The Close-Up View of Target-Date Fund Performance

Putting 2030 funds under the microscope.

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

Reader Response

Last month's column, "When Indexing Is Not an Improvement," pointed out that Vanguard Target Retirement 2030 VTHRX, which holds only index funds, had trailed two of its five largest actively managed rivals over the 10-year period ended Aug. 31. That struck me as newsworthy, given that the CFA Institute Research Foundation had recently suggested that 401(k) plan sponsors consider owning only index funds, both for investment reasons and to reduce their fiduciary liability.

Several readers emailed in response, writing that Vanguard’s fund had not led the way because it was more conservatively positioned. Their thesis being that Vanguard’s fund had been hindered during the long bull market because it held a lower equity position than its rivals. However, over a full market cycle, Vanguard 2030 would triumph, thanks to its ongoing cost advantage.

A worthy argument. If correct, it would have weakened my point. Fortunately for my pride, I anticipated this concern ahead of time, and had checked each fund’s equity weight at the start and end of the 10-year period to ensure that the comparison was fair to Vanguard’s fund. It was. On each occasion, Vanguard 2030’s equity weight placed in the middle of the six-fund pack.

Equity Weights

Which begs the question: What has determined the funds' relative performance? Today's article provides the answer, at least partially.

I began the evaluation by adjusting the calculation period to run for the 10 calendar years from 2011 through 2020. (Using calendar years assured that the necessary data would be available.)

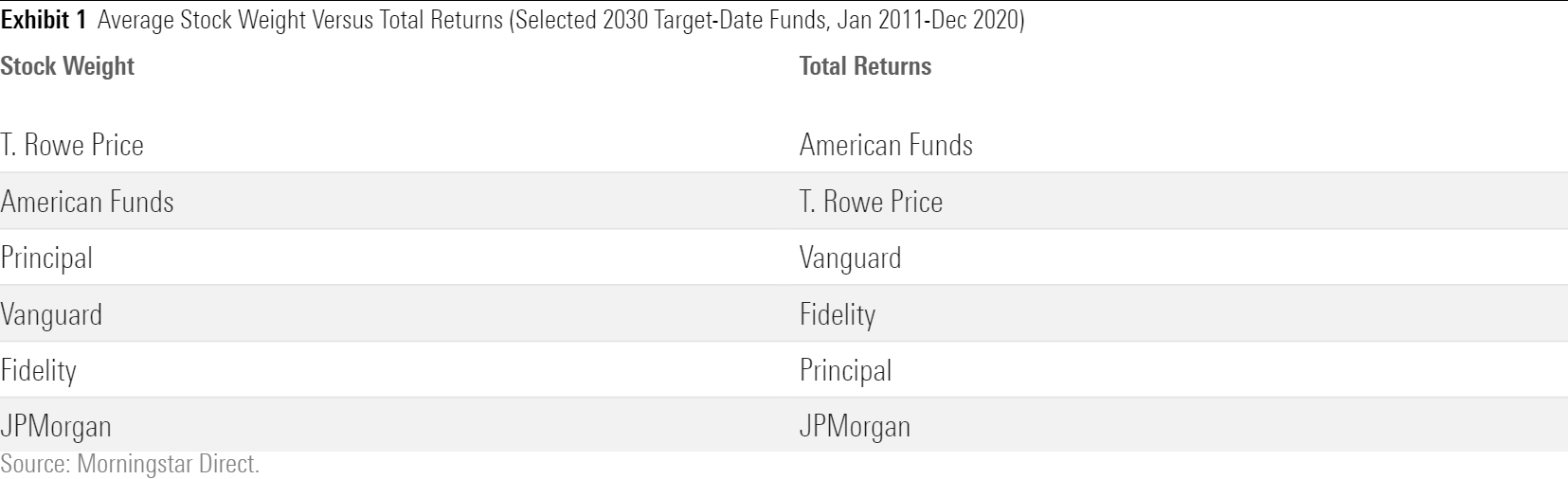

Hmmm. Vanguard’s fund had held the third-highest equity weight during the 2011-20 period, and it finished with the third-highest returns. Would the correlation be that direct? Did the 10-year performances of the six funds align directly with their stock percentages?

