September ETF Inflows Hold Steady Amid Inflation, Interest-Rate Uncertainty

A turbulent month in the markets doesn't throw ETF investors off course.

/s3.amazonaws.com/arc-authors/morningstar/30e2fda6-bf21-4e54-9e50-831a2bcccd80.jpg)

/s3.amazonaws.com/arc-authors/morningstar/a90ba90e-1da2-48a4-98bf-a476620dbff0.jpg)

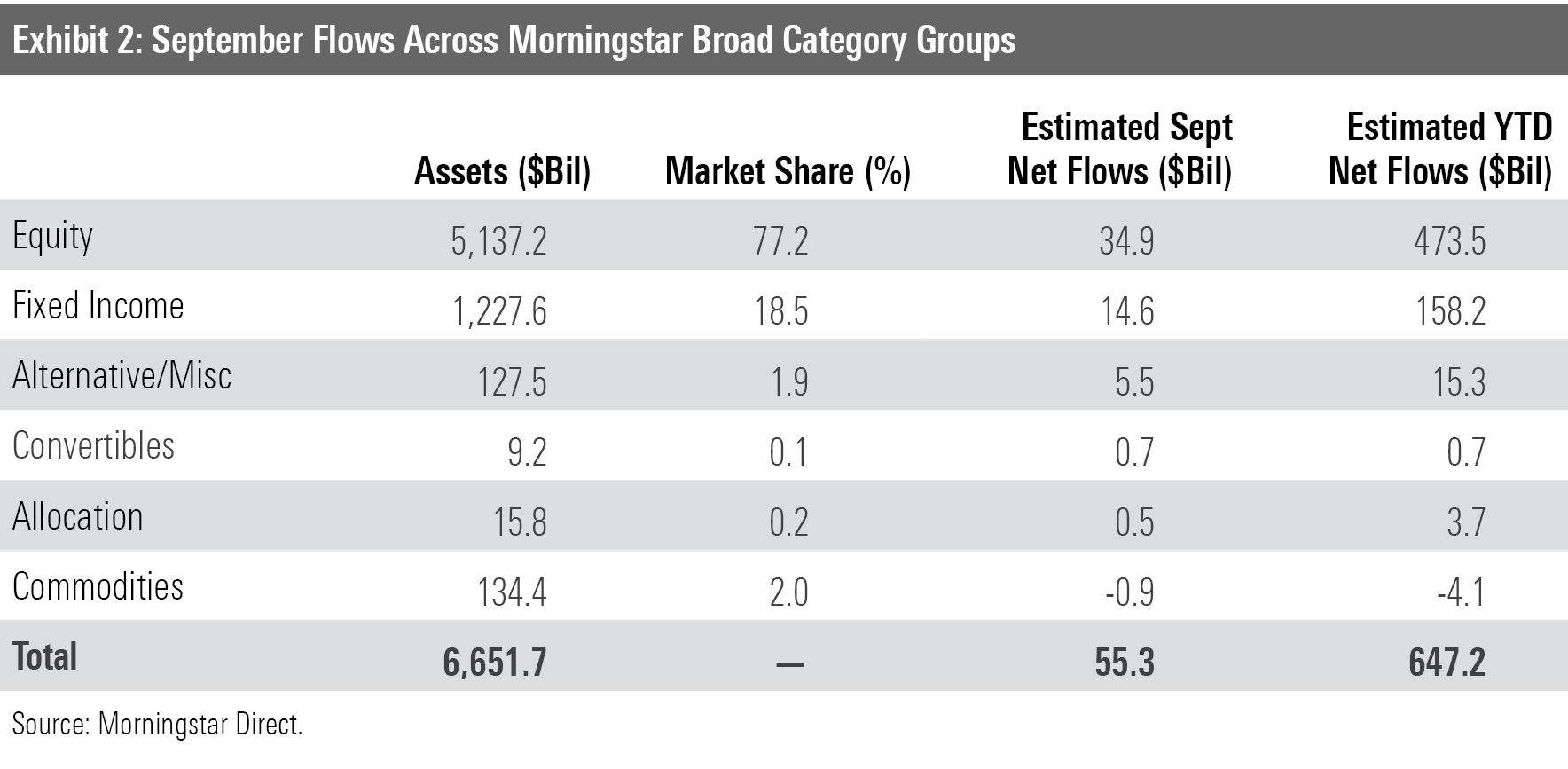

Despite tumult in the markets, U.S. exchange-traded funds notched another solid month of inflows in September 2021. Investors poured $55 billion into ETFs last month. ETFs have absorbed $647 billion through the first three quarters of 2021, and the $499 billion net flow record set in 2020 continues to drift further into the rearview.

After a tremendous run to start the year, global stock markets stumbled in September. The Morningstar Global Markets Index--a broad gauge of global equities--slid 3.96% last month. That snapped a seven-month streak of positive returns and marked the benchmark's worst monthly performance since the coronavirus-induced sell-off in March 2020. Bonds fared a bit better but still finished in the red for the second consecutive month. After declining 0.96% in September, the Morningstar US Core Bond Index has now dropped 1.36% for the year to date.

