The Costs That Matter for Investors

For most investors, ongoing expenses are much more important than transaction costs.

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

Don’t Bother Him

Last week, when writing about Robinhood's habit of obtaining payments for order flow, which affect the spreads that Robinhood clients pay for their stock and options trades, Bloomberg's Matt Levine wrote to critics of such practices, "If you bought GameStop GME when it was trading at $483, I simply do not care if you paid $483.01 or $483.007 or $483.20, and neither should you."

(Although many brokerage firms resell their customers’ orders, Robinhood correctly receives the most attention, as it is by far the most active practitioner. In the first quarter of 2021, 63% of Robinhood’s revenue came from payments for order flow, as opposed to 10%-15% for its main competitors.)

Levine’s point: GameStop currently costs $189, meaning that it has fallen 61% since its January peak. That loss dwarfs the relevance of trade execution, no matter how well or poorly the transaction was conducted. Fussing that detail is like bemoaning the lack of sunscreen when clutching a life preserver that has been encircled by sharks. Much bigger problems lurk. (And much happier results, too, for those who bought GameStop last summer when it cost $4 per share.)

To be fair, this is an extreme case. With a single, highly volatile security, market performance almost always overwhelms the effect of transaction fees. However, the math becomes less extreme with more realistic portfolios. In such cases, the investor’s wins and losses tend to cancel each other out, plus the individual returns are less dramatic. The drag of one-time costs becomes more important.

A Hypothetical Case

The principle still holds, though. Consider the example of an investor who holds 10 stocks. Each position consists of 200 shares valued at $50, for a total portfolio value of $100,000. For this exercise, I will make aggressive assumptions about three transaction fees that might afflict our hypothetical shareholder. The result therefore exaggerates the consequences of one-time expenditures. Even so, they are not terribly important for most investors.

The first fee has already been mentioned: the spread between the stock's bid and ask prices. Properly speaking, this really isn't a problem at all. Spreads on stock trades have never been lower. Although critics of payments for order flow claim that the practice harms retail investors, the truth appears to be otherwise. For the most part, Robinhood's clients receive better execution when the firm outsources its trade requests. The same holds for the high-frequency traders, who, despite their unsavory reputations, tend to reduce stock spreads rather than raise them.

Thus, I should model the effect of payments for order flows and the activities of high-frequency traders by lowering investor costs rather than raising them. But as I am presenting a worst-case scenario, I will suppose that the development of these two practices has raised stock spreads by 5 cents in each direction. Consequently, clearing completely out of one stock to buy another now costs an additional 10 cents per share, which equals $20 for 200 shares.

Onto the second item, commissions. In 2010, the lowest commission charged by online brokers to execute a stock trade was about $12. These days, thanks to fierce price wars, that figure has dropped to zero. For this exercise, I will assume that retail investors never cared all that much about stock commissions, thereby permitting brokers to retain that $12 umbrella. Add another $24 to the cost of a round-trip trade.

Finally, if Senate Democrats have their way--which they almost certainly will not--stock trades would be hit with a third fee, a financial transactions tax. If enacted, the tax would collect 0.10% of the proceeds from most investment transactions, with the charge split between the buyer and seller. Consequently, swapping one $10,000 equity position for another would cost our investor $10 of tax payments.

That makes for $54 in frictional fees for each $10,000 round trip: 1) $20 for higher stock spreads, 2) $24 for steeper stock commissions, and 3) $10 for the new tax. The first event rarely occurs, the time for the second has come and gone, and the third outcome is highly unlikely. Nevertheless, the combination does provide the practical upper limit of transaction fees (assuming, that is, that the investor is trading liquid, large-cap stocks and is not paying a full-service commission.)

By the Numbers

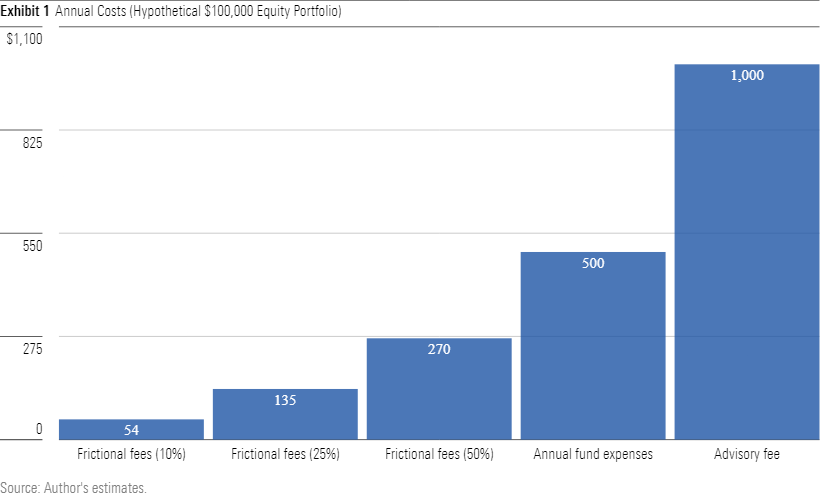

The chart below shows how the transaction fees compare with two flavors of ongoing expenses: 1) the average asset-weighted expense ratio for equity mutual funds and 2) a standard financial-advisory fee. Because transaction costs vary with investor activity, I have modeled three levels of turnover, ranging from 50% to 10%. Most readers, I suspect, land somewhere between those two extremes.

At $270 per year, frictional fees for the 50% turnover portfolio are noticeable, although only half as high as the expenses paid by the typical equity-fund investor. They are half again as high as a conventional financial-advisory fee. To be sure, aggressive traders who measure their time horizons in months rather than years would pay substantial charges. But this discussion is illustrative rather than realistic. Nor is this column written for such investors.

None of this should be taken as advice against owning mutual funds or against hiring financial advisors. Few funds, if any, can justify charging above-market expense ratios, but many are worthwhile purchases at 0.50% annually. As for financial advisors, their contributions vary not only according to their abilities, but also according to the needs of their customers. Judging whether they earn their keep is far beyond the scope of this column.

My point instead is that when investors consider what value they are receiving for their expenditures that their attention mostly be paid to ongoing fees. There was a time when transactional costs were meaningful--but not any more and not for most investors, under most conditions.

John Rekenthaler (john.rekenthaler@morningstar.com) has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar's investment research department. John is quick to point out that while Morningstar typically agrees with the views of the Rekenthaler Report, his views are his own.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/FGC25JIKZ5EATCXF265D56SZTE.jpg)

/d10o6nnig0wrdw.cloudfront.net/04-25-2024/t_d30270f760794625a1e74b94c0d352af_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/DOXM5RLEKJHX5B6OIEWSUMX6X4.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)