The Best HSA Plans for Spending

Spending your HSA on current medical costs? Two plans stand out.

/s3.amazonaws.com/arc-authors/morningstar/41940ba6-d0f1-493c-af96-52ad9419064e.jpg)

As we mentioned in an article last week, we recently released our 2018 Health Savings Account Landscape Report, which evaluates and ranks 10 of the largest HSA plans available to individuals assuming two distinct use cases: HSAs as a spending vehicle to cover current medical costs, and HSAs as an investment vehicle to save for future medical expenses. The HSA spending account is typically used by individuals with high healthcare costs who lack the means to pay out of pocket. HSAs represent an attractive vehicle to cover medical costs because the contributions and withdrawals skip out on federal income tax (plus the small amount of interest earned in the checking account isn't taxed).

How We Assessed HSAs as Spending Vehicles When evaluating HSAs as a spending vehicle, we focused on three main components: maintenance fees, additional fees, and the interest rates offered by their checking accounts. For each criterion, we assigned ratings of Positive, Neutral, and Negative. We believe maintenance fees represent the most important consideration when choosing an account. As such, ratings for maintenance fees are the only criterion that drives the overall assessment. This year, our spending account analysis focused only on each plan's account that offers FDIC insurance. The HSA industry remains young, and FDIC insurance gives us--and participants--confidence that healthcare spending dollars are protected from a catastrophic event at the provider.

The information presented in this article and in the report came from HSA plan websites and call centers as of Sept. 30, 2018. The details are subject to change.

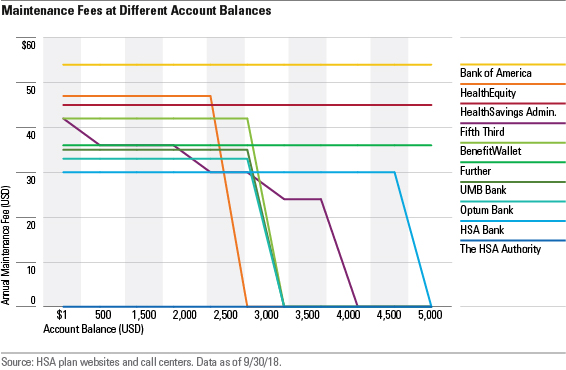

Maintenance Fees: Most plans charge monthly dollar-based fees to cover costs and generate revenue. Of the 10 plans we evaluated, only The HSA Authority offers an FDIC-insured account with no maintenance fees. The other nine plans charge anywhere from $30 to $54 per year, which is significant considering the average HSA balance stands at roughly $2,000. Six of those plans waive the maintenance fees once assets reach $2,500 to $5,000, but most participants have balances well below those thresholds. The chart below shows how each plans' maintenance fees change at various account balances.

Additional Fees: A number of plans charge fees in addition to the maintenance fee that are difficult for accountholders to assess. While these additional fees can add up, they tend to be avoidable and relatively infrequent. For instance, accountholders can sidestep fees for excess contributions or insufficient funds by carefully monitoring account values and deposits. Participants can skip paper-statement fees by opting for electronic statements, they can use debit cards instead of reordering checkbooks, and they can stick with online banking to avoid fees associated with ATM distributions, wire transfers, and manual withdrawals. That reinforces the point that these additional fees are likely to be small in comparison to maintenance fees.

Still, all else equal, we prefer plans that have fewer additional fees. Further, Optum Bank, and Bank of America stand out for minimizing additional fees, with two or fewer extra fees per provider. BenefitWallet, HSA Bank, and HealthEquity have a moderate number of additional fees, with seven or eight each. Fifth Third, The HSA Authority, HealthSavings Administrators, and UMB Bank each have between 10 and 15 additional fees. They would better serve their clients by reducing or eliminating those costs.

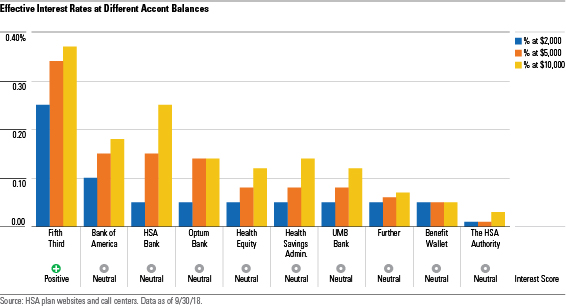

Interest Rates Offered: Interest rates available on checking accounts remain depressed. Accountholders can earn higher rates with higher deposits, but the majority of plans have negligible differences in rates regardless of account size. The chart below shows the effective interest rate--which accounts for multiple interest-rate tiers--that an accountholder would earn with various account balances.