Here, we'll take a closer look at how the major asset classes performed in September, where investors put their money, and which corners of the market looked rich and undervalued at month's end--all through the lens of ETFs.

September Stumbles

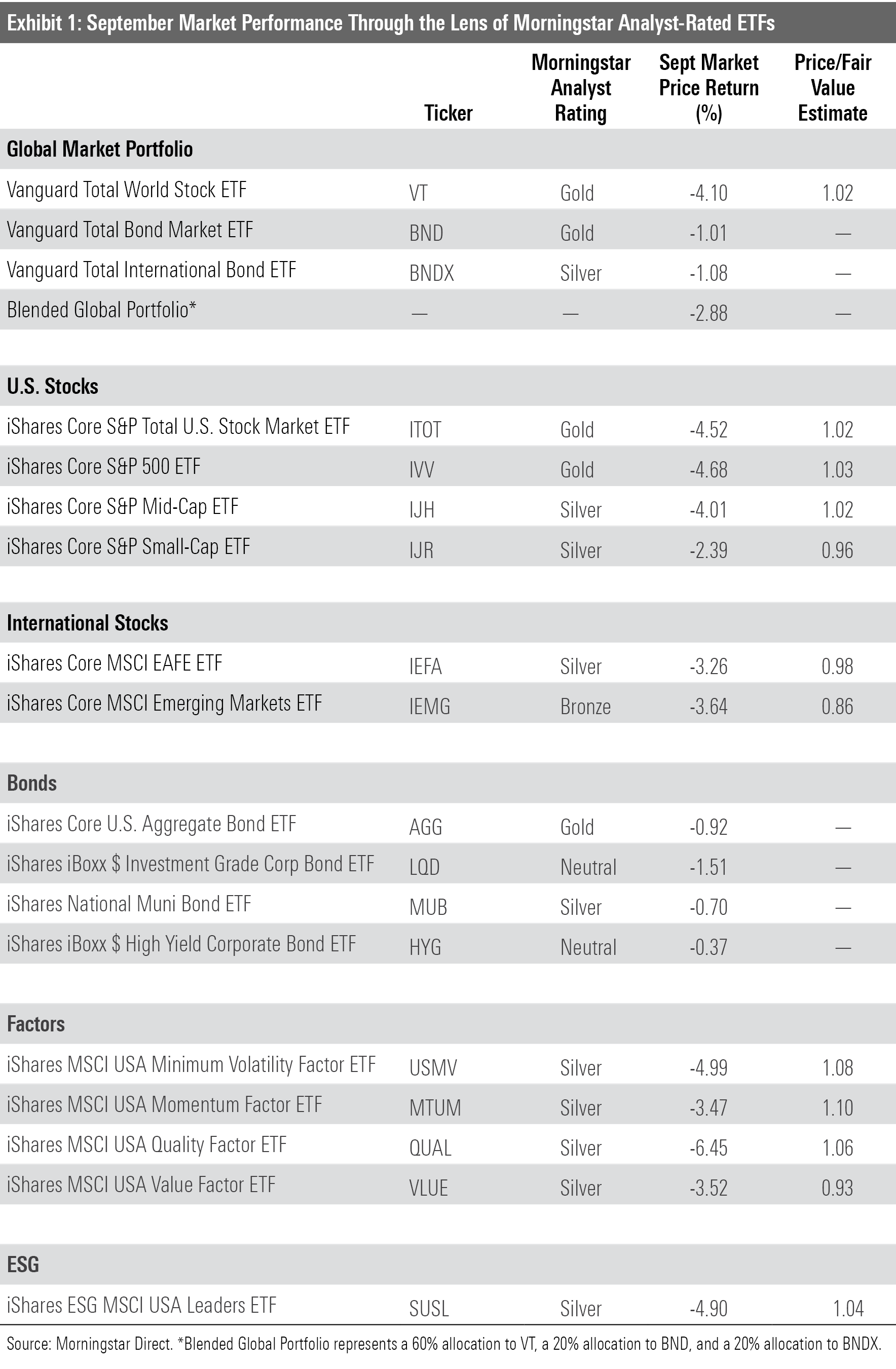

Exhibit 1 shows the September returns for a sample of Morningstar Analyst-rated ETFs that serve as proxies for major asset classes. Investors in a blended global portfolio suffered a 2.88% loss last month. After a stellar summer of performance, Vanguard Total World Stock ETF VT–-the portfolio's equity anchor--declined 4.10% in September. The bond sleeve held up better but couldn't pull the portfolio toward positive territory. Vanguard Total Bond Market ETF BND and Vanguard Total International Bond ETF BNDX posted declines of 1.01% and 1.08%, respectively.

U.S. stocks came back down to earth after a scorching run through the first eight months of 2021. IShares Core S&P Total U.S. Stock Market ETF ITOT, a broad collection of U.S. equities, slid 4.52% in September--its worst one-month performance since March 2020. This sizable step backward likely came in response to the Federal Reserve's shift in tone on monetary policy. Fed Chair Jerome Powell indicated in September that it could start to slow bond purchases as soon as November and raise interest rates sometime next year.

