights: 4.6% 10-year nominal returns for U.S. stocks; 4.3% 10-year nominal returns for U.S. aggregate bonds (as of Dec. 31, 2023).

Following a major U.S. market rally in 2023, Morningstar Investment Management’s 10-year equity outlook dropped relative to where it was in late 2022. In line with previous years’ assumptions, MIM’s outlook for non-U.S. stocks is substantially better: 7.4% for developed-markets stocks overseas and an impressive 9.5% for emerging-markets equities.

Like most of the forecasts, MIM’s return expectations for bonds have jumped to reflect higher yields. It assumes a 4.3% 10-year nominal return for U.S. aggregate bonds and 5.3% for U.S. high yield.

Research Affiliates

Highlights: 4.0% nominal (1.5% real) returns for U.S. large caps during the next 10 years; 4.8% nominal (2.3% real) returns for U.S. aggregate bonds (as of Dec. 31, 2023; valuation-dependent model).

On the heels of U.S. stocks’ rally in 2023, Research Affiliates’ 10-year U.S. market return expectations declined, from a nearly 6% nominal return projection for U.S. large caps at the end of 2022 to just 4% at year-end 2023. In fact, the firm is expecting U.S. aggregate bonds to outperform stocks over the next decade, and its expected volatility for bonds is also substantially lower. The firm accords a return edge to small-cap stocks: a 7.2% 10-year annualized return. Consistent with past forecasts, the firm is expecting better things from non-U.S. stocks: a 9.0% 10-year annualized return (6.5% real) for developed-markets stocks outside the U.S. and 9.9% (7.4% real) for emerging-markets equities.

Schwab

Highlights: 6.2% nominal returns for U.S. large caps during the next 10 years; 5.7% nominal returns for U.S. investment-grade bonds (as of Oct. 31, 2023).

Schwab bucked the trend toward lower expected equity returns and nudged up its 10-year return expectation for U.S. stocks as of its most recent forecast, to 6.2% versus 6.1% a year ago. The firm’s outlook for non-U.S. large caps remained in line with last year’s forecast: 7.6%.

In line with the outlook from other investment providers, the firm is forecasting a 5.7% gain in 2024 for U.S. investment-grade bonds, versus 4.9% last year and 2.3% in 2022. (All figures are nominal.) Schwab’s 10-year return expectations are well below each asset class’ returns from 1970 through October 2023.

Vanguard

Highlights: Nominal median U.S. equity market return of 4.2% to 6.2% during the next decade; 4.8%–5.8% median expected return for U.S. fixed income (as of Sept. 30, 2023).

Vanguard’s latest U.S. equity market return forecast is a touch below where it was a year ago. (The firm presents its forecasts in a range.) The new forecast calls for U.S. equity gains of 4.2% to 6.2% over the next decade, versus 4.7% to 6.7% a year ago. Its non-U.S. equity return forecast (7.0%–9.0%) is roughly unchanged and substantially higher than the U.S. return expectation. Vanguard provides sub-asset-class forecasts, too. In its most recent run, its 10-year return forecast for value stocks (4.8%–6.8%) was substantially higher than its outlook for growth names (1.2%–3.2%). The firm is also expecting small-cap stocks to best large caps: The range for the former was 4.9% to 6.9%, versus 4.2% to 6.2% for the latter.

Vanguard’s return expectations for U.S. aggregate bonds are roughly the same as they were a year ago. The firm is expecting better returns—albeit with higher volatility—from lower-quality bonds: a range of 6.3% to 7.3% for U.S. high-yield bonds and 6.4% to 7.4% for emerging-markets bonds.

Where to Find Stocks to Buy in 2024

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/6ZMXY4RCRNEADPDWYQVTTWALWM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/URSWZ2VN4JCXXALUUYEFYMOBIE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/CGEMAKSOGVCKBCSH32YM7X5FWI.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/66112c3a-1edc-4f2a-ad8e-317f22d64dd3.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/96c6c90b-a081-4567-8cc7-ba1a8af090d1.jpg)