I pulled each fund's net stock position, at the start of the 10 calendar years, from Morningstar Direct. (Morningstar.com provides such information for five years but not for 10.) I then compared the rank order of the average stock rating for the six funds to the rank order of their total returns.

Sorting funds by their equity weights told most of the relative-performance story. JPMorgan SmartRetirement 2030 JSMIX was the only fund to retain its exact position, placing last on both accounts (sometimes caution does not pay), but no fund except Principal LifeTime 2030 PMTIX shifted by more than one slot. Principal’s fund dropped two rungs, from the third-highest stock weight to fifth in returns. In the grand scheme of things, though, even that movement was modest.

Expanding the Analysis

Still, relying on the single data point of equity holdings might be overdoing the virtue of parsimony. After all, the decade featured a massive divergence between the performances of domestic and foreign stocks: The Morningstar U.S. Market Index appreciated by an annual 13.9%, while the Morningstar Global ex U.S. Index gained just 5.5%. Domestic stocks easily beat every other portfolio investment, but foreign equities not so much. It was also helpful to own bonds rather than cash.

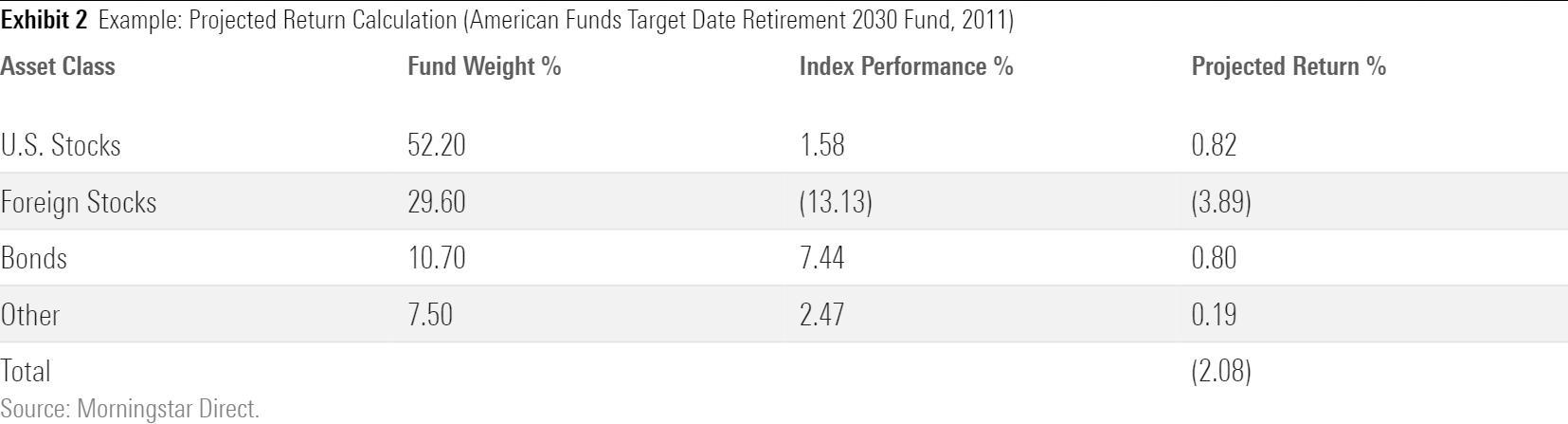

I therefore upgraded the study. It looked at each fund's exposure to four asset classes: 1) domestic stocks, 2) foreign stocks, 3) bonds, and 4) other. As there were now four categories rather than one, I couldn’t simply rank the output. Instead, I calculated calendar-year “projected returns,” by multiplying the percentage of assets that a fund at the start of each year in an asset class by that class’ total returns. For example, this was the projected return for American Funds Target Date Retirement 2030 REETX for the year 2011.

(Note: The Other category consists mostly of foreign bonds and cash. Consequently, I modeled it by averaging the performance of the Morningstar Global ex U.S. Core Bond Index and the Morningstar U.S. Cash T-Bill Index.)

