U.S. ESG Funds Outperformed Conventional Funds in 2019

A look back at the year in sustainability.

/s3.amazonaws.com/arc-authors/morningstar/42c1ea94-d6c0-4bf1-a767-7f56026627df.jpg)

Sustainable funds outperformed their conventional fund peers in 2019, helped in part by underweighting energy company investments but also by continuing a general trend from recent years of better performance than non-environmental, social, and governance funds.

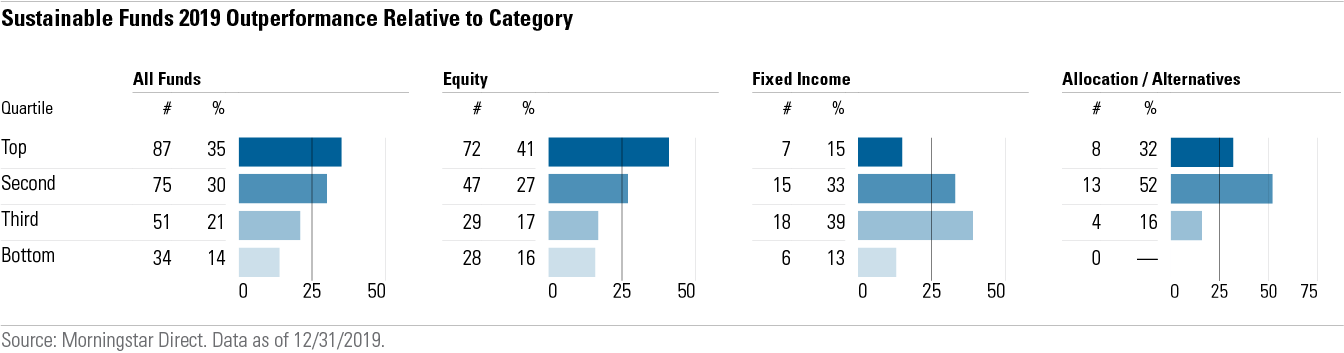

Overall Performance by Morningstar Category Rank To evaluate the investment performance of sustainable funds, we examined the rankings of their returns relative to their Morningstar Categories. The following chart groups those return ranks by quartile.

Sustainable funds comfortably outperformed their peers in 2019. The returns of 35% of sustainable funds placed in the top quartile of their respective categories, and nearly two thirds finished in the top two quartiles. By contrast, the returns of only 14% of sustainable funds placed in the bottom quartile, and only about one third placed in the bottom half.