Growth stocks bore the brunt of the Fed's shift in stance. Faster-growing stocks tend to thrive in low-interest-rate environments, in part because their cash flows are expected to come further in the future. Vanguard Growth ETF VUG dropped 5.33% last month, falling about 1.5 percentage points further than value counterpart Vanguard Value ETF VTV. This marks the latest chapter in the seesawing performance between value and growth stocks this year; VUG has led the way in four months so far, VTV in five. After 2021's first three quarters, VUG's 14.98% return narrowly trailed VTV's 15.7% gain.

While the downturn was widespread in the U.S. market, historically cheaper sectors held up better in September. Energy stocks, which value funds tend to favor, led all sectors by a wide margin last month as oil prices soared to prepandemic levels. Energy Select Sector SPDR ETF XLE advanced 8.97% in September. It was the only sector ETF in the SPDR suite to post a positive return. Financials and consumer staples stocks--mainstays of most value portfolios--fared relatively well, too. Bank stocks tend to stack up well in rising-rate environments because of the interest-rate revenue they derive from loan operations. JPMorgan Chase JPM, Bank of America BAC, and Wells Fargo WFC all finished September in the black. On the other hand, faster-growing tech stocks struggled. Technology Select Sector SPDR ETF XLK's 5.84% drop marked its worst monthly performance since March 2020, as it was dragged down by high-growth holdings like Nvidia NVDA, PayPal PYPL, and Adobe ADBE.

