The Role of Real Estate Investments in a Portfolio

Investors can benefit from allocating as little as 5% to REITs.

Investor confidence in real estate reached unprecedented levels in 2022, owing to home price appreciation and higher yields for other asset classes, such as REITs, in low-rate environments.

From the start of the pandemic in January 2020 through September 2022, the median sale price for existing homes and new houses in the United States each rose by more than 43%, and rental prices rose by 11%. In the past year, home sellers profited upward of $94,000, which was a 45% increase on investment returns from 2020 and a 71% increase from 2019. Those who owned multifamily properties during the pandemic were able to capitalize on this consistent double-digit rent growth over the past few years.

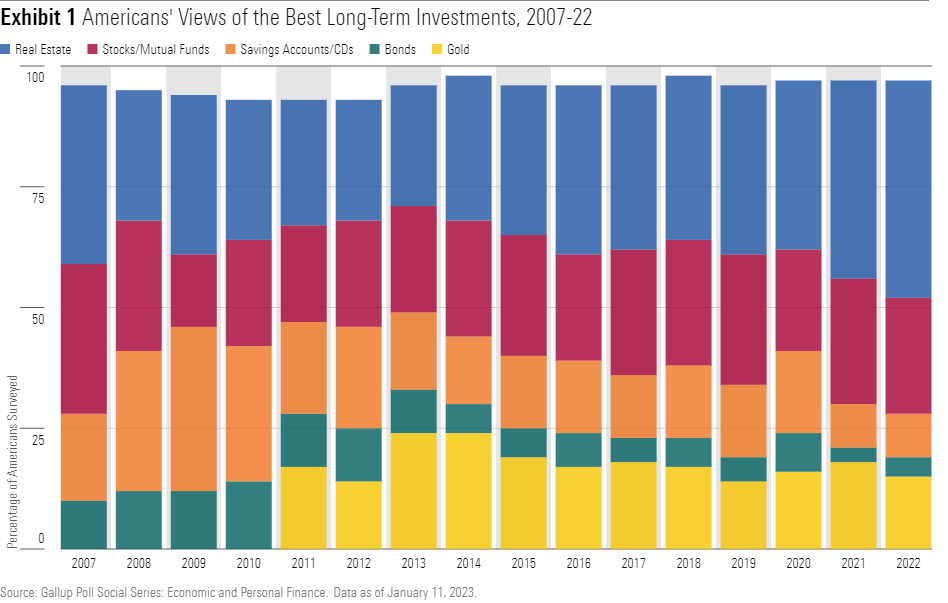

The chart below shows that Americans’ confidence in the housing market is at high point when compared with stocks/mutual funds, savings accounts/CDs, bonds, and gold, even though individual investors generally treat it as an alternative investment asset.

Investment portfolios are often underexposed to real estate investments. But thanks to improvements in their structure since the 2008 global financial crisis, REITs can play a valuable role in diversifying a portfolio.

What’s Behind Increased Investor Confidence in REITs?

After the housing crisis, REIT management teams strategically positioned their investment properties with a lower loan/value ratio, which allowed REITs to have more equity to serve as a margin of safety in case of capital market distress, like the coronavirus recession. In fact, REITs’ leverage lending is at a historic low of 28%, as REIT management teams now aim to rely on raising capital rather than debt to fund property acquisitions and development.

Additional reasons for the improvement of the REIT marketplace include:

- The rising popularity of index funds and exchange-traded funds has helped encourage investors to stay the course and not aim to beat the market.

- Stricter lending regulations make subprime lending issues less likely to occur.

- Investor education is greater than ever because of asset-level information available through the internet.

The crash of the housing market forever changed the standards of real estate for the better, with homebuyers no longer being able to purchase a property with an array of precash loan products and no-documentation loans. Plus, REIT management companies learned their lesson by reducing their ratios of debt/total assets and having 75% to 95% fixed-rate debt to limit exposure to rising interest rates.

These structural changes to the real estate market, in addition to REITs historically rewarding investors well over the long run, have helped investors feel more confident in this asset class. Since the beginning of the modern-REIT era in 1991, REITs’ annualized returns have outperformed the U.S. stock market more than 56% of the time.