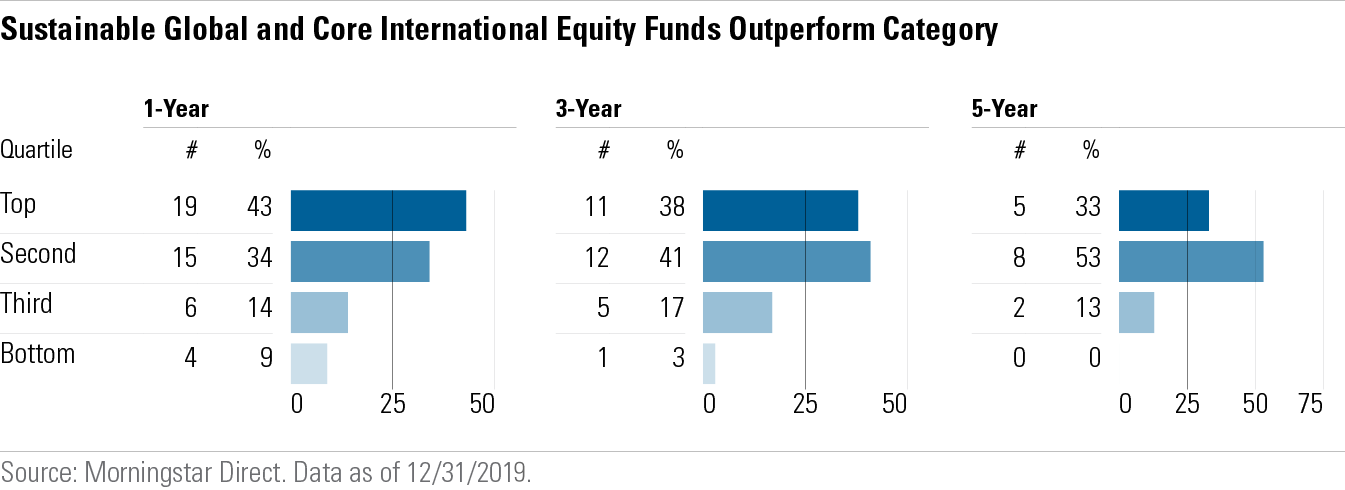

Sustainable equity funds did even better, with the returns of 41% ranking in the top quartile of their respective categories, and 68% in the top two quartiles. The returns of only 16% placed in the bottom quartile and 33% in the bottom half.

The relative returns of sustainable fixed-income funds in 2019 were more or less average for their categories and clustered into the middle two quartiles, while those of sustainable allocation and alternative funds skewed more positively. Overall, rather than their returns being distributed evenly within their respective categories, the returns of sustainable funds were skewed toward the top half, with the returns of two thirds landing in the top half and one third in the bottom half.

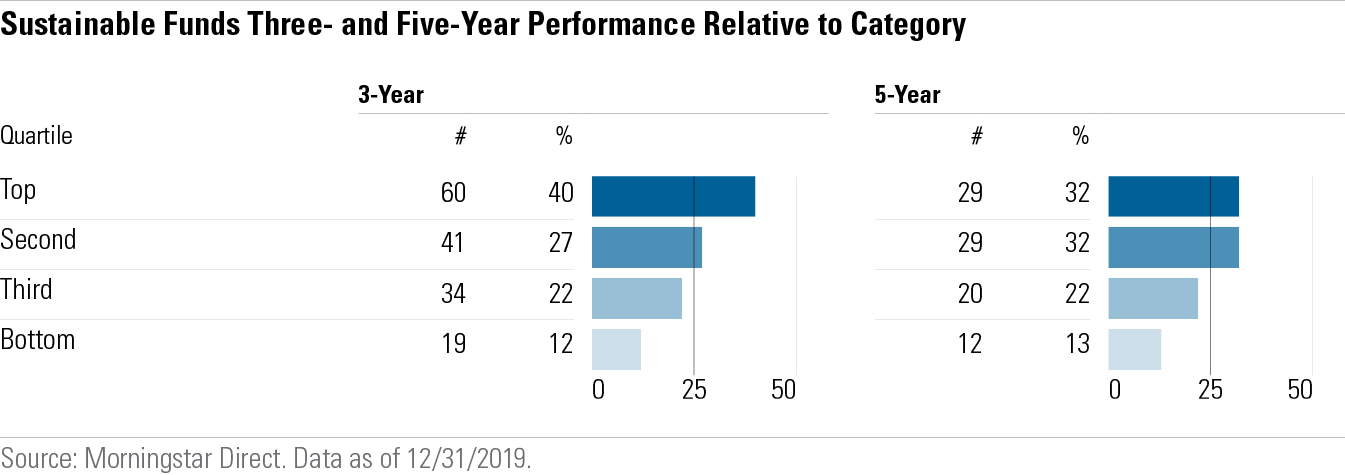

Focusing on the trailing annualized three-year returns through the end of 2019, we see a similar pattern. The returns of 40% of sustainable funds placed in the top quartile of their categories, and two thirds finished in the top half. Much of that outperformance was driven by sustainable equity funds. We see a similar story over the trailing five years, even though only 90 sustainable funds have five-year records, compared with 154 sustainable funds that have three-year records.

