Retirees Aren’t the Only Ones Who Face Sequence Risk

The order of investment returns matters for workers, too.

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

Real Life

Sequence risk—that is, the possibility that investor results could be harmed by the order in which those returns occurred—does not affect lump-sum purchases. Invest $10,000, sleep for 20 years, and your wealth upon awakening (assuming no ongoing account fees) will be (1+g) to the power of 20 * $10,000, with g representing the security’s annualized total return. How g was achieved is immaterial.

The lump-sum calculation works for Rip Van Winkle’s retirement portfolio. It does not suffice for actual workers, though. They invest not in one fell swoop, but instead in dribs and drabs, spread over decades. In such cases, as I was reminded when reading the draft for my friend Bill Bernstein’s splendid update (to be published in February) to his already splendid book, The Four Pillars of Investing: Lessons for Building a Winning Portfolio, sequence risk very much does exist.

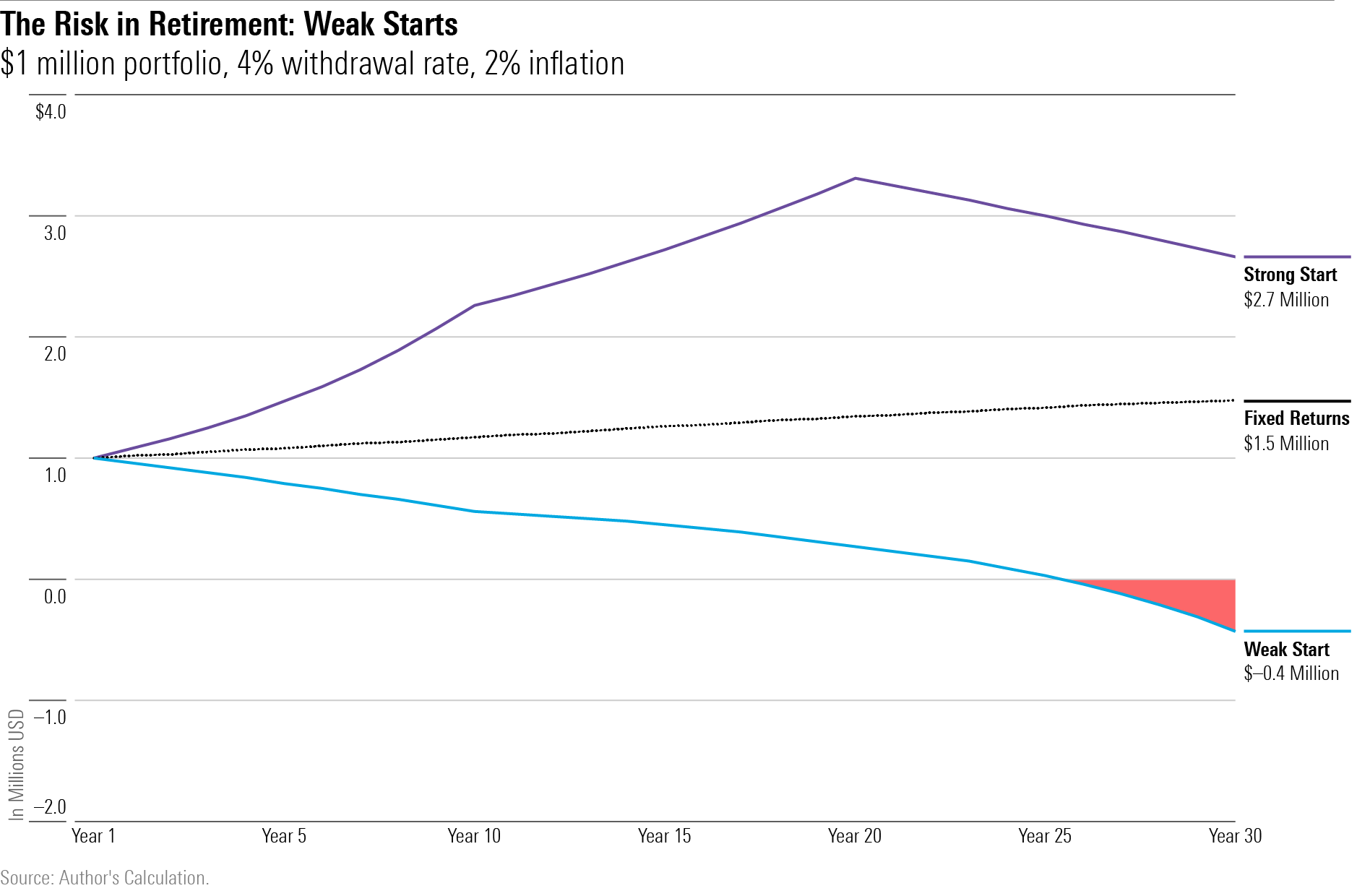

Recap: Retirees

To demonstrate that claim, I will reuse the model used for this past Friday’s column. That article compared the outcomes for three retirees who obtained identical annualized returns, but in different orders. The first investor gained 12% annually for the first decade of retirement, 6% for the next decade, and nothing for the final decade. The second investor received the reverse, treading water for the initial 10 years, then making 6%, then concluding with 12% gains. The third investor received the same long-term return as the first two—which computes to an annualized 5.89%, rather than the intuitive 6%—but as a fixed rate.

In short, the three retirees each received the same “g,” but while taking different paths. Below lies the highly divergent fates of their portfolios, assuming that each investor retired with $1 million, withdrew $40,000 from that portfolio during her first year of retirement, then increased her expenditure by 2% annually.

Sequence risk was huge. A second important lesson from the column was that retirees do not necessarily profit from reduced volatility. It is commonly believed that if retirees could own bonds that gain as much as stocks, they should do so, because the less volatility they suffer the better. But if a portfolio’s strong performance comes early during retirement, and the weak performance late, then stocks beat bonds, even if their long-term returns match.