What the Literature Says About the Role of Real Estate in an Investment Portfolio

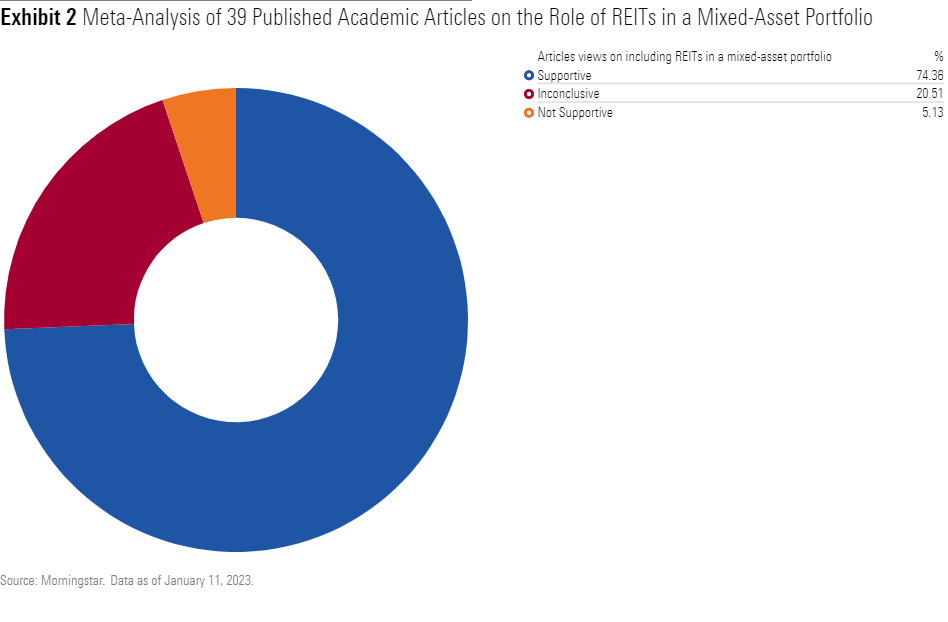

The compelling returns of REITs and recent heightened investor interest in the asset class have led to a rise in academic literature examining the role of real estate in an investment portfolio.

Accordingly, we reviewed 39 empirical articles published in prestigious academic journals (the Journal of Real Estate Portfolio Management, for example) from 1978 through 2022.

In the past two decades, market research and academic literature have suggested that adding REITs to a mixed-asset portfolio offers diversification benefits over long time horizons, primarily because of a low correlation with the U.S. stock market since the late 1990s.

Real estate returns are unlike those of stocks in part because:

- Their returns are primarily generated from income.

- At least 90% of a REIT’s taxable income must be distributed to investors in terms of dividends.

- REITs tend to offer higher dividends.

- REITs tend to follow real estate cycles, which last on average almost twice as long as bond and stock market cycles.

- The property market is highly segmented, which allows investors to diversify by real estate trends.

In addition, when correlations between REITs and stock returns are low, the future of REIT performance tends to be high. This allows investors to use real estate as a defensive stock during periods of economic distress and heightened market volatility.

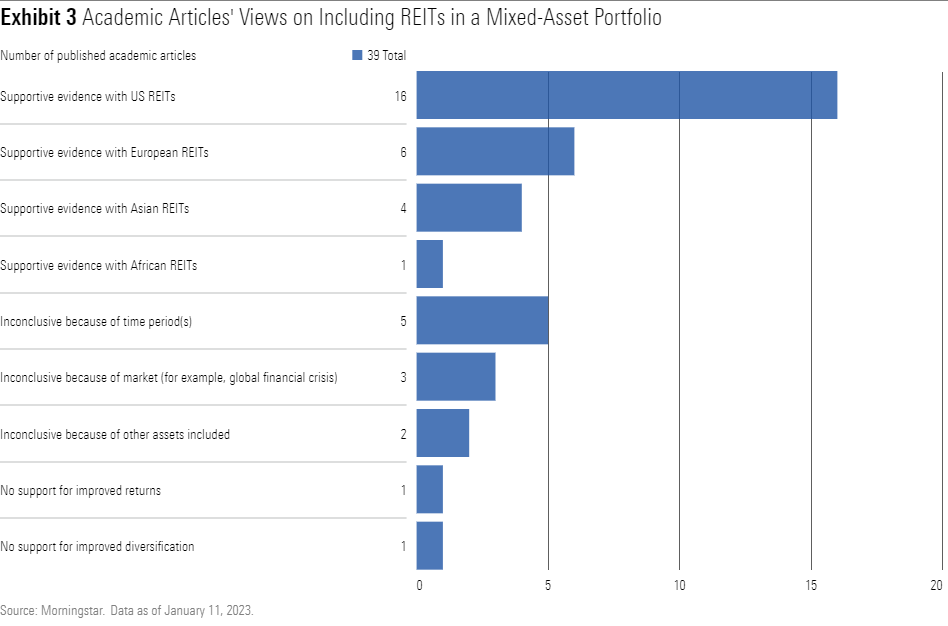

Furthermore, although some academic studies have reached the conclusion that REITs do not add incremental value to a multi-asset portfolio, our review of these studies found that they commonly examined narrow time windows or REITs with higher leverage ratios, and they were often published before the 2008 crisis.