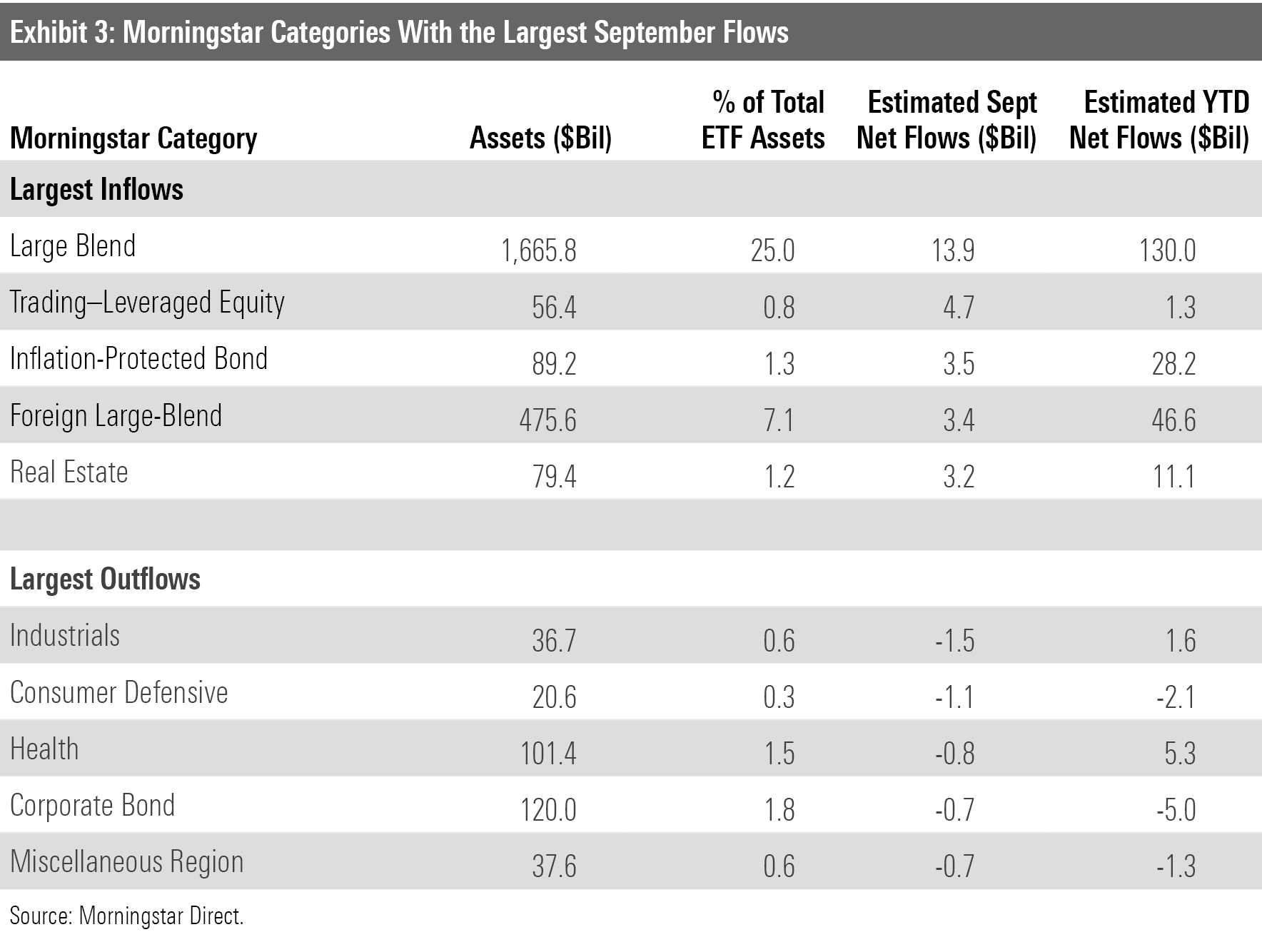

After large-cap stocks dominated the summer, small caps came out on top in September. IShares Core S&P Small-Cap ETF IJR lost 2.39% last month, while iShares Core S&P 500 ETF IVV tumbled 4.68%. These ETFs' relative performance overlaps with that of value and growth stocks. IJR tends to take on a more value-oriented posture. Compared with IVV, it favors energy and financials stocks and takes relatively light stakes in the technology and communication-services sectors.

Small-cap stocks also tend to be more economically sensitive, and the prospects for a fully reopened U.S. economy quietly improved last month. After a late-summer spike, coronavirus cases slowed down in September. The seven-day rolling average of U.S. reported cases dropped by about 35% from the start of the month to the end, according to data from the CDC. Over three fourths of U.S. adults had received at least one dose of the COVID-19 vaccine, per the CDC. Travel-dependent leisure stocks like Carnival CCL and MGM Resorts MGM advanced as the market broadly pulled back.

ETFs in iShares' suite of single-factor funds were not immune to the broad market's struggles in September. IShares MSCI USA Quality Factor ETF QUAL--which tends to strike a defensive stance--faced a particularly difficult month. It anchors its sector composition to that of the broad market but was hampered by unfavorable stock selection. In the financials sector, QUAL opted for asset-management firms like BlackRock BLK and T. Rowe Price TROW instead of the banks that held up quite well. Even more counterintuitively, iShares MSCI USA Minimum Volatility Factor ETF USMV--which is designed to outperform the market during drawdowns--slid further than the broad market. It has poor sector allocation to blame. The fund took relatively light stakes in energy and financials stocks, the two most-volatile sectors over the three years entering September.

TIPS Jar Filling Up

Stock ETFs continued to lead the way in September, but adverse market conditions may have damped investor enthusiasm. The nearly $35 billion that stock ETFs collected in September represented their smallest monthly haul of 2021.