Sequence Risk During Accumulation

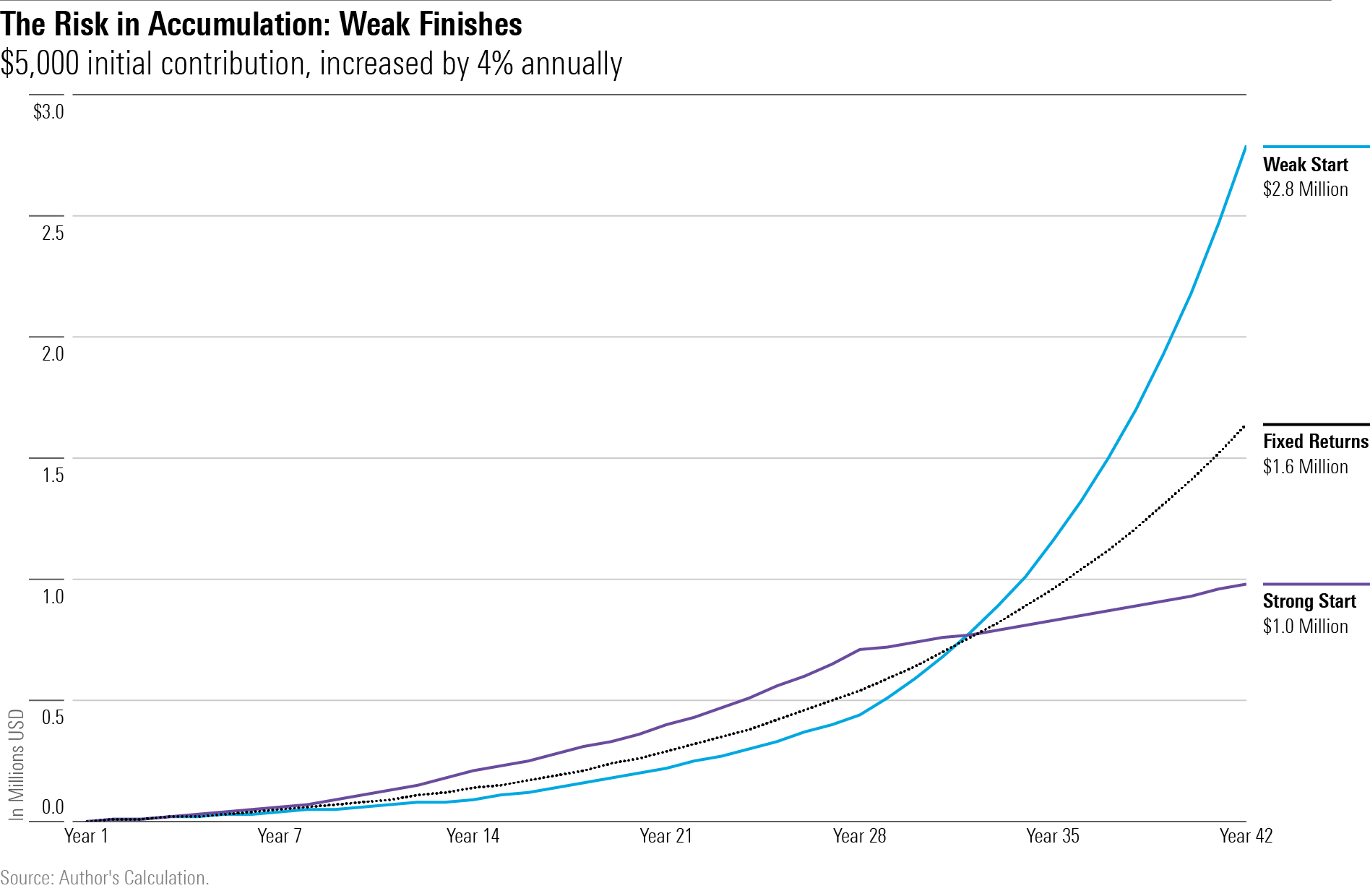

Now we will consider workers. This time, the model addresses three investors who are 22 years old, have just began their first jobs, and are relatively thrifty, placing $5,000 into tax-sheltered accounts during their first working year. Henceforth, they will raise their savings rate by 4% annually. That makes for a $24,965 contribution in Year 42. Following that, they will retire, at age 65.

Once again, the three investors earn identical annualized returns, and once again the sequences are reversed for the first two investors, while the third earns a fixed rate. The first worker begins strongly with 12% gains during the first 14 years of her career, followed by 6% through the middle stretch, and then breaking even during the final 14 years. The second worker starts poorly, earning nothing for 14 years. She then gains 6% for 14 years, before finishing with 12% increases. Meanwhile, the third worker trudges along, pocketing 5.89% each and every year.

The story remains the same. As with the retirees’ portfolios, the sequence of returns experienced by the workers powerfully influenced their results. One investor easily outpaced the worker who held the fixed-rate portfolio, while the other trailed badly. This time, though, the standings were inverted. The winner was the investor who began slowly and finished with a flourish. The loser was the investor holding the portfolio that started well but later fizzled.

While retirees and workers are each affected by sequence risk, their mechanisms are dissimilar. Strong early returns benefit retirees by reducing the demands on their portfolios. By Year 10, the retiree who enjoyed 12% returns coming out of the gate had cut her withdrawal rate by 1.7 percentage points, from the initial 4% to 2.3%. Her worries were over. Ten years into her retirement, her salient question had switched, from “Will I be able to pay my bills?” to “How large will be my legacy?”

Conversely, large initial returns are not particularly useful for workers, because they have yet to invest most of their assets. Of course, all things being equal, investment gains beat investment losses. But all things are not necessarily equal. If the high early returns lead to steep equity valuations that eventually stall the stock market, causing it to stagnate as corporate earnings “catch up” with equity prices, then that bull market did younger investors no favor whatsoever. They would been better off suffering early, then prospering late.

