ESG Risk in Sustainable Funds

Eighty-four percent of diversified sustainable funds receive 4 or 5 globes in the enhanced Morningstar Sustainability Rating.

/s3.amazonaws.com/arc-authors/morningstar/42c1ea94-d6c0-4bf1-a767-7f56026627df.jpg)

This month we released an enhanced version of the Morningstar Sustainability Rating. The globe rating now reflects environmental, social, and governance evaluations of companies in a portfolio both within and across industry groups. The original version only captured differences among companies relative to their industry peers. As a result, in the original version, portfolios that emphasized companies that were ESG “leaders” among their industry peers or avoided those that were ESG “laggards” tended to receive higher ratings.

Differences in the level of ESG risk across industry groups, however, were not reflected in the original version of the rating, even though companies in some industries clearly face more ESG risks than those in other industries. In fact, as is shown in Exhibit 1, the energy, utilities, and basic-materials sectors carry considerably more ESG risk than the real estate, technology, and communication services sectors.

Sustainalytics' company ESG risk framework, introduced in 2018, compares companies with their peers based on an evaluation of industry-specific material ESG risks, while also taking into account differences in overall ESG risk across industries. A fund's Morningstar Sustainability Rating now reflects both dimensions.

Over the past few years, the universe of sustainable funds has increased significantly. By my count, nearly 300 funds in the United States have an intentional sustainability focus, and another 500 or so have added some reference to ESG in their prospectus, indicating that ESG criteria are now being considered in their investment process.

The enhanced sustainability rating enables us to answer two key questions about these funds. First, how much ESG risk are intentional sustainable funds taking on relative to their peers? Is there any difference between intentional sustainable funds and so-called ESG consideration funds?

How Well Are Intentional Sustainable Funds Managing ESG Risk? Certainly, we should expect sustainable funds to be managing their ESG risks better than conventional funds. In the original version of the sustainability rating, the vast majority of sustainable funds had better ratings, but those ratings only reflected within-industry comparisons. Many sustainable funds, in fact, use some variant of "best-in-class" selection, tilting their portfolios toward ESG leaders and away from ESG laggards.

But not all sustainable funds avoid fossil fuel, for example. In the original version of the rating, a lack of fossil-fuel exposure would not necessarily have hurt a fund's globe rating. In fact, a fund holding the best-in-class company in the integrated oil and gas industry would have benefited from doing so.

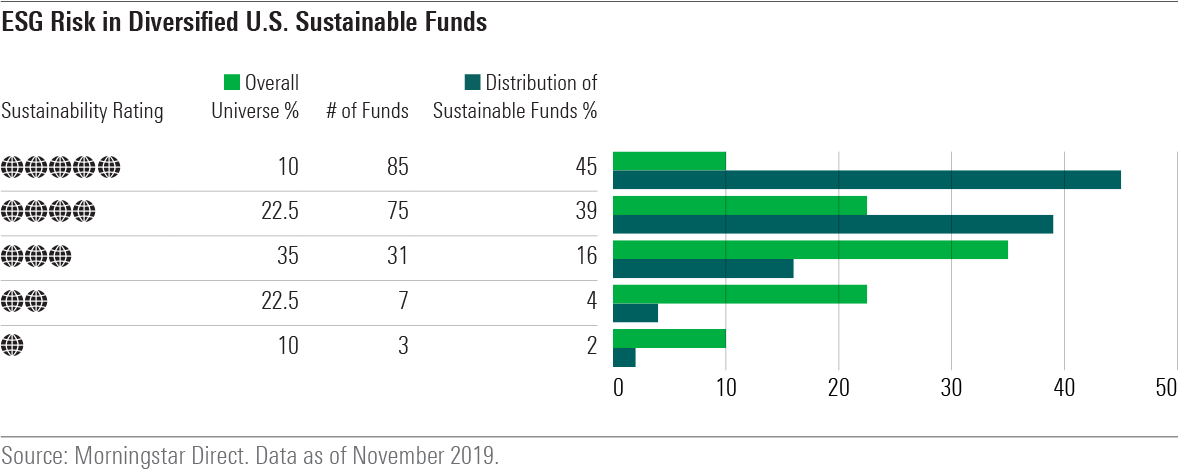

Based on the enhanced rating, Exhibit 3 shows the globe ratings of diversified sustainable funds relative to those of the overall universe of funds. Globes are assigned based on portfolio sustainability scores over the past 12 months relative to a fund's Morningstar Global Category using a normal distribution. Only 10% of all funds in a global category receive 5 globes, and only 10% receive 1 globe. Another 22.5% receive 4 globes and 2 globes, respectively, and the 35% in the middle receive 3 globes.

Diversified sustainable funds have significantly lower levels of ESG risk embedded in their portfolios. More than four in five (84%) diversified sustainable funds receive the highest ratings, 4 or 5 globes, compared with only a third of funds in the overall universe. Only 6% of diversified sustainable funds receive the lowest ratings, 1 or 2 globes, compared with a third of funds in the overall universe.

Diversified sustainable funds fared similarly well in the original version of the ratings. As noted above, that version rewarded "best-in-class" selection, while this version adds industry weightings as a factor. The new rating suggests that most diversified sustainable funds are doing a good job relative to peers at lowering ESG risk both across their industry exposures and within industry groups.

