529 Education Savings Plans That Receive Top Marks

Looking for a way to tax-consciously invest for future educational expenses? A top-rated 529 plan could be an answer.

/s3.amazonaws.com/arc-authors/morningstar/de44b91c-c918-4e53-81c3-ce84542f3d36.jpg)

During the April tax season, many families review their financial profiles and consider contributions to a tax-advantaged investment account. One such option is a 529 education savings plan. Overseen by individual states and available through two channels—either sold by advisors or available directly to individual investors—they encourage savers to put money aside for future qualified education expenses with some enticing tax advantages. Depending on the state and the plan, contributions may be tax-deductible. While invested in a 529 plan, earnings accumulate tax-free and withdrawals are not taxable when used to pay for qualified education expenses, such as tuition and relevant books, supplies, and equipment.

But with 90 or so plans to choose from, which are the most compelling options? Morningstar rates 62 plans, and only three currently earn a Morningstar Analyst Rating of Gold. This top-level rating is based on an assessment of four underlying pillar inputs: People, Process, Parent, and Price. The individual pillars consider best-in-class industry practices that, when rolled up to the Morningstar Analyst Rating for 529 Plans, reflect our confidence in the plan’s potential to provide participants with a thoughtfully structured and risk-aware process that generates compelling performance relative to peers. Plans with Above Average People ratings have skilled investment teams with experience managing multi-asset strategies. For the Process Pillar, we look for plans that follow what we believe to be best practices, offering age-based or target-enrollment options that utilize a well-researched asset-allocation approach and a robust process for selecting underlying investments. The Parent rating is based on our evaluation of the state agency offering the plan and its ability to provide thoughtful oversight and stewardship. The Price rating considers the fees of the investment options that comprise the plan, relative to its appropriate Morningstar Category peer. We emphasize fees charged by a plan’s age-based or target-enrollment options, which tend to be the more-popular choice among 529 participants.

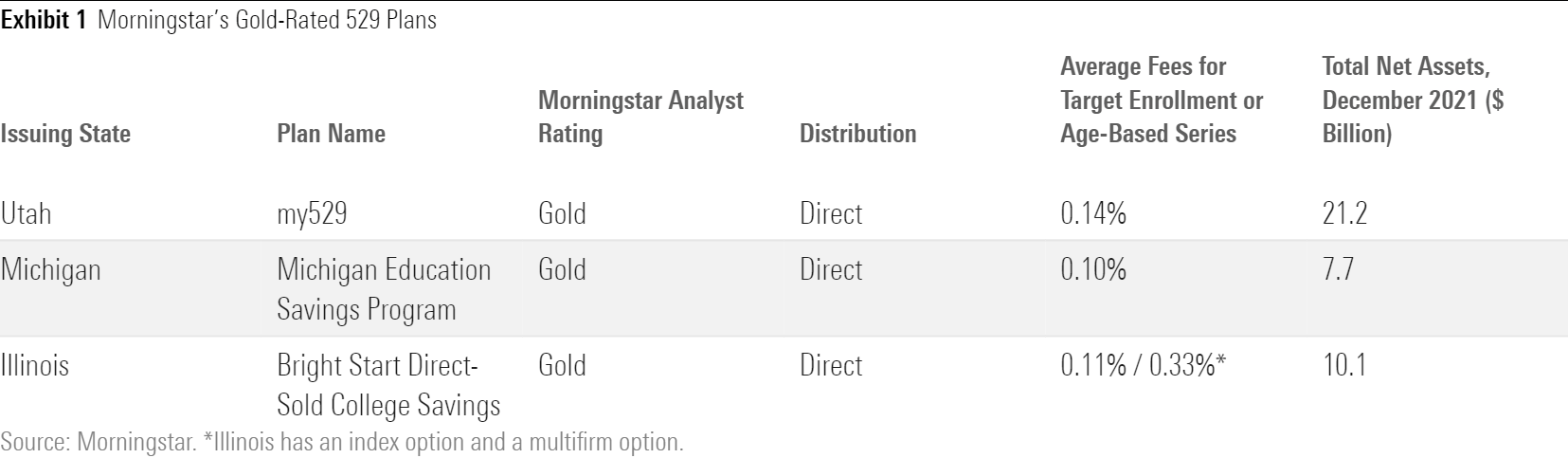

The three plans with Gold ratings are available directly to individual investors and are listed in Exhibit 1. Each offers a well-designed age-based or target-enrollment series, which are set-it-and-forget-it investment options that gradually de-risk during the accumulation and savings period. These series can serve as a default choice for most investors, similar to a target-date series for retirement savers. These Gold-rated plans also employ a solid menu of static options of mutual funds and/or exchange-traded funds that provide exposure to individual asset classes and a safe vehicle to park cash, such as an FDIC-insured savings account.