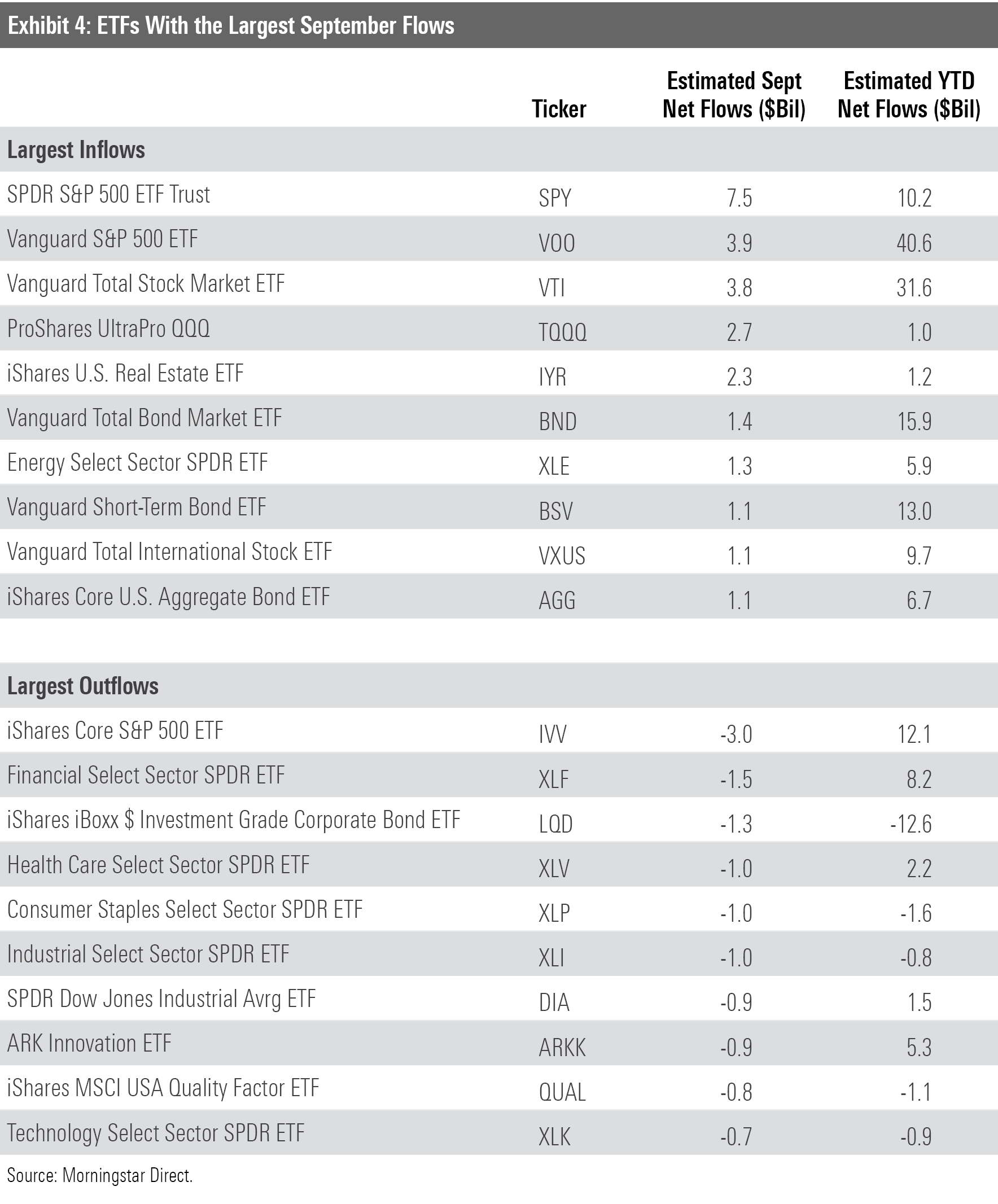

ETFs that land in the alternative broad category group took in nearly $6 billion last month--their steepest monthly inflow this year by a substantial margin. ProShares UltraPro QQQ TQQQ accounted for nearly half of that, pulling in $2.7 billion--including $867 million on Sept. 29 alone. Over the course of the eventful month, the fund notched organic growth of 18% that narrowly offset its sharp September decline of 16.7%. TQQQ delivers triple-leveraged exposure to the tech-heavy Nasdaq-100 Index, which lost 5.69% last month. Whether the sudden interest came from a concentrated few investors or a bevy of Nasdaq-100 believers remains unclear.

Inflation-protected bond funds took in $3.5 billion in September, led by iShares TIPS Bond ETF's TIP $980 million haul. These funds have now collected $28.2 billion for the year to date. With three months to spare, that number more than doubles their previous annual record. Even as the Fed has reiterated that inflation is transitory, it clearly remains top of mind for many U.S. investors.

ETF investors continued to favor the shorter-term bond Morningstar Categories last month, as they come with less interest-rate risk than peers that favor longer-term debt. Intermediate core bond and short-term bond ETFs collectively hauled in over $5 billion in September. These two categories have absorbed $27 billion apiece year to date. Meanwhile, long-term bonds suffered outflows and have collected a modest $178 million through 2021's first three quarters. Bank-loan bond funds notched a solid month as well, raking in $784 million. Like bank stocks, these bond portfolios should fare well in rising-rate environments.

Aside from TQQQ, flows into individual ETFs looked standard in September. Low-cost, broadly diversified index funds continued to consume the lion's share of new investor money. The trio of SPDR S&P 500 ETF Trust SPY, Vanguard S&P 500 ETF VOO, and Vanguard Total Stock Market ETF VTI filled in the top three spots for the second consecutive month. Vanguard's two-headed monster of VOO and VTI has been fixed atop the flows leaderboard; the tandem has jointly raked in $72.3 billion year to date. That tops the 2021 inflows of all categories, excluding the large-blend space in which they reside.

State Street's suite of sector ETFs seemed to fall out of favor with investors in September, irrespective of performance. Five the 10 ETFs to suffer the steepest outflows last month came from that lineup. While performance could explain why investors pulled out of Industrial Select Sector SPDR ETF XLI (negative 6.08% return), Financial Select Sector SPDR ETF XLF held up better than the broad market. The SPDR ETF lineup tends to cater to tactical traders more than long-horizon investors, and shorter-term clients may see this as the time to let their money sit on the sidelines.

