Buy the Unloved: 2021 Funds Edition

After an out-of-favor 2020, the large-cap, bank-loan, nontraditional bond, and world-allocation Morningstar Categories may be due for a rebound.

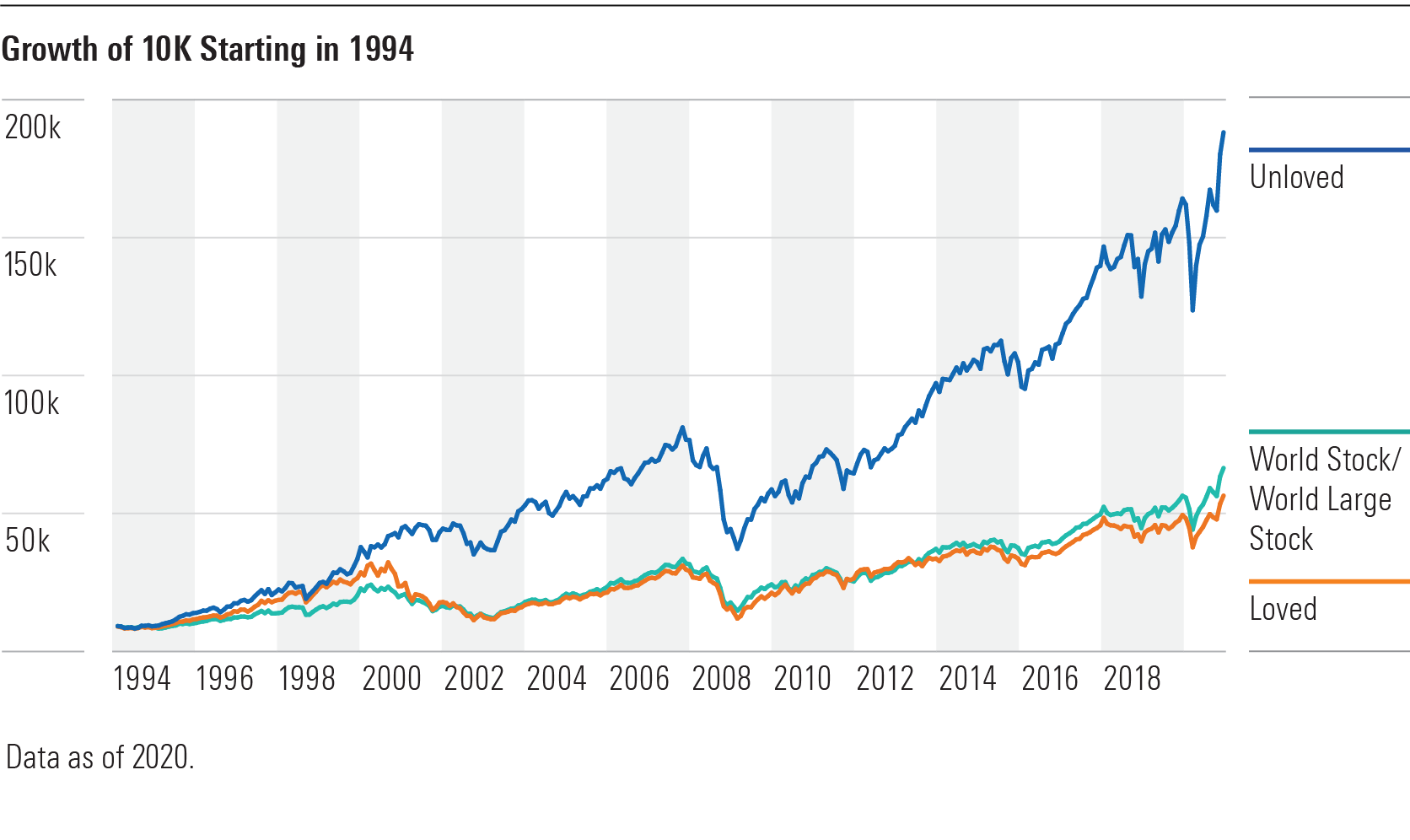

/s3.amazonaws.com/arc-authors/morningstar/c5cfeb1b-84bd-4fc2-9ea1-ed94bbd92e9f.jpg)

A version of this article first appeared in the February 2021 issue of Morningstar FundInvestor. Download a complimentary copy of FundInvestor by visiting the website.