The average HSA checking account balance stands at about $2,000. At that level, accountholders at nine of the 10 plans we evaluated earn between 0.01% and 0.10%. Fifth Third stands out for offering a materially better rate, at 0.25%.

As account balances grow, interest rates begin to make a bigger impact. For instance, once assets reach $10,000, Fifth Third and HSA Bank yield 0.37% and 0.25% APY, respectively. Still, few accountholders have that much in their checking accounts. And at the remaining eight plans, yields on a $10,000 balance range from 0.03% to 0.18% APY, which is unremarkable.

With higher yields and/or higher average account balances, the interest offered may become a more important consideration. For now, they shouldn't weigh too heavily when choosing an HSA--especially one used as a spending account.

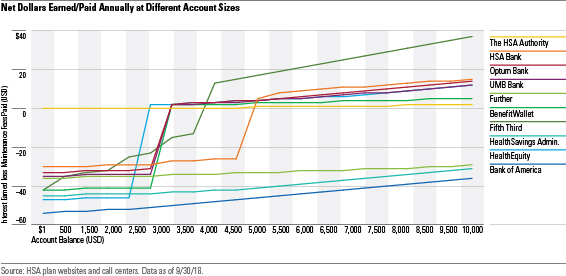

Putting Fees and Interest Rates Together To illustrate the relative impact of maintenance fees versus interest rates, the chart below shows annual dollars earned or paid after netting out maintenance fees and interest earned at account balances ranging from $500 to $10,000. This yields an interesting insight: Accountholders who expect their HSA balance to remain below $4,000 should use The HSA Authority, and those who expect to keep more than $4,000 in their HSA should use Fifth Third. The HSA Authority will either come out ahead or roughly match the best plans at account values of $4,000 or less. Fifth Third's plan waives its maintenance fee at $4,000, and, thanks to its relatively high interest rates, it outperforms all other HSA plans by at least $10 per year in interest. Even if the accountholder's HSA balance temporarily dipped below $4,000 for a year, he or she would lose only about $15, which can be recouped by savings elsewhere in less than two years' time. Fifth Third also becomes gradually more attractive in absolute-dollar terms as assets grow. For instance, it outperforms the second-best plan by $22 annually once assets reach $10,000.

The exhibit below also illustrates how unappealing the plans from Bank of America, HealthSavings Administrators, and Further are for HSA spenders. Those three plans have permanent maintenance fees, regardless of account size. Bank of America's plan is the least attractive, trailing all plans in this study and lagging the best HSA plans by anywhere from $50 to $74 annually.

The Best HSAs for Spenders The table below shows each plan's rating for maintenance fees, additional fees, and interest rates, as well as each plan's overall spending account assessment. As mentioned previously, each plan's maintenance fee rating drives its overall spending account assessment because we think that's the most important consideration for HSA spenders. Plans that charge no maintenance fees receive Positive assessments, plans that waive maintenance fees after assets reach a certain threshold earn Neutral assessments, and plans with maintenance fees that can't be waived receive Negative assessments.

Only The HSA Authority received a Positive assessment for use as a spending vehicle. It’s the only plan we evaluated that doesn’t charge a maintenance fee, allowing spenders to stretch their HSA dollars further.

Plans that levy maintenance fees yet waive them once assets reach a certain balance, including HSA Bank, Fifth Third, Optum, BenefitWallet, UMB Bank, and HealthEquity, receive Neutral assessments. These plans waive fees once balances reach $2,500 to $5,000, but most participants have balances well below those thresholds. After we published our report, HealthEquity informed us that it offers an account with a maintenance fee that is $12 lower than what its call center disclosed to us, and that it begins waiving the fee at a balance of $2,000 instead of $2,500. While those would certainly represent positive developments, the plan’s overall spending account assessment would not have changed in light of that information.

Further, Health Savings Administrators, and Bank of America levy permanent maintenance fees regardless of account balance. All three plans receive Negative assessments.

Our assessments are geared toward the average spender, who has about $2,000 in her HSA account. However, for HSA spenders who intend to keep more than $4,000 in their accounts, Fifth Third represents a better option than The HSA Authority. At that balance, Fifth Third waives its maintenance fee and offers a much better interest rate than all other plans.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

/d10o6nnig0wrdw.cloudfront.net/07-25-2024/t_56eea4e8bb7d4b4fab9986001d5da1b6_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/BU6RVFENPMQF4EOJ6ONIPW5W5Q.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/41940ba6-d0f1-493c-af96-52ad9419064e.jpg)