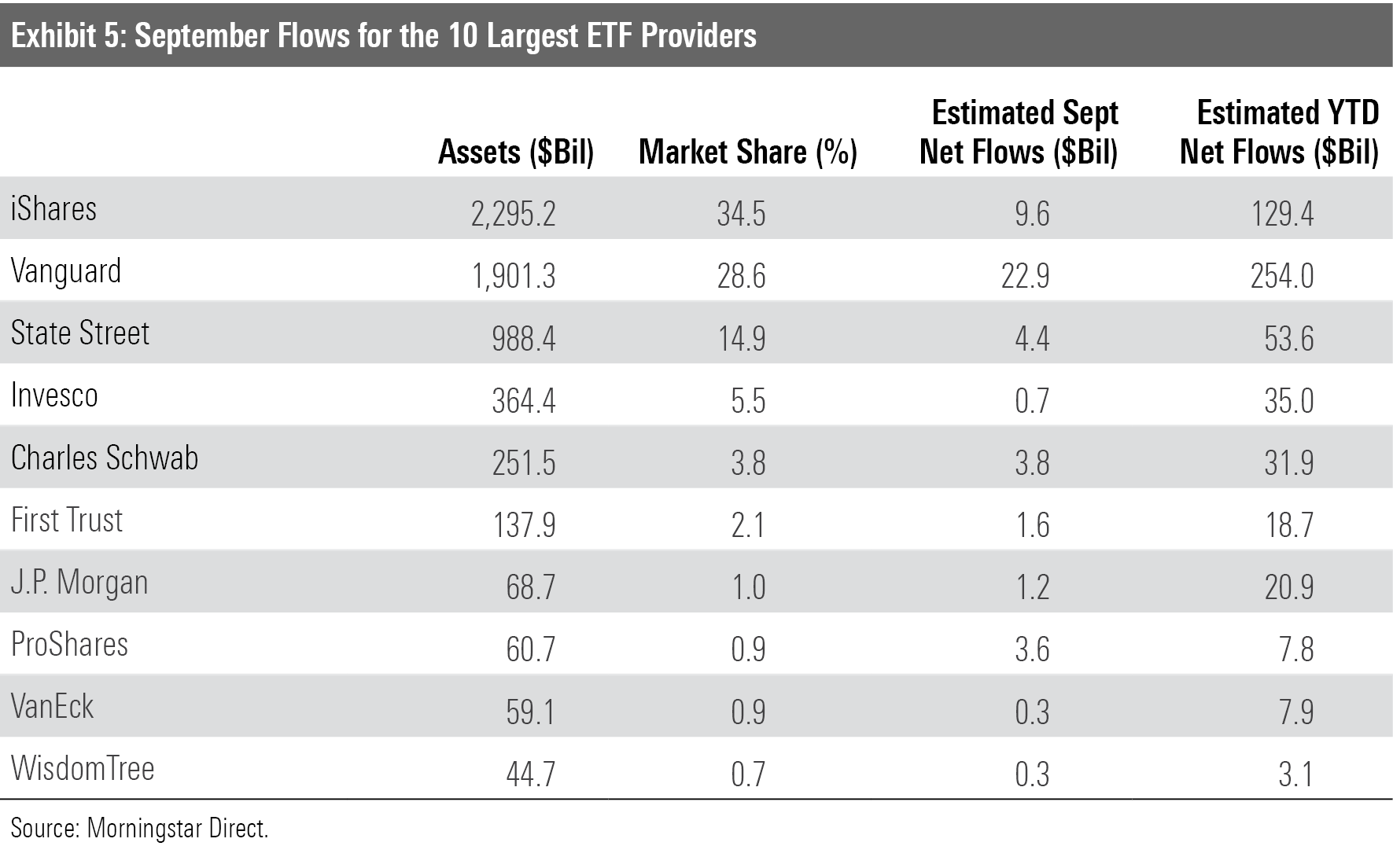

Parental Guidance

Vanguard's ETF lineup collected $22.9 billion in September. While that marked its lowest monthly inflow of 2021, it extended its streak atop the ETF provider flows league table to 10 months. At the end of September, the firm's $254 billion year-to-date take exceeded that of its four closest competitors combined (iShares, State Street, Invesco, and Charles Schwab).

J.P. Morgan has grown its ETF assets under management at a faster rate than any of the other top 10 ETF providers this year. As the seventh-largest ETF provider that claims only 1% of the overall market share, it's easier for J.P. Morgan's AUM to grow at a faster clip than behemoth peers like iShares and Vanguard. Still, J.P. Morgan has seen its predominantly stock ETF lineup add nearly $21 billion year to date. Seven of its ETFs have added more than $1 billion on the year, led by JPMorgan BetaBuilders Europe ETF's BBEU $5 billion haul. Only JPMorgan Diversified Return International Equity ETF JPIN, which has a Morningstar Analyst Rating of Bronze, has experienced outflows greater than $150 million.