Last year was a tumultuous one that introduced a lot of volatility and uncertainty into the markets. While unpredictability characterized 2020, Buy the Unloved's tried-and-true approach remained steadfast. Buy the Unloved is a contrarian investment strategy that has done well for more than 25 years by pointing investors toward out-of-favor Morningstar Categories. The original iteration dates to 1994 and will be referred to as Version 1. The original received a slight methodology tweak, creating a second iteration, Version 2, which is detailed in this article.

Version 1's longtime, against-the-grain approach works by pointing investors to cheap, or out-of-favor, parts of the market that may be due for a rebound. Rather than evaluating valuations directly, though, it uses flows as a guide. Through this lens, the categories with the most outflows are the most out of favor. The sample size in Version 1 is limited to long-only equity categories. We also exclude those categories where flows are less useful indicators, such as the target-date, trading, and leveraged categories.

In its 25-plus-year history, this approach has rewarded investors. The strategy involves investing equal sums in the three categories with the largest calendar-year outflows (in dollars) for the previous year. After three years, sell the stakes and invest the proceeds equally in that year's unloved categories, and so on. Investors who have followed this simple approach have reaped the rewards.

Source: Morningstar.

While Version 1 has worked well, we expanded our methodology two years ago to include a broader set of categories and factor in the percentage change of flows, not simply absolute flows. To recap, Version 2 includes bond and allocation categories and equally weights dollar flows and the percentage change in assets to determine the loved and unloved. Given the inclusion of fixed income, a new bogy was appropriate. We chose a custom index that's 60% MSCI All Country World Index and 40% Bloomberg Barclays U.S. Universal Index (a broad fixed-income standard). This iteration has a shorter track record, so we need to see how well it works over time.

Let's look at the results. In Version 1, which used net flows in open-end and exchange-traded funds through December 2020, the year's most unloved equity categories were large blend, large growth, and large value. By contrast, the most loved categories were technology, healthcare, and equity energy. Below are some ideas for investing in this year's unloved categories.

Large Blend Parnassus Core Equity PRBLX, which has a Morningstar Analyst Rating of Silver, boasts a disciplined approach that considers environmental, social, and governance characteristics. It excludes companies that derive significant revenue from alcohol, tobacco, weapons, fossil fuels, nuclear power, or gambling and then employs ESG, quality, and valuation screens to filter out about 85% of the universe. From there, it looks for companies with sustainable competitive advantages, increasingly relevant products or services, exemplary management, and ethical practices. The approach has rewarded investors with consistent downside protection. While it tends to sacrifice some of the upside, the fund's long-term record is impressive; we expect this team's approach to continue to reward investors over the long term.

Investors can also opt for more-traditional large-blend exposure with Gold-rated Fidelity 500 Index FXAIX. It is one of the cheapest funds that tracks the S&P 500, which includes large-cap stocks representing about 80% of the U.S. market.

Large Growth Despite outflows, the large-growth category has been on a tear. For a fund that stands apart, Silver-rated Fidelity Contrafund FCNTX is a good option. It boasts a colossal asset base, standing at more than $130 billion, but veteran portfolio manager Will Danoff is up to the challenge. This fund does not track an index. Danoff crafts a well-diversified portfolio of more than 300 stocks that stands apart from its Russell 1000 Growth Index bogy. He's been the manager here since 1990 and has proved that his approach can excel in different market environments. Like many large-growth rivals, Danoff and his team look for best-of-breed companies with competitive advantages, improving earnings potential, and capable leadership. Where the fund distinguishes itself, though, is in execution. For example, Danoff uses the fund's massive scale to his advantage.