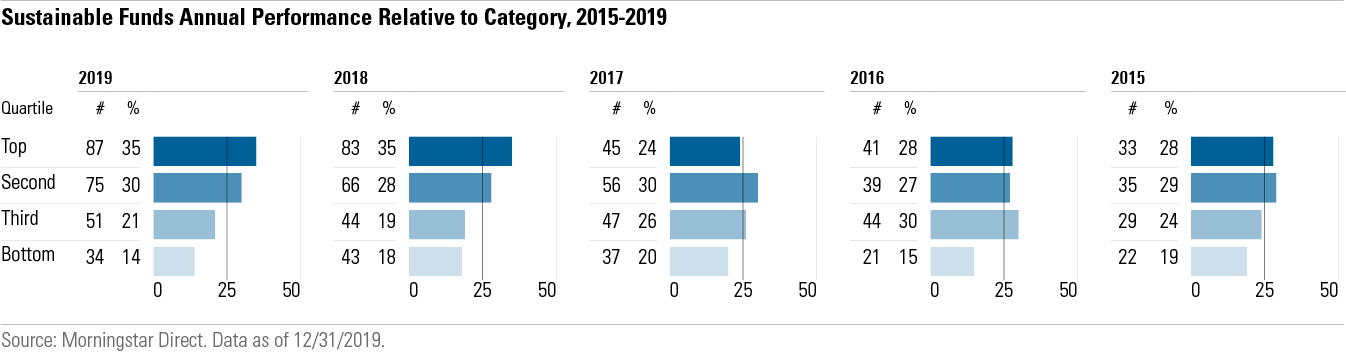

Over the past five years, sustainable funds have done well in both up and down markets relative to their conventional peers. When markets were flat (2015) or down (2018), the returns of 57% and 63% of sustainable funds placed in the top half of their categories. When markets were up in 2016, 2017, and 2019, the returns of 55%, 54%, and 65% of sustainable funds placed in the top half of their categories.

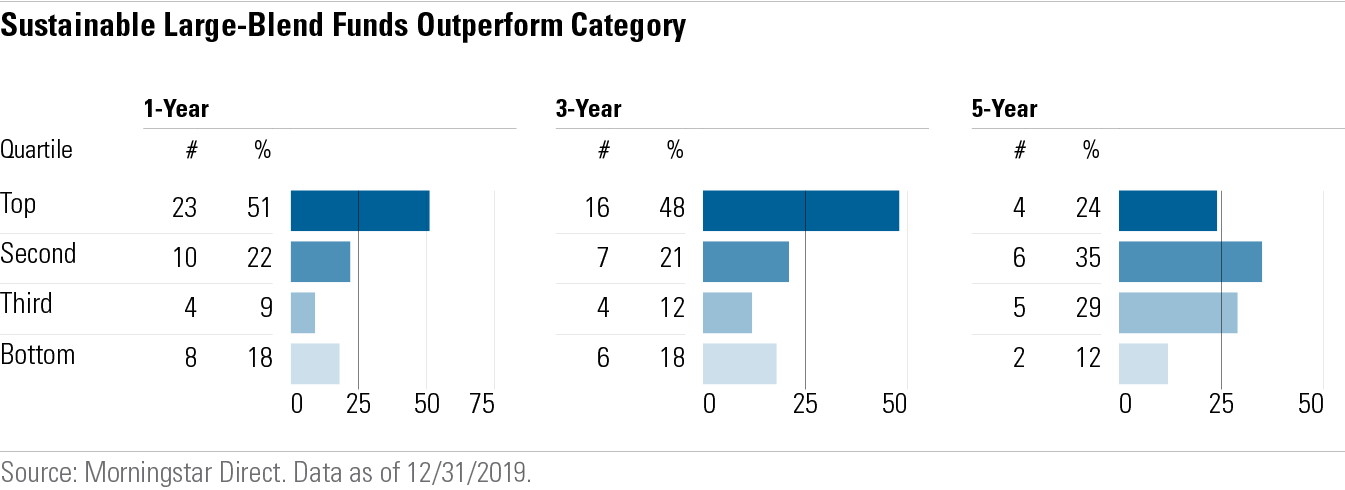

Performance of Sustainable Large-Cap Equity Funds Most investors have significant exposure to the world's largest companies, and the largest groups of sustainable funds are those that invest in U.S. and global large-cap equity. These funds outperformed in 2019 and for the trailing three and five years.