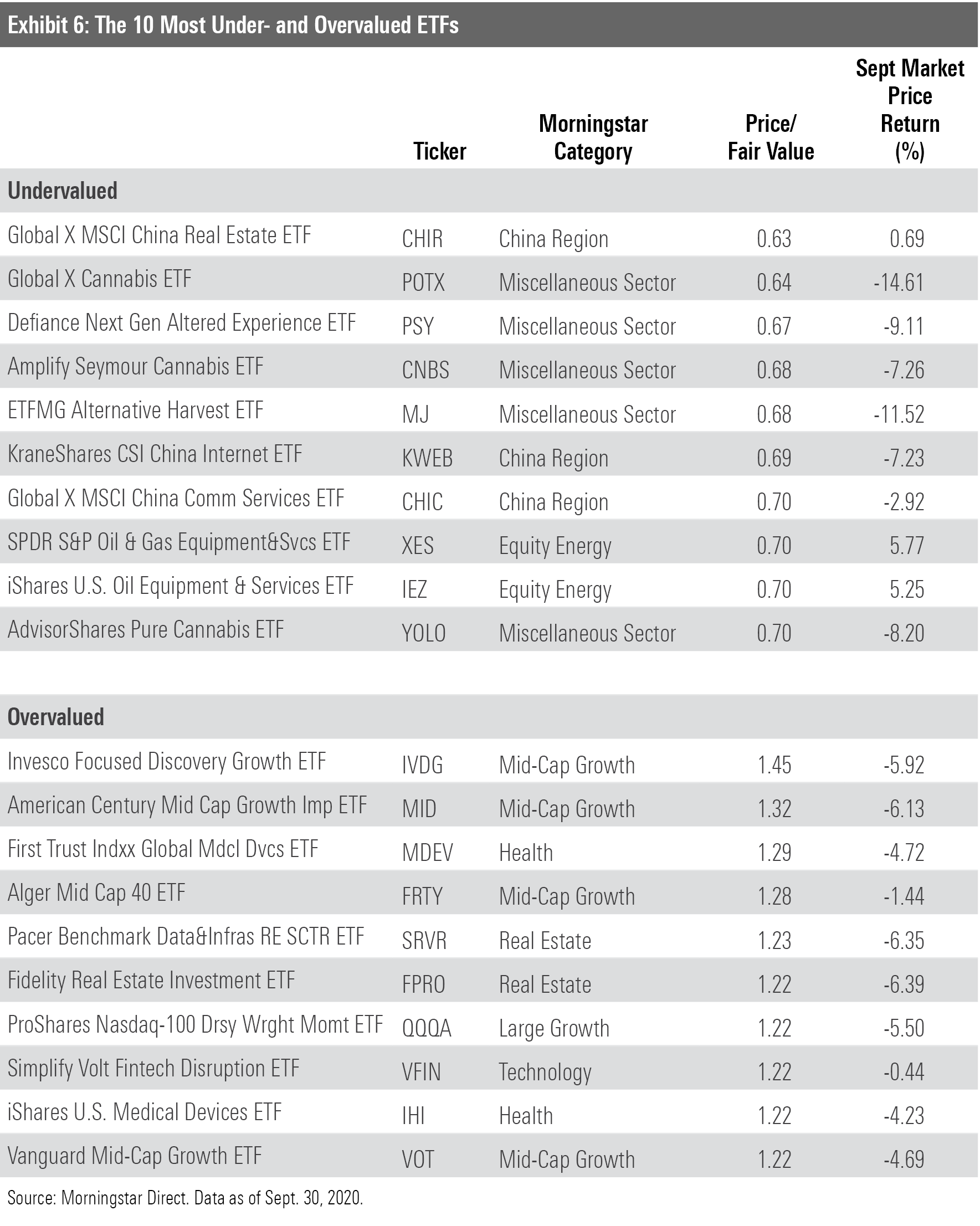

Cannabis ETFs' Valuations Have Gone to Pot

The fair value estimate for ETFs rolls up our equity analysts' fair value estimates for individual stocks and our quantitative fair value estimates for stocks not covered by Morningstar analysts into an aggregate fair value estimate for stock ETF portfolios. Dividing this value by the ETFs' market prices yields the price/fair value ratio. This ratio can point to potential bargains and areas of the market where valuations are stretched.

The "undervalued" half of Exhibit 6 shows funds that traded at the lowest price relative to their fair value at the end of September. ETFs that seek to capitalize on the legalization of cannabis or other drugs constitute half of this month's list. While each of these funds saw sharp declines in September, their performance has not always marched in lock step.

Consider Global X Cannabis ETF POTX and Amplify Seymour Cannabis ETF CNBS. The funds have little in common other than their targeted cannabis theme. POTX tracks a rules-based index that features companies that derive at least 50% of their revenue from the broadly defined cannabis industry. Canadian companies constitute about two thirds of the portfolio. CNBS is an active offering that focuses on U.S. stocks and carries a sharper growth orientation. Only about one third of these portfolios overlap with one another. POTX has dropped 8.79% year to date, while CNBS has notched an 11.18% gain. This illustrates a broader point on thematic funds: Strategies that purport to chase a common theme can do so in very different manners, leading to very different outcomes for investors.

Oil ETFs have been mainstays on the under- and overvalued ETF list since early 2020, but only two such funds made the list this month. Oil stocks broadly climbed in September as worldwide demand for fuel continued its rebound and limited supply drove up prices. After a strong month, SPDR S&P Oil & Gas Equipment & Services ETF XES and iShares U.S. Oil Equipment & Services ETF IEZ both advanced about 23% year to date. Their continued spot on the "undervalued" list shows how far oil stock valuations fell during the COVID-19 downturn.

