Turning 401(k) Plans into Lifetime Investments

The Department of Labor lays the groundwork.

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

10 Years Later Starting next year, 401(k) participants will regularly receive information about the amount of income that their plan assets might deliver during retirement. The Department of Labor has announced an "interim final rule" that would require 401(k) administrators to show each participant's account balance not only as a lump sum, but also as a projected monthly income stream.

This decision has been a long time coming. The DOL first floated the concept February 2010, then followed up with the details in May 2013. Seemingly forgotten, the proposal resurfaced because of the SECURE Act of 2019, which amended various retirement-plan regulations. Among the Act's mandates was that plan sponsors provide participants with projected-income calculations. Voila! The DOL had but to dust off its 2013 submission.

The ruling is modest, mandating only disclosure. (Consequently, the expense of complying will also be modest, with the annual cost estimated at one penny for each $10,000 of investor assets.) But its implications are deeper. Once investors have been told how much income their accounts can generate, they may begin to think of their 401(k) accounts not solely as lump sums during their working years, but also as retirement paychecks. Perhaps they will keep their accounts for life.

That is what insurance companies desire. By its own admission, the Insured Retirement Institute, which represents companies that sell annuities (along with any other insured retirement strategies), "fought hard" to include this provision in the SECURE Act. Ultimately, insurers would like to place annuities inside 401(k) plans, so that employees who wish to convert their lump sums into income can accomplish that task within the plan.

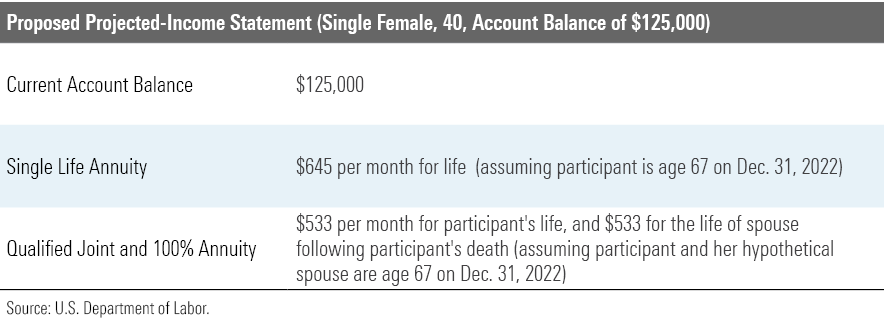

Short and Simple The required disclosure consists of three data points: 1) the participant's current account balance; 2) the lifetime expected monthly payment for that balance, should it be used upon the employee's retirement date to buy a single premium immediate annuity; and 3) the lifetime expected monthly payment, if the balance is used instead to purchase a joint immediate annuity.

The DOL’s fact sheet illustrates the presentation. Its sample participant is female, 40 years old, and single. Her 401(k) plan holds $125,000. Should the interim rule be ratified (likely), her statement will contain this section:

Note that although the DOL’s example specifies the participant’s gender, age, and marital status, it largely disregards such information for its disclosure. The annuity calculations use gender-neutral mortality tables, so that male and female results are identical; the assumed retirement age for all participants is 67, beginning on the final day of the employee’s current statement; and both the single and joint results appear, regardless of the employee’s marital status.

These choices can be defended. Although gender typically affects annuity rates, and therefore would be a helpful investment input, gender-neutral tables are the legal standard. Similarly, although assuming a retirement age of 67 is overly optimistic, because most workers who expect to work until that age fail to do so, that schedule aligns with the date when Social Security pays full benefits.

The choice to ignore the participant’s age looks silly. Why depict a December 2022 retirement date, at “age 67,” for a 40-year old? But that objection, too, can be addressed. Clearly, nobody can forecast future annuity rates. It's best, therefore, to use today’s annuity rate (derived from the interest rate on the constant-maturity 10-year Treasury note and the aforementioned mortality table) with the understanding that the payout rate will fluctuate over time.

Finally, showing both single and joint annuity rates is prudent, as marital statuses change. (Also, the plan administrator may not collect such information.)

The Positives The IRI, understandably given its business desires, glowingly extols the disclosure. The institute's research "overwhelmingly shows that workers want these estimates and would actively save more for retirement" if such numbers appeared on their statements. Per its study, 75% of employees stated that the additional figures would encourage them to raise their 401(k) contribution rate.

Believe that 75% figure when pigs fly, cows dance, and dogs preach sermons. The intentions of investment-survey respondents greatly outweigh their subsequent deeds. But the point remains. Lump sums don't convey much understanding. It's clear that possessing $190,000 beats having $125,000, but what does that really mean? Converting to monthly income provides the context. Increasing the lump sum by another $65,000 pushes the projected monthly payment for a single participant from $645 to $980. That is clear.

Another benefit from the disclosure should be reducing the problem of "leakage," whereby employees spend their alleged retirement assets when switching jobs, or by taking loans against their accounts that they don't repay. That unfortunate habit has been well documented. The issue cannot be fixed without the severe solution of banning participants from early withdrawals, but it can be alleviated by more tangibly connecting their 401(k) investments to their retirement futures.

The Peril There is, however, one big concern with the DOL's proposal: the projection's optimism. As discussed, the DOL's decision to use a retirement age of 67 is not without merit. But it does yield an unrealistically high annuity rate for most newly minted retirees, as the median retirement age is 62. Defaulting to that age rather than 67 would cut projected monthly income by about 15%.

Also, not everyone will wish to annuitize. Indeed, while the insurers hope to change retiree habits, relatively few people buy immediate annuities today, in part because the decision is final. Once those assets are spent on purchasing the annuity, they can never be retrieved. But if retirees do forgo the annuity, they will have difficulty matching its payout, even if they start at age 67. Annuities have their disadvantages, but they do yield more than most investment alternatives.

Finally, unlike Social Security, those projected 401(k) payouts are nominal. They will not be adjusted by cost-of-living increases.

Thus, while the monthly income statement is instructive, and should encourage better investor behavior, it does run the danger of being too good to be true.

John Rekenthaler (john.rekenthaler@morningstar.com) has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar's investment research department. John is quick to point out that while Morningstar typically agrees with the views of the Rekenthaler Report, his views are his own.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/5WSHPTEQ6BADZPVPXVVDYIKL5M.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/OMVK3XQEVFDRHGPHSQPIBDENQE.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/BNHBFLSEHBBGBEEQAWGAG6FHLQ.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)