Mind the Gap: Global Investor Returns Show the Costs of Bad Timing Around the World

Around the world with investor-timing errors.

/s3.amazonaws.com/arc-authors/morningstar/fcc1768d-a037-447d-8b7d-b44a20e0fcf2.jpg)

The struggle is real. The average investor has lagged behind the average fund for the past 10 years. The reason is that, in aggregate, investors’ timing is not very good. Over the 10 years ended 2016, the average U.S. investor in diversified equity funds enjoyed a 4.36% return, even though the average diversified equity fund returned 5.15%. That’s a fair amount to give up. In fixed income, the gap was nearly as large, and that’s painful because the returns are much smaller. In bondland, we found the average investor received a 2.99% return, versus 3.72% for the average bond fund.

Combining all funds, we come up with a return for the average fund of 4.33% compared with a 3.96% return for the average investor.

This is why I always take time out to warn you to "Mind the Gap." Saving enough money and selecting the right investments are crucial to your success. But timing is another vital piece that investors tend to forget.

Inside the Data To calculate fund investor returns, we adjust the official returns by using monthly flows in and out of the fund. Thus, we calculate a rate of return generated by a fund's investors. As with an internal rate of return calculation, investor return is the constant monthly rate of return that makes the beginning assets equal to the ending assets, with all monthly cash flows accounted for.

In order to roll up that data, we asset-weight investor returns so that we arrive at the average investor return for an asset group. We then compare that with the average fund to see whether investors timed their investments well. To add a new wrinkle, I compared these numbers with asset-weighted total returns based on funds’ asset sizes at the beginning of the time period in order to judge whether investors made wise changes over the subsequent 10 years, or whether they should have stood pat.

You can find Morningstar Investor Return data for a fund on its Morningstar.com page by selecting the Performance tab. As you look, it is worth thinking about the investor return on its own as well as the gap with total returns. The investor return is essentially the aggregate investor’s bottom line. Even if the gap is significant, as long as the investor return is good, you know they did OK. If you see a big gap, it’s worth considering why that gap happened and whether it might be an issue for you.

All single-fund investor returns come with the caveat that there is a fair amount of randomness in them that is beyond the fund manager’s control. Two funds doing the same thing might have different investor returns just because they are in different sales channels or had different launch dates. Some factors are more within the fund company’s control than others, such as how a fund is positioned, the soundness of the strategy, and how volatile a fund is. All of these things play key roles in how well investors use a fund.

What if Everyone Left Their Funds Alone? Hmmmm. That might be a good idea. When I asset-weight returns using assets from 10 years ago, I get better results than from either investor returns or a straight average of returns. For example, the typical diversified equity fund investor would have had a return of 5.31%, topping the 5.15% average fund return and the 4.36% average investor return. For bond funds, the hands-off return was 4.30%, compared with 2.99% for the average investor return and 3.72% for the average fund return.

Even allocation funds lagged the hands-off portfolio: They enjoyed 4.31% returns compared with 4.298% for asset-weighted results at the beginning of the period and 3.87% for the average fund. Why did investors get it right in allocation? Because of 401(k)s and target-date funds. Investing in a 401(k) means you invest every paycheck, and that’s even better than standing pat because you are buying low during sell-offs—provided you don’t panic and give up in a sell-off. As the results show, most investors were able to stick to their plans.

Factors in Investor Returns We sliced and diced the fund universe based on some factors to see if there was a link with investor returns. Expense ratios had the strongest link. The gap grew for each successive quintile of fund expense ratios in equities, and investor returns steadily declined, too. For example, the cheapest quintile (at the start of the 10 years) in diversified equity returned 4.59% compared with 1.78% for the priciest. That means investor returns were much worse in higher-cost funds even if you were to add fees back in. In that same group, the returns gap grew from 1.24% to 2.57% for the priciest funds.

In bonds, the gap was steady across fee groups, though investor returns were higher for cheaper funds. Specifically, cheap funds had investor returns of 3.14% compared with 2.34% for pricey funds. However, the data understate the impact of fees because many high-cost funds were liquidated over the 10-year period we studied and their returns did not make it into the final data. Bond funds in the cheapest quintile were twice as likely to survive as those in the priciest and eight times as likely to survive and outperform their peer group. Thus, the gap issue is hidden by the fact that the high-cost failures were wiped out.

We also tested standard deviation, Morningstar Risk rating, and manager tenure. The results were mixed. Equity funds with lower standard deviation and risk rating had modestly better investor returns than those that were more volatile. However, those factors didn’t really move the needle for bonds or allocation funds. In addition, manager tenure showed no link at all with investor returns.

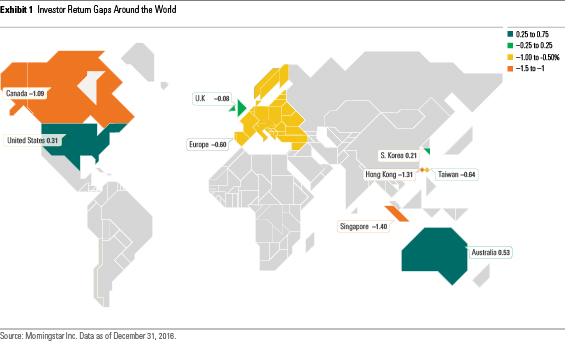

Global Perspective We've expanded our look at investor returns to some key markets around the world. In general, the gaps and behavior patterns were not so different from what we saw in the U.S. However, in most cases we were limited to five years' worth of data. Those figures probably understate the gap because markets have generally trended up and because the gap compounds over time. You can see the gap around the globe in this map. You can find our white paper on global investor returns here.

Strong Results for Automatic Investment Plans In South Korea, investors had particularly good timing in fixed-income funds. In Australia, superannuation funds enjoyed positive gaps. In the U.S., allocation funds had positive gaps. The link across these markets was automatic investment plans. In the U.S., target-date funds have consistently had positive gaps because U.S. investors contribute to their 401(k) savings with every paycheck. In South Korea, general savings plans feature automatic monthly investments, though they are not the only means of investing in funds. These relatively simple plans work wonders at keeping investors on track and preventing them from unwise market-timing moves. Seeing this work in three different investment cultures is a strong endorsement for the practice worldwide.

This is a structure that many regulators around the world are considering as a way to encourage retirement savings. The most recent example is the launch of the Default Investment Strategy on April 1, 2017, by Hong Kong’s Mandatory Provident Fund Schemes Authority. The evidence suggests the idea has merit for its ability to help investors realize the potential of retirement plans. It combines some of the strengths of defined benefit with defined contribution by making low-cost diversified investments the default option.

/d10o6nnig0wrdw.cloudfront.net/04-25-2024/t_d30270f760794625a1e74b94c0d352af_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/DOXM5RLEKJHX5B6OIEWSUMX6X4.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZKOY2ZAHLJVJJMCLXHIVFME56M.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/fcc1768d-a037-447d-8b7d-b44a20e0fcf2.jpg)