Lessons

Retirees address sequence risk by being flexible. If their investments are initially successful, they can follow their established plans—or, perhaps, even increase their spending. If, on the other hand, their portfolios languish during the early years of retirement, they may need to adapt. Possible changes include lowering the withdrawal rate; maintaining that rate but forgoing the inflation adjustment; and reducing spending.

Regrettably, workers have fewer tools with which to combat sequence risk. Critics of target-date funds complain that the short-dated funds are too aggressive. They recommend that such funds hold fewer stocks to lock in shareholder gains. But that decision cuts both ways. Consider, for example, a worker who started a 401(k) plan in the 1980s, received fine returns on a smallish portfolio in the ‘90s, and then booked no profits for another 10 years as equities languished. Her retirement fortune relied upon capturing the stock market’s subsequent rebound.

(In this article’s second chart, the winning portfolio trails the fixed-return portfolio until Year 32. In effect, that investor waited three decades for stocks to reward her patience. She would have been ill served indeed to time the market by exiting just as equities were finally coming good.)

One approach, perhaps, is to divide the retirement portfolio into two buckets, one of which is invested conservatively as the retirement date approaches, to establish an investment floor. The remaining assets could then be invested boldly, thereby ensuring that the worker participates at least partially in a stock market rally, should that occur during the latter stages of her career.

Those, of course, are just passing thoughts. The central point of today’s article is that workers, as with retirees, face sequence risk—only in their case, the danger is that the weak performance arrives late in the game, rather than early.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/WDFTRL6URNGHXPS3HJKPTTEHHU.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IFAOVZCBUJCJHLXW37DPSNOCHM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/JNGGL2QVKFA43PRVR44O6RYGEM.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)