Exhibit 1 Morningstar's Gold-Rated 529 Plans

Utah Offers Flexibility

Utah’s my529 has consistently been one of our favorite offerings. The 10-portfolio series employs a progressive glide path, in which the equity allocation is gradually trimmed (four times a year) over an investor’s time horizon, starting at 100% equities at age 4 and landing at 10% in the Enrolled portfolio. The underlying lineup of four Vanguard index funds and two principal preservation vehicles provides broad exposure with no frills. This design earns it an Above Average Process rating. This gradual shift is an industry best practice, as it helps education savers avoid the risk of meaningfully shifting out of equities just after a market dip, when there is the potential to lock in losses. The fees for these portfolios are low, at 0.14%-0.15%.

The my529 team boasts topnotch resources, underpinning a High People rating. A dedicated group of roughly 75 professionals handles everything from portfolio management to recordkeeping. The team also receives support from an investment advisory committee and multiple independent consultants. These additional resources and insights keep the plan ahead of 529 peers. We rate the state parent High: Its centralized oversight structure allows for engaged stewardship of the plan, and the state has earnestly continued to reduce fees.

One distinctive feature that is offered only by the Utah plan is the ability to create a custom series in which investors design their own glide path and select the underlying investments. The investment menu includes 22 options, such as Vanguard index funds and DFA funds that cover broad asset classes, style and size, and strategies with a sustainable investment focus. Given the degree of customization for this option, it is suitable for experienced investors or those who work with an investment advisor. The fees are higher for these portfolios and range from 0.14% to 0.49%.

Michigan Is Straightforward at an Attractive Price

Michigan Education Savings Program is notable for offering an easy-to-use, straightforward series with extremely low average fees of 0.10%. Michigan also employs a progressive glide path, but one slightly flatter than Utah's, as it starts with an 80% equity allocation and lands at 20% by college enrollment. (This can result in some performance differences depending on the market environment.) This shape is influenced by the historical average age of the beneficiary when the account opens. This prudent approach aids investors who may have delayed saving for education expenses and supports a High Process rating. The enrollment-date portfolios hold mostly index funds, with a slightly more diversified lineup relative to Utah, as it also includes REITs, Treasury Inflation-Protected Securities, and high-yield bonds.

This plan was designed via an effective collaboration between the Michigan Bureau of Investments and its dedicated program manager TIAA-CREF, which underpins an Above Average People rating. Michigan, with its investment staff, conducts in-house research and taps participant studies to make informed investment decisions on behalf of beneficiaries. Their dedication to shaping a simple, low-cost plan around their participants’ evolving needs also supports a High Parent rating.

Illinois Provides a Full Gamut of Choices

The Illinois’ Bright Start Direct-Sold College Savings Plan offers two different age-based series: one that uses only low-cost Vanguard funds and a multifirm one that employs a blend of active and passive strategies. The index series is cheap, with portfolio fees of 0.11%-0.12% and the blend portfolios charging 0.20%-0.41%. The blend series offers a broader mix of asset classes, providing slightly more diversification relative to its index series, as well as those from Michigan and Utah.

The state Treasury office teamed up with Wilshire Associates to design and run this plan. For both series, the glide path is available at three risk levels: aggressive, moderate, and conservative. They start with equity allocations of 100%, 90%, and 80%, respectively. The Utah and Michigan glide paths tend to fall somewhere between Illinois’ aggressive and moderate offerings. The Illinois glide path is stepped; this means the equity allocation is trimmed about once every two years, so it is not as smooth as Utah’s and Michigan’s progressive glide paths. For the index series, the asset-class exposure is similar to that of the Michigan plan. The blend series boasts a strong lineup that includes a number of Gold-rated actively managed funds, such as Dodge & Cox International Stock DODFX and BlackRock High Yield Bond BHYIX. With six well-designed offerings and an excellent lineup of underlying funds, this plan earns a High People and Process rating. We rate the Parent Above Average, which reflects its solid oversight for this plan, as well as the advisor-sold plan.

Conclusion

All three plans offer a compelling menu of options, but with slight differences. Investors who want to choose their risk level (conservative, moderate, or aggressive) and/or want a mix of index funds and highly regarded active funds in their age-based or target enrollment series might consider using the Illinois plan. Those who want a very low-cost, straightforward target enrollment series can chose the Michigan plan. The flexibility offered by Utah, combined with reasonable fees, can be used by more-experienced investors or those working with a professional financial advisor.

This is the first in a five-part series focused on 529 education savings plans.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/KD4XZLC72BDERAS3VXD6QM5MUY.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/BZ4OD6RTORCJHCWPWXAQWZ7RQE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/JNGGL2QVKFA43PRVR44O6RYGEM.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/de44b91c-c918-4e53-81c3-ce84542f3d36.jpg)