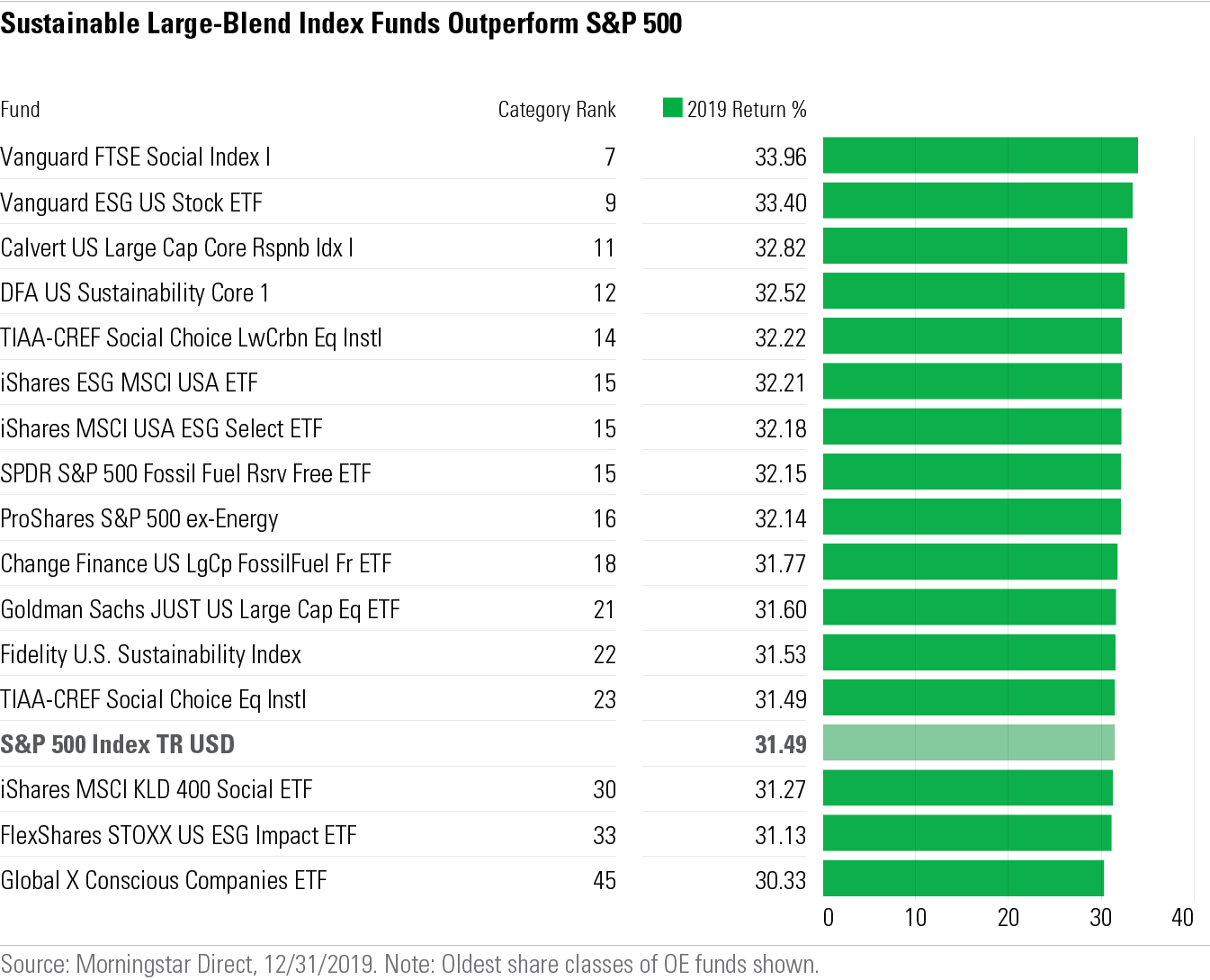

U.S. Large Cap: Investors have 56 sustainable-fund options in the large-blend category, and as a group, sustainable large-blend funds turned in an impressive 2019. Of the 45 funds with full-year records, the returns of 23 ranked in the category's top quartile, and the returns of 73% ranked in the top half. Moreover, all of the top-quartile sustainable funds (23 of 45) beat the S&P 500 for the year. That is a 51% "beat rate," twice that of large-blend funds overall.

Over the longer periods, nearly half of the 33 sustainable large-blend funds with sufficient records place in the category's top quartile for the trailing three years. Although the group diminishes to only 17 funds with five-year records, more than half place in the category's top half for the trailing five years.

Among sustainable index funds in the large-blend category, 13 of 16 matched or outperformed the S&P 500 in 2019.