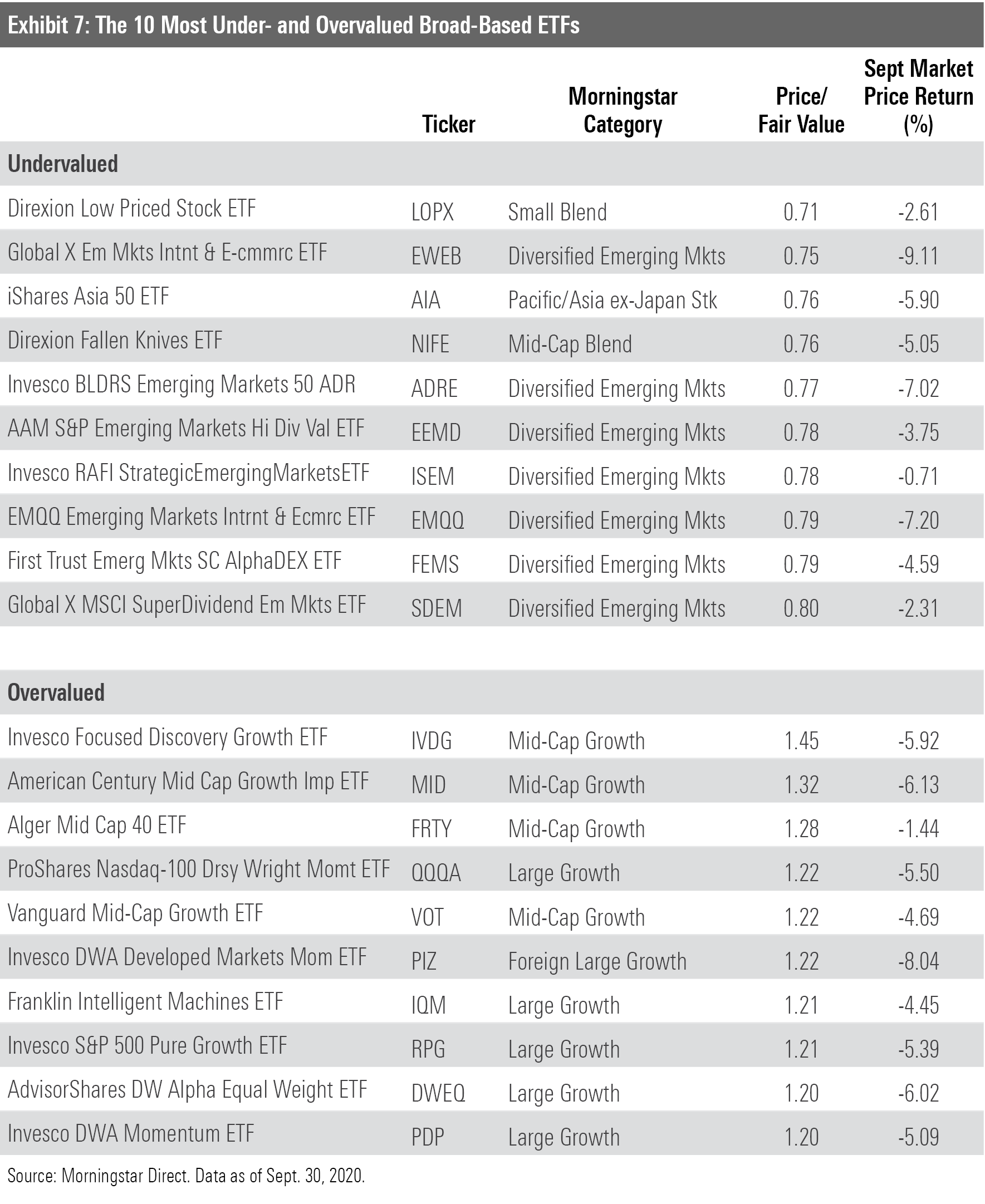

Investors hunting cheap valuations in a more diversified portfolio should likely keep their focus overseas. As Exhibit 7 shows, emerging-markets stock ETFs dominated the ranks of the cheapest broad-based options at the end of September. Most of these funds zero in on international stocks that look cheap relative to their dividends or other fundamental measures of value. The question becomes: Are these funds cheap enough to offer adequate returns for the risk they court?

Global X MSCI SuperDividend Emerging Markets ETF's SDEM risk/reward profile should give investors pause. Relative to the MSCI Emerging Markets category benchmark, its upside-capture ratio was 76% and its downside-capture ratio 103% over the three years through September 2021. The stocks featured in some of these portfolios may be cheap, but not cheap enough to compensate for their risk.

The pricier side of Exhibit 7 consists almost entirely of funds that land in the U.S. large-cap growth or mid-cap growth categories. While currently the most expensive corner of the market, investors with conviction in this space may consider Vanguard Mid-Cap Growth ETF VOT. It's a well-diversified option that channels the market's collective wisdom with its market-cap-weighting approach. Savvy turnover buffers reduce transaction costs and complement its lean 0.07% expense ratio, making it one of the lowest-cost funds in the category. It carries an Analyst Rating of Gold.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/DOXM5RLEKJHX5B6OIEWSUMX6X4.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZKOY2ZAHLJVJJMCLXHIVFME56M.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IGTBIPRO7NEEVJCDNBPNUYEKEY.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/30e2fda6-bf21-4e54-9e50-831a2bcccd80.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/a90ba90e-1da2-48a4-98bf-a476620dbff0.jpg)