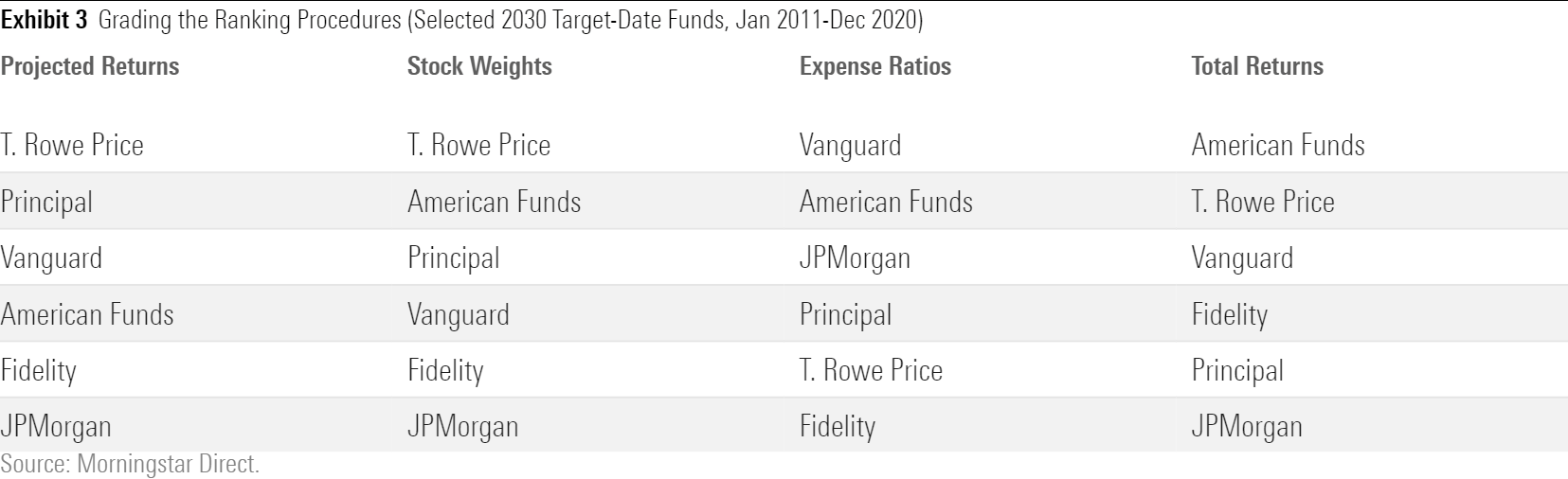

The fund’s actual return was negative 1.86%. That projection was closer than most (you didn’t think that I would choose an errant example, did you?), but none of the estimates were terribly far off the mark. I then combined the 10 calendar-year projections to arrive an annualized projected return for each fund. Once again, I placed the funds into rank order. I then compared the projected return rank order to the orders that came from sorting funds by: 1) their equity exposures; 2) their expense ratios, from lowest to highest; and 3) their actual total returns.

I confess the table is confusing, but I can quickly cut to the chase. To my surprise, the four-category calculation did not improve upon the stock weights’ forecast. In fact, the four-category calculation fared slightly worse, because it pushed the American Funds entry further down the ladder and Principal’s fund further up. Both moves were in the wrong direction. However, both methods of sorting the funds according to their portfolio holdings proved superior to ranking the funds by their expense ratios. That correlation was essentially nil.

Wrapping Up

Do not generalize the previous sentence! This column assessed funds that possess several moving parts, during a bull market that lessened the importance of expense differences, with actively managed funds that are all industry leaders. What’s more, none of the active funds have particularly high expense ratios. This was therefore not a typical comparison between cheap index funds and costly active funds. In such circumstances, the index funds are highly likely to prevail.

Not, I think, in this case. The performances of the 2030 target-date funds--as well as target-date funds of other vintages--will be largely determined by their equity weights.

John Rekenthaler (john.rekenthaler@morningstar.com) has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar's investment research department. John is quick to point out that while Morningstar typically agrees with the views of the Rekenthaler Report, his views are his own.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/G3DCA6SF2FAR5PKHPEXOIB6CWQ.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/6ZMXY4RCRNEADPDWYQVTTWALWM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)