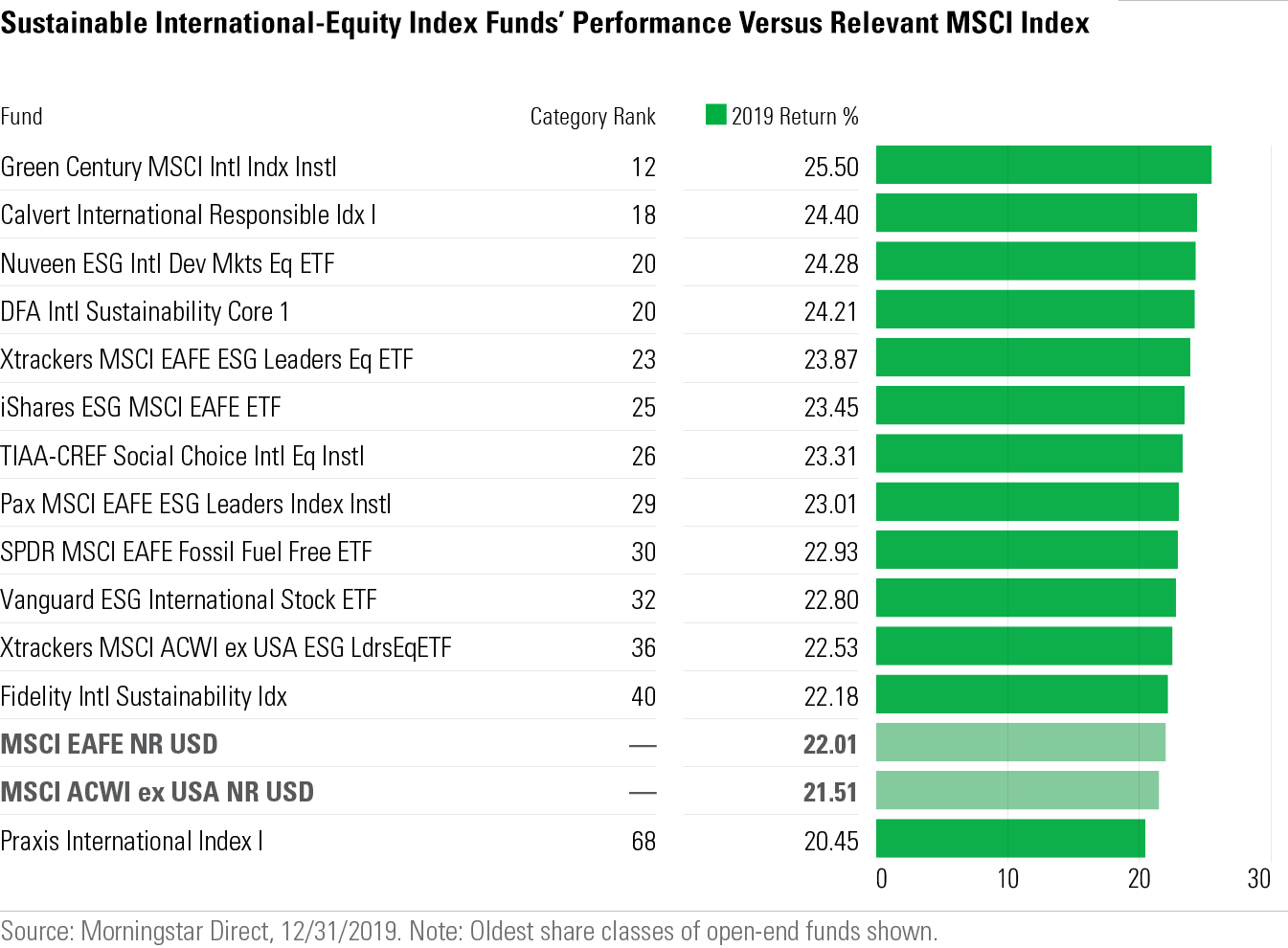

Global and Non-U.S. Developed-Markets Large Cap: There are 48 sustainable funds that focus on developed-markets large-cap equities, of which there are 30 diversified sustainable global funds focused on large-cap equities in developed markets, including the United States. These funds are in the world large-stock category. The remaining 18 funds focus on core non-U.S. large caps and reside in the foreign large-blend category.

Of the 44 sustainable funds with full-year records, the returns of 19 ranked in the top quartile of their categories with another 15 in the second quartile. That is an impressive 43% top-quartile rate and a 77% top-half rate.

By contrast, the returns of only four funds ranked in the bottom quartile. While the ranks of funds with longer-term records thin considerably, the three- and five-year returns of the older sustainable funds rank even better relative to their categories.

Among sustainable index funds that focus on non-U.S. large caps, 12 out of 13 beat the relevant conventional index, either the MSCI EAFE or MSCI ACWI ex USA.

A partial explanation for the outperformance of sustainable equity funds--both U.S. and global--may lie in their sector weightings. They have been, on average, underweight energy during a period of significant underperformance by that sector. Diversified sustainable U.S. equity funds have about a 1.9% average energy weighting compared with 3.9% for the S&P 500. That difference alone, however, does not explain the relative outperformance of sustainable funds across categories.

Similarly, many have the impression that sustainable funds are overweight technology, which could be responsible for their relative outperformance. But diversified sustainable U.S. equity funds have an average 23.9% weighting to the information technology sector, just about the same as the S&P 500's 24.2% weighting.

The performance of sustainable funds relative to the fund universe is consistent with evidence from academic research, which suggests no systematic performance penalty associated with sustainable investing and possible avenues for outperformance through reduced risk or added alpha.

Because of the variety of approaches that a fund manager can take to sustainability and to other facets of the investment process, including passive funds optimized to minimize tracking error to conventional market-weighted indexes and differences in the skill of active managers, consistent year-by-year outperformance by sustainable funds relative to the fund universe seems unlikely, yet it has happened in each of the past five calendar years.

Jon Hale has been researching the fund industry since 1995. He is Morningstar’s director of ESG research for the Americas and a member of Morningstar's investment research department. While Morningstar typically agrees with the views Jon expresses on ESG matters, they represent his own views.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HDPMMDGUA5CUHI254MRUHYEFWU.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/OMVK3XQEVFDRHGPHSQPIBDENQE.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/42c1ea94-d6c0-4bf1-a767-7f56026627df.jpg)