Equity Portfolios Tend to Underrepresent Real Estate

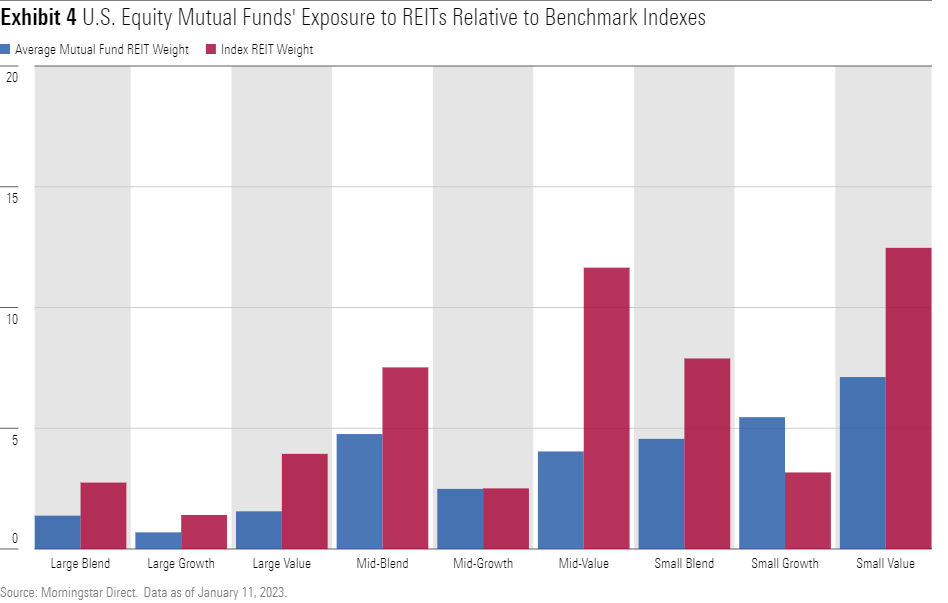

Despite solid performances over extended periods, REITs are typically underutilized as a way to diversify a portfolio, as equity fund managers have consistently been underweight in REITs for the majority of the past two decades.

In the past 20 years, equity fund managers across eight of the nine Morningstar Style Box categories tended to allocate less of their portfolios to REITs; the chart below shows that value funds were least exposed to REITs when compared with their benchmark indexes.

However, our analysis suggests that in recent years, the large-cap market has steadily increased its REIT exposure (although it’s still underexposed). While many individual investors tend to be underexposed to REITs, institutional investors have long embraced real estate as a core asset class because of REITs’ low correlation to the equity market (0.680) and investment-grade bonds (0.003) in the past 20 years, liquidity in the investment, transparency of performance, and low capital requirements.

That said, rising interest rates at the start of November made purchasing property more expensive and subsequently reduced the demand for real estate. Homebuyers and real estate investors alike who thrive on a high-risk, high-reward strategy faced profit margins declining to a 13-year low in 2022 as mortgage rates rose to the highest levels since the second quarter of 2002. While we saw the housing market begin to correct itself in the third quarter of 2022 with home sale prices slowly declining and rent price growth down to a single-digit rate for two consecutive months, it’s a bit unclear how the real estate market will unfold.