While most diversified sustainable funds also received 4 or 5 globes under the original "best-in-class" version of the ratings, many gained or lost a globe in the transition to the enhanced version. Those that lost globes tend to have largely sector-neutral portfolios. Several funds based on ESG indexes that are sector-neutral fell from 5 globes to 4 globes. These include, among others, iShares ESG MSCI USA ESGU, Fidelity International Sustainability Index FNIDX, and Xtrackers S&P 500 ESG ETF SNPE. Their ratings still benefit from their "best-in-class" approach, reflected by the fact that most of them retain 4 globes, but their ratings took a hit from exposure to high-ESG risk sectors.

Those that gained globes, such as Calvert Emerging Markets Equity CVMIX, Parnassus PARNX, and Pax Ellevate Global Women's Leadership PXWIX, are underweight higher ESG risk sectors and overweight lower ESG risk sectors.

Fossil-fuel exposure has gained significance in the enhanced ratings. Sustainable funds that avoid fossil fuel may now be rewarded for avoiding the high-ESG-risk industries exposed to fossil fuel. The 15 diversified sustainable funds with the least fossil-fuel exposure gained a total of 8 globes in this month's transition to the enhanced rating. Twelve of those 15 funds now have 5-globe ratings. By contrast, the 15 diversified sustainable funds with the most fossil-fuel exposure gained no globes, as a group, and have lower globe ratings. Only one has a 5-globe rating, while the other 14 have 3- and 4-globe ratings.

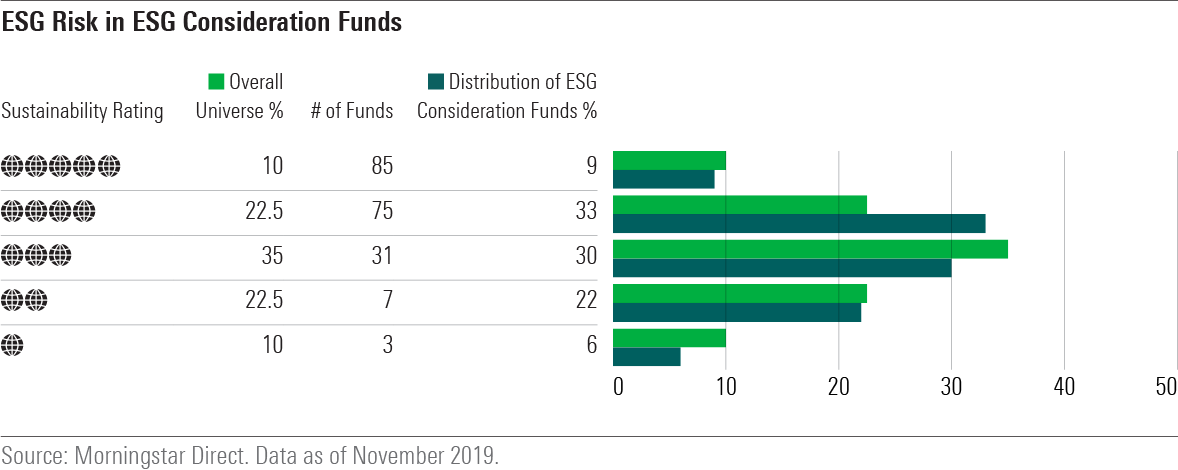

How Well Are Funds That Are "Considering" ESG Managing ESG Risk? Over the past two years, many otherwise conventional funds in the U.S. have added ESG criteria to their prospectus. This trend reflects the realization on the part of many asset managers that consideration of material ESG issues results in a more complete investment analysis. Yet there is little evidence, thus far, of whether ESG "consideration" is actually having an impact on these funds. From an ESG risk perspective, are ESG consideration funds distinguishable from conventional funds, on the one hand, and from funds with a clear sustainable investing mandate, on the other?

ESG consideration funds do exhibit somewhat lower ESG risk than conventional funds. Among ESG consideration funds, 42% receive 4 or 5 globes, versus 32.5% of funds overall. And 28% receive 1 or 2 globes, versus 32.5% of funds overall. Compared with funds that have a sustainable investing mandate, however, ESG consideration funds tend to have much higher ESG risk relative to their category peers, as can be seen by comparing Exhibits 3 and 4.

Intentional Sustainable Funds Exhibit Lower ESG Risk Than ESG Consideration Funds or Traditional Funds The enhanced Morningstar Sustainability Rating now spans two dimensions of ESG risk, reflecting both within-industry and across-industry assessments. An overwhelming majority of diversified sustainable funds receive 4 or 5 globes, far more than the percentage of ESG consideration funds or conventional funds that receive 4 or 5 globes.

Of course, ESG risk, in itself, may not be the only dimension that sustainable investors want to consider. They may also want to know how a fund engages with the companies it owns, votes proxies, and seeks to provide measurable impact beyond financial return. But the material ESG risk embedded in a portfolio is an important component to consider and one that clearly distinguishes intentional sustainable funds from both ESG consideration funds and traditional funds.

Jon Hale has been researching the fund industry since 1995. He is Morningstar’s director of ESG research for the Americas and a member of Morningstar's investment research department. While Morningstar typically agrees with the views Jon expresses on ESG matters, they represent his own views.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

/d10o6nnig0wrdw.cloudfront.net/07-25-2024/t_56eea4e8bb7d4b4fab9986001d5da1b6_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/BU6RVFENPMQF4EOJ6ONIPW5W5Q.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/42c1ea94-d6c0-4bf1-a767-7f56026627df.jpg)