Large Value For investors really looking to go against the grain, LSV Value Equity LVAEX is a fine choice. While the team's deep-value approach has been out of favor, it's a solid systematic process that has been consistently applied since its March 1999 inception. The team looks for cheap companies using a set of thoroughly vetted fundamental factors. The firm's proprietary quantitative model runs on EBITDA forecasts, earnings/price estimates, and cash flow estimates. It then ranks the investment universe based upon expected return. It lands in the far-left portion of the Morningstar Style Box (deep value) and boasts a much smaller average market cap than its typical peer. So, if value is out of favor, this fund will be especially hurt. Indeed, that has been the case in recent years. It's a contrarian approach that's worked well over time, but it requires patience.

Version 2 Under Version 2's enhanced methodology that factors in flows as a percentage of total net assets, we arrive at a different cohort of categories. By this measure, 2020's most unloved categories were bank loan, world allocation, and nontraditional bond. Conversely, the most loved categories of the year were corporate bond, high-yield bond, and short-term bond. Below are some options for investing in this other contingent of unloved categories.

Bank Loan The bank-loan category experienced significant outflows during the pandemic-driven sell-off. A distinct group of peers experienced redemptions that averaged 9% of assets over the month of March, and Silver-rated T. Rowe Price Floating Rate PRFRX was no exception. While this fund has been out of favor, contrarian investors should be well-served here. It boasts a robust team and a selective, proven approach that has helped it navigate the bank-loan space deftly. The strategy's process is dictated by fundamental research performed by the credit analyst team. Manager Paul Massaro drives overall portfolio construction and collaborates with analysts to determine conviction and sizing of individual positions. He looks for relative value, focusing mainly on BB and B rated loans while being selective within CCC debt. Liquidity is also a consideration, and Massaro typically maintains 10% to 20% in more-liquid securities, including cash, floating-rate notes, high-yield bonds, and derivatives, which help manage asset flows.

World Allocation This next fund is a differentiated option in the world-allocation category. Silver-rated T. Rowe Price Global Allocation RPGAX benefits from a large team, fairly strong underlying managers, and solid portfolio construction. The fund has a distinct structure. Whereas many world-allocation funds follow a traditional 60/40 equity/fixed-income split, this fund targets 60% in equities, 29% in fixed income, and 11% in alternatives. The latter exposure comes primarily from a Blackstone hedge fund of funds that, until recently, garnered a 10% weighting. This fund can withdraw from the strategy only once every six months and can add to it monthly. As a result, the hedge fund's weighting can drift from its target. At the market trough in early March 2020, it exceeded 12% but was still comfortably short of the 15% illiquid holdings limit imposed on mutual funds. But this fund's team, anticipating further volatility, trimmed the position to 7.5% in July. Management makes allocation calls but doesn't deviate substantially from its neutral weightings. And while the portfolio includes more than 20 strategies, the niche holdings make sense. For example, the fund sold a broad international strategy in 2018 and replaced it with the more focused T. Rowe Price European Stock PRESX and T. Rowe Price Japan PRJPX because they offer more exposure to smaller firms.

Nontraditional Bond Pimco Dynamic Bond's PUBAX lead manager Marc Seidner has impressed in recent years with a circumspect approach that has proved effective under a variety of market conditions. This fund is unfettered by benchmark constraints. Seidner aims to construct a portfolio that outperforms cash by 3-4 percentage points annualized while balancing risk factors such that neither interest-rate nor credit risk dominates its returns. A negative duration and a moderately bullish outlook on the global economy left this strategy struggling in 2015's tough stretch for corporate credit and emerging-markets debt. That caution was welcome during early 2020's extreme pandemic-driven volatility, though. It suffered a 9.3% loss from Feb. 20 through March 23, but its typical competitor fared worse. For investors seeking a more conservative option, this fund should fit the bill.

Conclusion Buy the Unloved isn't a total portfolio investing strategy, and it does not work 100% of the time. While outflows do not directly affect or indicate valuations, the data can point us toward areas of the market that have been beaten down or are unpopular and that may be ripe for recovery. It's also important to consider the contrary case at a time when our own biases may push us toward high-flying funds that may be reaching a tipping point.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

/d10o6nnig0wrdw.cloudfront.net/07-25-2024/t_56eea4e8bb7d4b4fab9986001d5da1b6_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/BU6RVFENPMQF4EOJ6ONIPW5W5Q.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/c5cfeb1b-84bd-4fc2-9ea1-ed94bbd92e9f.jpg)