The Benefits of Real Estate in a Portfolio

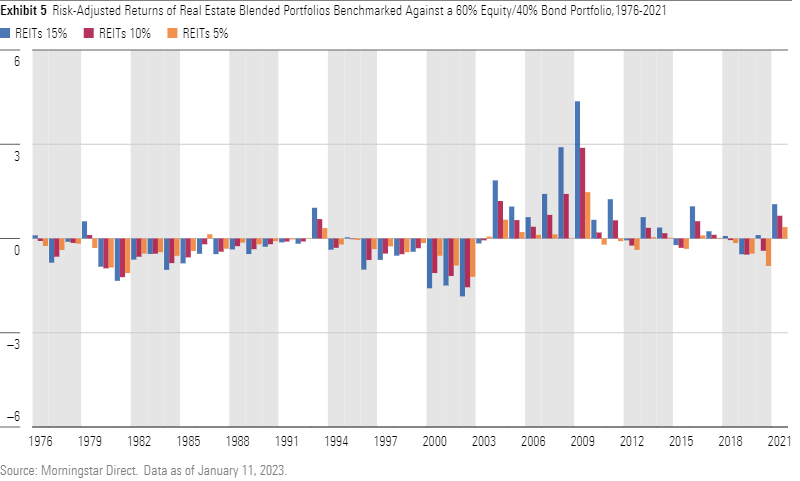

Our analyses highlight that since the early 2000s, allocating at least 5% of your portfolio holdings to real estate leads to greater returns and comes with fewer risks compared with a traditional 60% equity and 40% bond portfolio.

These findings support the abundance of academic literature on asset allocation, which maintains that real estate should account for 5% to 20% of a mixed-asset portfolio.

Additionally, recent research found that low-risk-aversion investors (with their higher benchmark allocation in stocks) who are fully invested in a stock and bond portfolio and are considering real estate assets would obtain higher returns by including REIT common stocks, while high-risk-aversion investors would benefit in more risk reduction from REIT preferred stocks.

Real estate has long been considered an important asset class in portfolio management. However, a recurring question for investors is: Just how much should be allocated to the asset class?

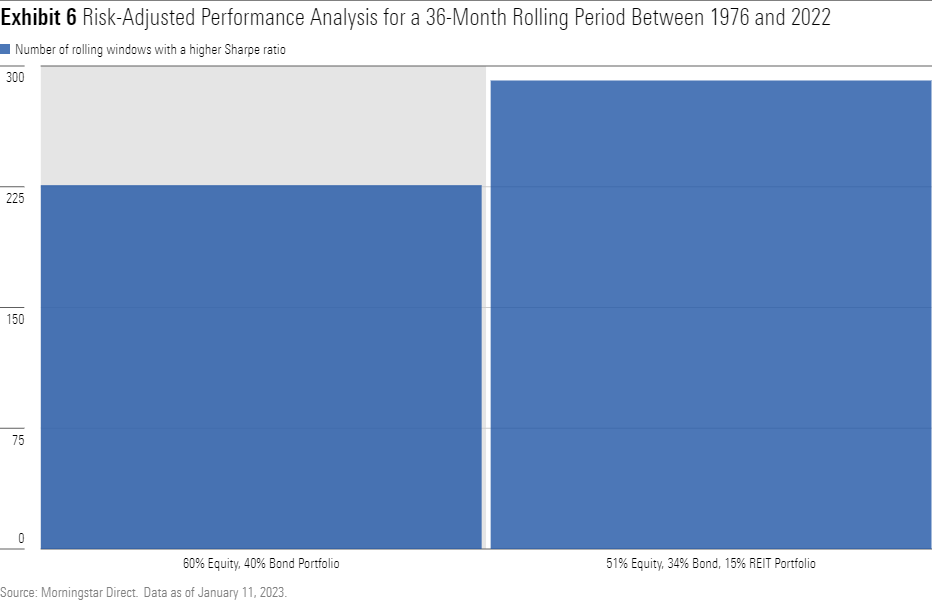

As shown below, our analyses indicate that in the past 46 years, a real estate blended portfolio (51% equity, 34% bonds, and 15% REITs) outperformed a traditional portfolio (60% equity and 40% bonds) 56% of the time.

The Fall and Rise of Real Estate Investments

Real estate has made up a great deal of ground since being the worst-performing asset class during the 2008 crisis. This comeback can primarily be attributed to stringent lending policies for homebuyers, consumer protection policies, and real estate syndications improving the ways they restrict their capital structures.

While there has been ample enthusiasm to dive into real estate recently, individual investors tend to be underexposed to REITs in their portfolio. Academic literature and our research suggest that the inclusion of REITs in a traditional 60% equity and 40% bond portfolio often provides greater risk-adjusted returns in the long term.

However, with federal interest rates rising the most in a single year since 1980, it remains unclear what’s in store for real estate. That said, REITs have shown a sturdy growth of 12% since their inception in 1960, and our research shows that allocating as little as 5% of your portfolio to real estate can bring about greater returns and fewer risks than a traditional mixed-asset portfolio.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

/d10o6nnig0wrdw.cloudfront.net/07-25-2024/t_56eea4e8bb7d4b4fab9986001d5da1b6_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/BU6RVFENPMQF4EOJ6ONIPW5W5Q.png)